Germany and Adjustments in Current Account Imbalances

In the mid-2000s, some economists and commentators were concerned that the world was in a “saving glut.”1 That is, the global supply of saving had significantly increased.

This situation gave rise to what was known as “global imbalances,” in which some countries—such as China, Germany and Japan—were running increasing current account surpluses (that is, spending less than what they were producing), while other countries—such as the U.S., Spain, Greece and Portugal—were running increasing deficits (that is, spending more than what they were producing).2

Changes in Global Saving Rates

During the financial crisis, external imbalances around the world began adjusting, and global imbalances started declining. The U.S., for instance, reduced its current account deficit by consuming less and saving more, whereas China and Japan reduced their current account surpluses.

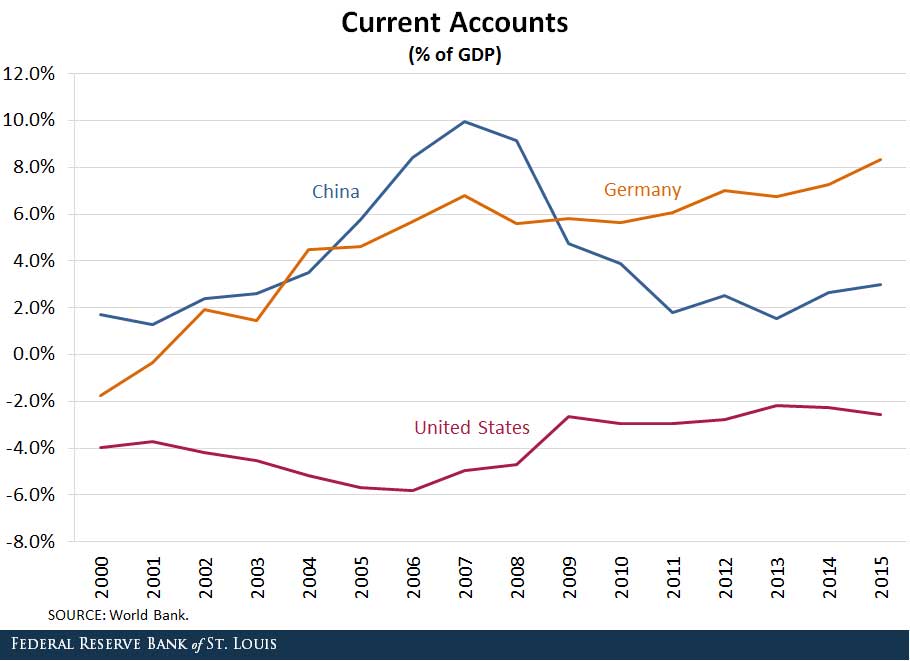

One exception in the rebalancing process has been Germany, a country that kept increasing its current account surplus, even after the financial crisis. The figure below shows the rebalancing of the current account (as a percentage of GDP) in both China and the U.S., as well as the steady increase in the current account surplus (as percentage of GDP) in Germany.

In the U.S., the current account deficit went from -5 percent of GDP in 2008 to -3 percent in 2015. China experienced a similar rebalancing, with the current account surplus dropping from about 9 percent of GDP in 2008 to about 3 percent in 2015. In Germany, however, the current account surplus increased from 6 percent of GDP in 2008 to more than 8 percent of GDP in 2015.

The Rise in Germany’s Trade Surplus

Germany’s trade surplus started increasing initially when employers and unions agreed to contain wage growth. This resulted in an internal devaluation of Germany inside the eurozone, making German products more competitive. This increase in competitiveness triggered an increase in exports and, hence, a trade surplus in Germany.

Another reason behind the increase was related to demographics. Because it is an aging society, Germans have been increasing their savings for the future. This has also contributed to the continuous increase in trade surpluses in Germany.

Policies aimed at increasing investment in Germany could reverse this trend and would help increase investment in the world, helping to further the external rebalance that started in the late 2000s.

Notes and References

1 Bernanke, Ben S., “The Global Saving Glut and the U.S. Current Account Deficit.” March 10, 2005.

2 The current account of a country measures: (i) the difference between its exports to and its imports from the rest of the world and (ii) the international asset position of a country with the rest of the world. If exports of a country are larger than its imports, we say that the country runs a current account surplus, or is a net lender to the rest of the world. If a country’s exports are smaller than its imports, we say that the country runs a current account deficit, or is a net borrower from the rest of the world.

Additional Resources

- On the Economy: Global Current Account Surplus: Is There Trade with Other Planets?

- On the Economy: What Is the Impact of Chinese Imports on U.S. Jobs?

- On the Economy: Does Trading with the U.S. Make the World Smarter?

Citation

Ana Maria Santacreu, ldquoGermany and Adjustments in Current Account Imbalances,rdquo St. Louis Fed On the Economy, June 19, 2017.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions