Do Institutional Investors Chase Returns?

Studies have shown that investors’ expectations of future stock market returns are positively correlated with previous stock market performance, but do not match up well with actual future returns.1 Namely, investors tend to be more optimistic than they should be after observing good returns.

Studies have also suggested that even professional investors, such as institutional investors, follow the same pattern.2 In this blog post, we’ll take a closer look at whether institutional investors chase returns.

Buying High and Selling Low

Expectations and experience play important roles in investor behavior in the stock market. Investors increase their stock holdings if their expectations of future returns rise, and they cut down if their expectations lower. Therefore, a positive correlation between past returns and return expectations leads to returns-chasing behavior, which is characterized by buying after a high return and selling after a low return.

However, a high return implies a relatively high price. Thus, returns-chasing investors are likely to buy high and sell low, which could reduce their overall return over time.

Institutional Investors and Chasing Returns

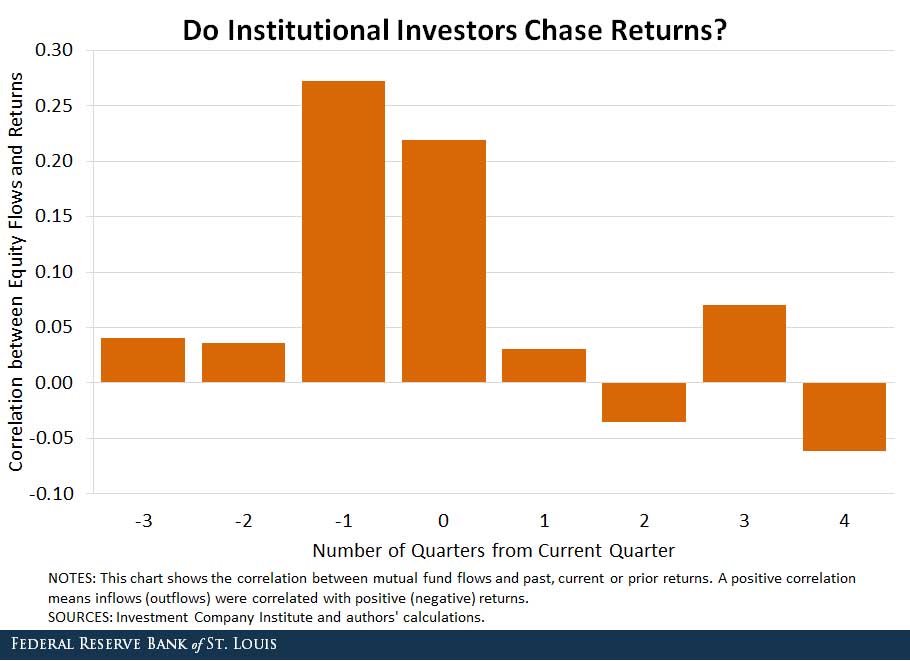

We examined if institutional investors are immune to returns-chasing behavior. We used domestic mutual fund data from the Investment Company Institute from the first quarter of 2000 through the second quarter of 2016.3 The figure below plots the correlation coefficient between equity flows and returns for the equity mutual funds held by institutional investors.4

The correlations between current equity flows and past returns were positive but quite modest. For the previous and current quarter, the correlations were 0.27 and 0.22, respectively. The positive correlations suggest that equity mutual fund investors tend to buy when recent returns are high, but the relationship is not strong.

The correlations between today’s equity flows and future returns were close to zero. This indicates that the buy or sell decisions made by the institutional investors have no predictive power on future returns.

In sum, we find modest returns-chasing behavior among the institutional investors. Even though their buy and sell decisions have close to zero correlation with future returns, their returns-chasing behavior is still likely to reduce their overall returns because they are more likely to buy high and sell low.

Notes and References

1 See, for example, Greenwood, Robin; and Shleifer, Andrei. “Expectations of Returns and Expected Returns.” Review of Financial Studies, March 2014, Vol. 27, Issue 3, pp. 714-46.

2 Greenwood and Shleifer (2014) suggest this as well.

3 The mutual fund data are well-suited for analyzing returns-chasing behavior because they include data for quarterly net cash flows to mutual funds as well as the net value of mutual funds. The net cash flow data indicate the additional funds added or withdrawn. Hence, we can simply compute the correlation between net cash flow and the past and future returns of mutual funds. In addition, the mutual funds are classified by method of sale. In general, there are two main categories: retail sales and institutional sales. The latter refers to those sales made primarily to institutional investors and institutional accounts. Hence, we can reasonably assume the investor behaviors observed in institutional sales are done mostly by the institutional investors.

4 The correlation coefficient indicates a stronger positive correlation the closer it is to 1 and a stronger negative correlation the closer it is to –1.

Additional Resources

- Economic Synopses: The Cost of Chasing Returns

- On the Economy: Mutual Fund Flows and Investor Behavior

- On the Economy: The Stock Market Is Up, but Mutual Fund Investors Are Fleeing

Citation

YiLi Chien and Paul Morris, ldquoDo Institutional Investors Chase Returns?,rdquo St. Louis Fed On the Economy, Feb. 16, 2017.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions