Understanding the Recent Behavior of Inflation

For the last two years, inflation has been high, well above the Federal Reserve’s 2% annual target. High inflation has been persistent and widespread—the result of both supply and demand factors associated with the COVID-19 pandemic, including the fiscal and monetary policies that were implemented in response.For previous work on this subject, see my blog posts “2021: The Year of High Inflation” (April 12, 2022) and “Inflation Is Still High and Widespread” (Oct. 17, 2022). This post is the first in a two-part series that will analyze the behavior of inflation and the impact of fiscal and monetary policies during this episode, and provide a plausible outlook for the near future.

Aggregate Prices and Inflation

Inflation is the change in the price level over a period of time. The Federal Reserve’s preferred measure for the price level is the personal consumption expenditures (PCE) price index, as published by the Bureau of Economic Analysis—essentially, the average price of the consumption component of gross domestic output.

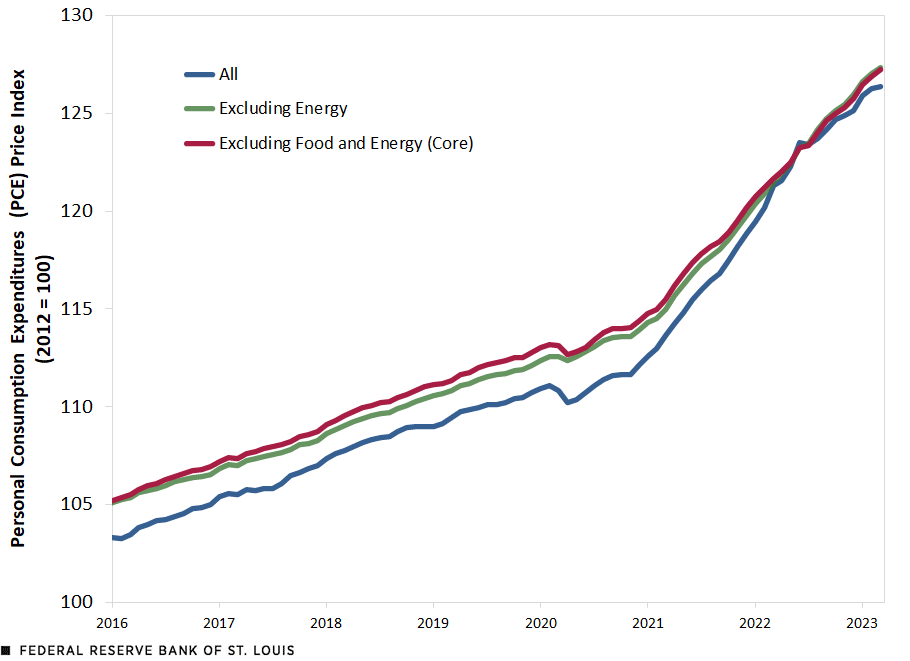

The first figure shows the monthly evolution of the PCE price index since January 2016 until March 2023, the latest data available. It also plots two alternative measures: an index that excludes energy prices and an index that excludes food and energy prices (known as core PCE). Energy prices are largely determined by oil and gas, which are internationally traded commodities whose costs reflect global factors. Although a small component of consumption expenditures (about 4%), energy prices are very volatile and thus drive movements in the average price level that may give a misleading impression of what is happening with prices in general. For somewhat similar reasons, food prices (about 8% of total consumption expenditures) are also removed to then create the core price index, which is often cited along with the “headline” index, which includes all goods and services. However, in recent times, food prices have been less volatile and their behavior during the pandemic more aligned with other prices. Thus, an index that removes only energy prices might be more informative of underlying domestic factors.There are many alternative measures of underlying or trend inflation. For a recent take, see Kevin Kliesen’s April 18, 2023, Economic Synopses essay, “Measures of ‘Trend’ Inflation.”

PCE Price Indexes

SOURCES: Bureau of Economic Analysis and Haver Analytics.

In the period prior to the COVID-19 pandemic, prices were growing at an average annual rate of 1.8%, slightly below the Federal Reserve’s 2% target. This growth process, which we call inflation, was arrested at the onset of the pandemic and resumed toward the end of 2020, though at a significantly faster rate. We can see that energy prices played an important role in this period, as the acceleration and subsequent deceleration in inflation were less pronounced once we excluded them. The index excluding energy and food and the index excluding energy show a steadier, more consistent increase.

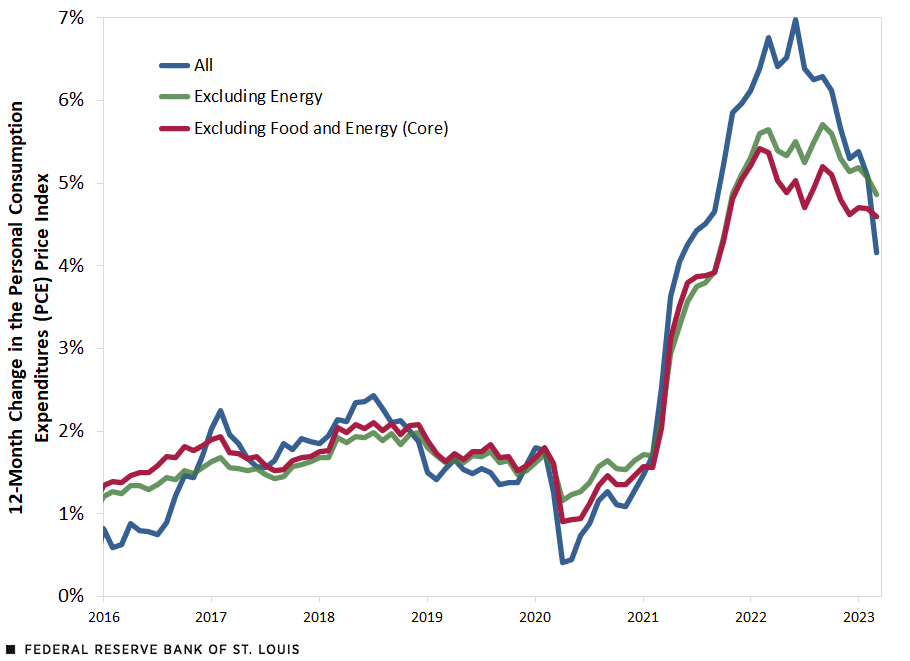

The second figure shows inflation rates, measured as the 12-month change in the corresponding price index. For all three indexes considered, annual inflation has persistently exceeded 2% since March 2021. This figure shows clearly how energy contributed to inflation dynamics. However, when we exclude energy prices, inflation is still very high, staying over 5% annually for all of 2022 and just under 5% in March 2023. When looking at core PCE, i.e., excluding both food and energy, there is a modest moderation in inflation from its peak, but it is much less pronounced than with headline inflation.

Annualized PCE Inflation Rates

SOURCES: Bureau of Economic Analysis and Haver Analytics.

The first table provides a summary of inflation rates over various periods of interest. The first, 2016-19, covers the years immediately prior to the pandemic, when inflation was close to the Federal Reserve’s 2% target. Next are the years 2020, 2021 and 2022. Finally, the period labeled “COVID-19” covers the whole pandemic period, between March 2020 and March 2023. All inflation rates are annualized to make them comparable across periods of different lengths.

| All Goods and Services | Excluding Energy | Excluding Food and Energy (Core) | |

|---|---|---|---|

| 2016-19 | 1.8% | 1.7% | 1.8% |

| 2020 | 1.3% | 1.6% | 1.5% |

| 2021 | 6.0% | 5.1% | 5.0% |

| 2022 | 5.3% | 5.1% | 4.6% |

| COVID-19 | 4.3% | 4.1% | 3.9% |

| SOURCES: Bureau of Economic Analysis, Haver Analytics and author’s calculations. | |||

| NOTES: The COVID-19 period starts in March 2020 and ends in March 2023. | |||

The table highlights how inflation accelerated in 2021 and 2022. Overall, the aggregate price level rose at an average annual rate of 4.3% since the start of the COVID-19 pandemic. This rate moderates to 4.1% annually when we exclude energy prices and 3.9% annually when we exclude both food and energy prices. These rates are between 2.1 and 2.5 percentage points higher than the pre-pandemic period and well in excess of the Federal Reserve’s 2% target.

