As Goes Small Business, So Do the Conditions for Commercial Real Estate

It's no secret that since Q4 2007, the U.S. economy has been mired in a "cascading economic recession." The seeds of this recession were a hybrid of over-leveraging and overbuilding earlier in the decade, which germinated artificial economic demand in the form of expanded homeownership, elevated home prices, inflated commercial real estate (CRE) values, excess commercial construction, and elevated consumer confidence and spending. These new sprouts then branched out with foliage in the form of employment growth and near-record small business formations. Strong sales and readily available credit were the nutrients feeding this plant growth.

So, what happened?

Answering this question will be the basis for academic papers into the next decade. In the interim, elected officials, policymakers and economists are wrestling to develop effective strategies now to arrest job loss, stubbornly elevated unemployment, declining real estate values and the expanding ripples of this recession.

This article is not intended to proffer policy answers; rather it is intended to aid in understanding the linkage between the health of small business and commercial real estate. One observation that should be clear from the key small business and CRE metrics that follow is that deciding how to address the woes of either small business or commercial real estate in isolation is a bit like trying to answer the question: Which came first—the chicken or the egg?

Let's explore this relationship by working the problem backward, from the present-day conditions. An examination of a few metrics establishes the inter-relationship of small business and commercial real estate. We'll call this the "Top 10 Correlations List," if you will, between small business and commercial real estate:

…Correlations #10, 9 and 8: Access to credit, government regulation and employee costs (such as health care)

These are three metrics that tend to have material impacts on both small businesses and commercial real estate. Recognizing that most commercial real estate development—especially residential—is dominated by small companies (those with less than 500 employees), commercial real estate developers and owners alike are small businesses. To the extent that credit is limited, employee costs are high, and government regulations are onerous (at both a local and national level), commercial real estate and small businesses struggle to grow.

…Correlation #7: "Poor sales"

According to a 2010 survey by the National Federation of Independent Businesses (NFIB), "poor sales" was the problem identified most (29 percent) as number one by small businesses, followed by taxes (21 percent) and government requirements (15 percent). It follows that if businesses have weak or declining sales, those businesses will not occupy as much CRE space, and why this factor is closely correlated to both small businesses and commercial real estate.

…Correlation #6: Office commercial real estate occupancy and business bankruptcies

Data compiled by office CRE industry trade groups report that approximately 30 percent of all business bankruptcies involve a small service-related business occupying space in an office building or business park. As business bankruptcies have climbed, the national office vacancy rate has climbed to 18 percent.

…Correlation #5: Retail commercial real estate occupancy and business bankruptcies

Data compiled by small business and retail industry trade groups report that between 40 percent and 45 percent of all business bankruptcies involve space in a retail center. Similar to our last factor, as business bankruptcies have climbed, the national retail vacancy rate has risen to 12 percent—and it exceeds 14 percent in more than half of the nation's 100 most populated MSAs, according to CBRE-Econometric Advisors and International Council of Shopping Centers (ICSC).

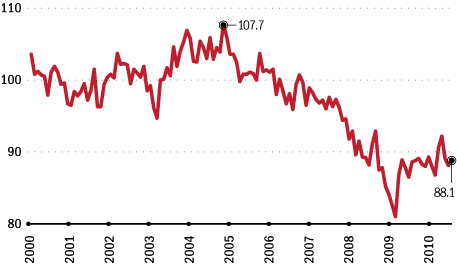

…Correlation #4: The small business optimism index and CRE space

As seen on the accompanying chart, the NFIB Small Business Optimism Index has plummeted from a peak of 107.7 in Q1 2005 to 88.1 at Q2 2010. At the same time, demand for CRE space, measured in the form of net absorption, has been negative.

Small Business Optimism Index (SA, 1986=100)

Source: National Federation of Independent Business

…Correlation #3: Personal bankruptcies and small business sales activity

As personal bankruptcies rise, fewer consumers have disposable income to spend. A rise in personal bankruptcies is then typically followed by a rise in business bankruptcies. That correlation has held through this recession. Personal and business bankruptcies have been rising in the most populated 180 U.S. MSAs for six consecutive quarters (according to the U.S. Census Bureau and the Federal Reserve Bank of Atlanta's Commercial Real Estate Market Spotlight).

…Correlation #2: The ratio of small business employment to job growth

According to the International Council of Shopping Centers (ICSC), 9 percent of non-farm employment in the U.S. is tied to non-anchored retailers in the nations' 104,000 shopping centers.

And…the #1 correlation that demonstrates the interrelationship between small business and commercial real estate: overall job growth

It is not coincidental that business bankruptcies have increased, and commercial real estate values declined as unemployment has remained elevated at or above 9.5 percent.

While the culmination of these metrics demonstrates that small business and commercial real estate are indeed interconnected, the virus adversely impacting both small business and CRE is job loss. If employment growth were to re-establish, unemployed consumers would have income again to spend, and employed consumers would have more confidence in the sustainability of their income. This increased confidence would in turn result in increased consumer spending; increased consumer spending would translate to improved sales—the number one issue cited by small business. Improved sales would result in fewer small business bankruptcies, and fewer small business bankruptcies would then eliminate 75 percent of the increase in retail and office vacancy.

The other piece of this puzzle is credit. In the current environment, both small business and commercial real estate credit is constrained. Small business credit is recessed largely because of a lack of demand. If businesses are primarily worried about poor sales, they are not inclined to expand or utilize lines of credit. There is also a tiered structure of credit for small business. A material percentage of small business utilized credit cards or equity in their homes to fund inventory and receivables. As those sources of credit have contracted (100 million fewer credit cards at Q2 2010 than at Q1 2009), and home values declined, the second-tier of small businesses without other collateral (plant, building, equipment, inventory, etc.) cannot access credit to survive or grow. The challenge for commercial real estate is different. CRE values have declined 45 percent from their 2007 peak (Moody Commercial Property Index), and are still declining. Banks have elevated CRE concentrations, and the capital markets remain largely closed to CRE, with only $5.0 billion in estimated C.M.B.S. issuance in 2010 compared with $234 billion at the peak in 2007. Therefore, the problem with credit to CRE is a concentration of CRE loans in banks and a "refi-gap" created by declining values.

In conclusion, attacking the credit, weak demand and excess supply challenges confronting small business and CRE in isolation will likely prove ineffective. Small business and commercial real estate are intertwined in much the same way as the chicken and the egg. Employment is the common thread. Re-establish employment growth, and the tide of demand will rise for both small business and commercial real estate.

Bridges is a regular review of regional community and economic development issues. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other community development questions