Global Supply Chain Disruptions and Inflation During the COVID-19 Pandemic

Abstract

We investigate the role supply chain disruptions during the COVID-19 pandemic played in U.S. producer price index (PPI) inflation. We exploit pre-pandemic cross-industry variation in sourcing patterns across countries and interact it with measures of international supply chain bottlenecks during the pandemic. We show that exposure to global supply chain disruptions played a significant role in U.S. cross-industry PPI inflation between January and November 2021. If bottlenecks had followed the same path as in 2019, PPI inflation in the manufacturing sector would have been 2 percentage points lower in January 2021 and 20 percentage points lower in November 2021.

Introduction

The COVID-19-pandemic recession and recovery have been unique compared with previous recessions, largely due to policies that led to behavioral changes. Lockdowns meant people were traveling less both for work and for leisure, eating out less, and going to fewer entertainment venues, among other things. At the same time, work from home and fiscal stimulus packages increased the demand for certain goods such as technological goods, cars, and furniture. These changes resulted in an overall shift away from consumption of services and toward consumption of durable goods.

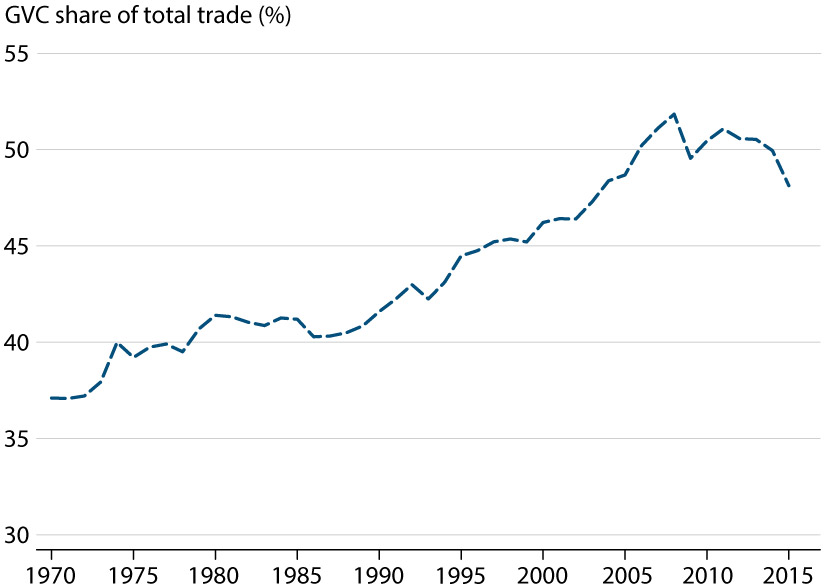

The rapid increase in the demand for durable goods, together with the global nature of the pandemic, has exposed vulnerabilities in the current production structure of these goods. Over the past several decades, production of durable goods has become more fragmented, relying heavily on global value chain (GVCs). Instead of doing everything in-house, firms can outsource parts of their production processes to other countries. Figure 1 shows that GVC participation has been rising steadily over time, though it has plateaued in recent years (see Antrás, 2020).

Figure 1: GVC Participation Over Time, 1970-2015

NOTE: The figure represents the evolution in the share of total trade that requires inputs from at least two countries.

SOURCE: World Bank World Development Report 2020.

While GVC participation has advantages, as firms can benefit from outsourcing production to regions with a comparative advantage, it comes with risks (Santacreu and LaBelle, 2021a,b). Shocks that hit a particular stage of the production process can propagate along the chain and expose firms dependent on inputs from these regions. Some of these risks did materialize during the current pandemic through global lockdowns (Leibovici, and Santacreu, and LaBelle, 2021), low vaccination rates in emerging countries (Çakmaklı et al., 2021), and large shipping costs and disruptions in some key ports, putting additional pressure on supply chains.

These risks can be exacerbated when supply chains rely heavily on critical inputs from one or a few regions. Take the example of semiconductors. The advancement of technology in nearly every product has made semiconductors a vastly important input for the entire economy; however, their production largely relies on a few countries, such as Taiwan and China. A sharp increase in the demand for products that use this input may create large bottlenecks in semiconductor-dependent industries. Therefore, due to the global nature of supply chains, even a relatively small demand shock to a critical sector can propagate into a larger supply/demand disruption. This mismatch between supply and demand puts upward pressure on prices. In this article, we address the following question: To what extent has the global nature of supply chain disruptions contributed to producer price index (PPI) inflation across U.S. sectors?

The main challenge to answer this question is the limited access to real-time data on supply chain disruptions. We rely on the Purchasing Managers' Index data from IHS Markit. These data, which are available with a subscription, comprise monthly surveys sent to senior executives at private firms in 44 countries. We focus on two measures from this survey that capture supply chain disruptions: backlogs and supplier delivery times. Backlogs measure how much the number of unfulfilled new orders has changed from the previous month; delivery times measure how much the average time it takes for suppliers to deliver inputs has changed from the previous month. Each variable represents a rate of change over the previous month, and both capture demand and supply effects. Higher backlogs typically indicate that demand is increasing at a rate producers cannot meet, while the opposite indicates unused production capacity resulting from a lack of demand. Hence, backlogs measure how quickly suppliers can keep up with demand. The same logic applies to delivery times. As such, these measures can be used to infer demand and supply mismatches that contribute to price increases and inflation.

We begin by documenting three salient features of the data on supply chain disruptions. First, bottlenecks have become worse since January 2021, as implied by an increasing number of unfulfilled orders and longer delivery times. Second, backlogs and delivery times track PPI inflation quite well, with each having a correlation of about 90 percent for the period January 2020 to November 2021. Third, supply chain disruptions and their contribution to PPI inflation have been heterogeneous across industries. Backlogs increased sharply in the automobile and technology equipment industries. These increases were followed by large increases in PPI inflation. In the pharmaceutical industry, however, bottlenecks remained relatively steady, which were reflected in a steady increase in PPI inflation over the same period. These results suggest that the supply and demand mismatch was worse in the technology equipment sector and the automobile and auto parts sector than in the pharmaceutical sector.

We then ask the following question: Did U.S. industries more exposed to global supply chain disruptions experience higher PPI inflation over this time period? To answer this question formally, we construct measures of industry exposure to supply chain disruptions, both domestic and foreign. In particular, we exploit heterogeneous variation in an industry's sourcing patterns across countries and interact it with our measures of supply chain disruption: changes in backlogs and in delivery times, respectively. If an industry in the United States relies heavily on intermediate inputs from a country where supply chain disruptions are severe, this industry will be more exposed. We consider both the manufacturing and non-manufacturing sectors. To the extent that for each industry we keep the value-added shares fixed at the levels in 2018, the interaction with the bottleneck variables in our exposure measure captures the role of the supply shock in that particular industry.

Our empirical strategy consists of regressing industry PPI inflation on our measures of domestic and foreign exposure, including industry fixed effects. We focus on the period January 2021 to November 2021. We find that both domestic and foreign exposure have a positive effect on industry PPI inflation. However, only foreign exposure is statistically significant. These results hold when using either backlogs or supplier delivery times as the measure of disruption. Moreover, the effects of global supply chain disruptions on PPI inflation are larger if the exposure variables are lagged by one month, suggesting that supply chain disruptions have a delayed impact on inflation. We then conduct the same regression analysis but separate the industries into manufacturing and non-manufacturing sectors. In the non-manufacturing sector, both domestic and foreign exposure have a positive and statistically significant effect on PPI inflation. In the manufacturing sector, however, only foreign exposure is statistically significant.

Finally, we ask the following question: What would PPI inflation have been during 2021 if backlogs in each country had followed their 2019 path? To answer this question, we do a back-of-the-envelope calculation in which we take the results from our regression analysis and compute a counterfactual PPI inflation rate using the data on bottlenecks from 2019. We find that PPI inflation in the manufacturing sector during 2021 would have been 2 percentage points lower in January and 20 percentage points lower in November 2021.

Our results show that supply chain disruptions during the COVID-19 pandemic recession and recovery have been unprecedented. The shift in demand toward durable goods consumption and the heavy reliance on foreign suppliers to produce these goods has created a mismatch between supply and demand resulting in price increases. Sectors that rely more heavily on foreign inputs from countries that faced stronger disruptions experienced larger increases in PPI inflation.

This article complements a short but growing literature on inflation and supply chain disruptions. Ha, Kose, and Ohnsorge (2021) analyze the driving forces of global inflation, focusing on the 2020 global recession. Comin and Johnson (2020) study the role of trade integration and offshoring on inflation. Leibovici and Dunn (2021) discuss the extent to which supply chain disruptions account for the recent rise in inflation, focusing on the case of semiconductors. Finally, Amiti, Heise, and Wang (2021) study the effects of rising import prices on U.S. producer prices.

Citation

Ana Maria Santacreu and Jesse LaBelle,

ldquoGlobal Supply Chain Disruptions and Inflation During the COVID-19 Pandemic,rdquo

Federal Reserve Bank of St. Louis

Review,

Second Quarter 2022, pp. 78-91.

https://doi.org/10.20955/r.104.78-91

Editors in Chief

Michael Owyang and Juan Sanchez

This journal of scholarly research delves into monetary policy, macroeconomics, and more. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System. View the full archive (pre-2018).

Email Us