Breaking Down Inflation

The second table decomposes inflation excluding energy into four big categories: food, core goods, core services excluding housing, and housing. The contribution of these components in total consumption expenditures is, roughly, 8%, 22%, 50% and 16%, respectively (the remaining 4% reflects expenditures in energy goods and services).

| Food | Core Goods | Core Services Excluding Housing | Housing | |

|---|---|---|---|---|

| 2016-19 | 0.2% | -0.6% | 2.4% | 3.4% |

| 2020 | 3.9% | 0.0% | 1.7% | 2.2% |

| 2021 | 5.7% | 6.1% | 5.1% | 3.7% |

| 2022 | 11.6% | 3.4% | 4.2% | 7.7% |

| COVID-19 | 6.6% | 3.2% | 3.8% | 4.8% |

| SOURCES: Bureau of Economic Analysis, Haver Analytics and author’s calculations. | ||||

| NOTES: The COVID-19 period starts in March 2020 and ends in March 2023. | ||||

The behavior of these components was very different during the pre-pandemic period: Food experienced almost no inflation, core goods prices were actually declining (mostly driven by durables), while core services excluding housing and housing were both growing above the Federal Reserve’s target rate. The pandemic changed these trends: Since 2021, all components have been growing at rates higher than 2% annually. For the overall pandemic period, food experienced the fastest inflation rate (6.6% annually), followed by housing (4.8% annually). In recent communications, Fed Chair Jerome Powell has identified the category “core services excluding housing” as key in understanding inflation dynamics.As Powell explained in his Nov. 30, 2022, speech, the reason is that “wages make up the largest cost in delivering these services.” Inflation in this category has largely behaved the same as for the core price index and remains well above 2%.

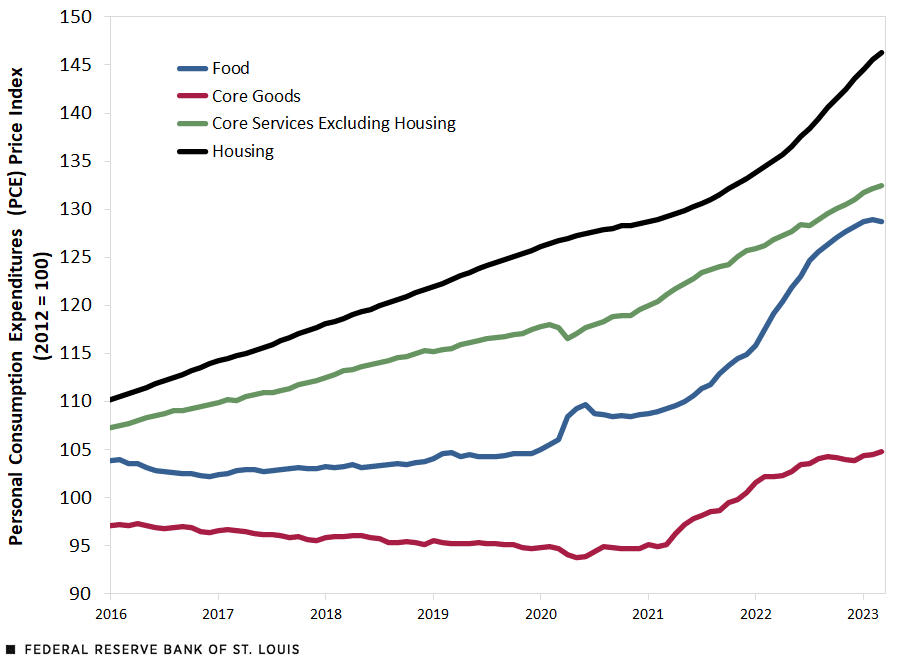

Components of the PCE Price Index Excluding Energy

SOURCES: Bureau of Economic Analysis and Haver Analytics.

Above, the third figure shows the evolution of prices of the main components discussed earlier.

Notably, the price of core goods seems to have stabilized during the second half of 2022, while inflation in food prices has decelerated markedly over the same period. In contrast, the rate at which the price of core services excluding housing is increasing shows no signs of slowing down. Similarly, housing services actually experienced a significant acceleration in inflation in 2022. It is well understood that housing prices tend to lag other prices,This is because rents are renewed infrequently (e.g., once a year) and because owner-occupied housing prices are also measured largely using rent data. so the most recent observations may reflect this lag rather than a current trend. Even if this were the case, core services excluding housing—which account for half of consumption expenditures—continue to rise steadily and are a major contributor to overall inflation.

Inflation Is Widespread

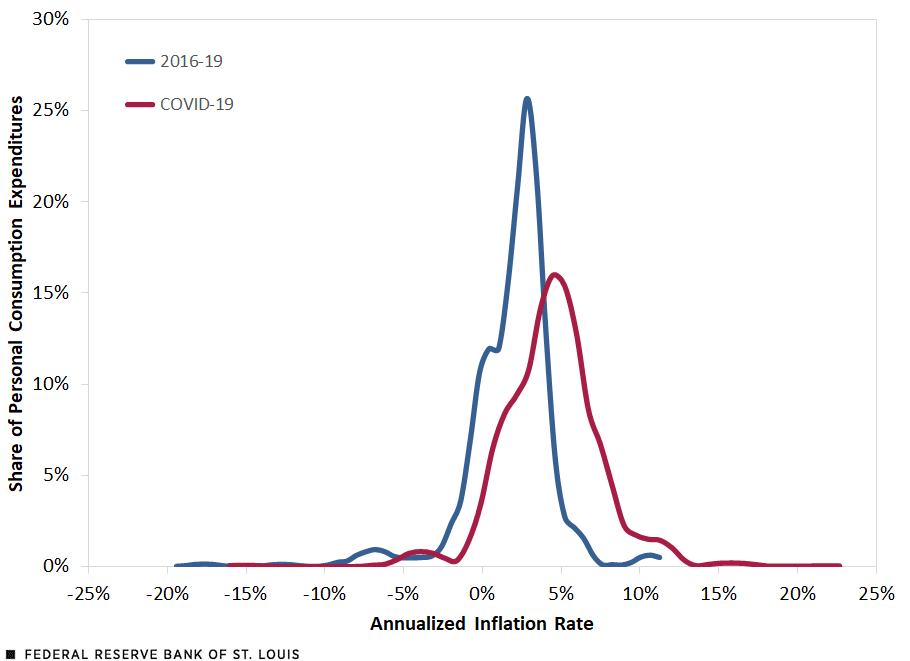

We can further analyze inflation across individual product categories by computing their annualized price change and expenditure share in each period. The fourth figure estimates the distribution of inflation across product categories, with annualized price changes on the horizontal axes and the corresponding expenditure shares on the vertical axes.The disaggregated data published by the Bureau of Economic Analysis consist of 244 product categories with monthly series on expenditures, prices and real quantities. There is some double counting in the report, so the actual number of product categories is slightly smaller. See NIPA tables 2.4.4U, 2.4.5U and 2.4.6U. For a full description of the methodology, see my blog post “How Widespread Are Price Increases in the U.S.?” (Oct. 19, 2021). I considered two periods: the pre-pandemic period (2016-19) and the COVID-19 period (March 2020 to March 2023). Focusing on the COVID-19 period as a whole removes the effects of temporary surges in prices and provides a better overall picture.

Estimated Distribution of PCE Inflation

SOURCES: Bureau of Economic Analysis and author’s calculations.

NOTES: Distributions are computed with kernel density estimation in Stata, using the optimal bandwidth for each period. The COVID-19 period covers March 2020 to March 2023.

The pandemic has shifted the distribution of inflation to the right. That is, during the COVID-19 period, a larger share of consumption expenditures were on products that experienced higher inflation rates than in the pre-pandemic years. The current high inflation episode is a widespread phenomenon and not the result of a few outliers.

The distribution of inflation across product categories also highlights several important differences between the pre-pandemic and COVID-19 periods. From 2016 to 2019, 18% of consumption expenditures were on products experiencing negative inflation; this proportion drops to less than 1% in the COVID-19 period. Conversely, the share of expenditures on products experiencing more than 5% annual inflation was only 5% in the pre-pandemic period and rose to over 40% during the COVID-19 period. These are significant changes that help us understand the nature of the current high inflation.

In my next post, I’ll examine the impact of fiscal and monetary policies during this inflationary episode and provide a plausible outlook for the near future.

Notes

- For previous work on this subject, see my blog posts “2021: The Year of High Inflation” (April 12, 2022) and “Inflation Is Still High and Widespread” (Oct. 17, 2022).

- There are many alternative measures of underlying or trend inflation. For a recent take, see Kevin Kliesen’s April 18, 2023, Economic Synopses essay, “Measures of ‘Trend’ Inflation.”

- As Powell explained in his Nov. 30, 2022, speech, the reason is that “wages make up the largest cost in delivering these services.”

- This is because rents are renewed infrequently (e.g., once a year) and because owner-occupied housing prices are also measured largely using rent data.

- The disaggregated data published by the Bureau of Economic Analysis consist of 244 product categories with monthly series on expenditures, prices and real quantities. There is some double counting in the report, so the actual number of product categories is slightly smaller. See NIPA tables 2.4.4U, 2.4.5U and 2.4.6U. For a full description of the methodology, see my blog post “How Widespread Are Price Increases in the U.S.?” (Oct. 19, 2021).

Citation

Fernando M. Martin, ldquoUnderstanding the Recent Behavior of Inflation,rdquo St. Louis Fed On the Economy, May 8, 2023.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions