Why Is Inflation So Low?

KEY TAKEAWAYS

- If low inflation persists, this would raise questions about the central bank’s commitment to its inflation target and increase the risk of deflation.

- The U.S. isn’t the only country facing this issue. Other developed countries are dealing with low inflation.

- Technological and demographic changes may be likely reasons, although some hypotheses link low inflation to monetary policy.

The U.S. inflation rate has been below the Fed’s 2 percent inflation target since 2012. In this article, we revisit the merits of some of the most common explanations for the current low inflation rate.

While a moderate inflation rate can be beneficial for the economy, there are several reasons to be concerned about very low inflation. First, an inflation rate lower than the 2 percent target for a long period of time may signal that the monetary authority does not have inflation under control or that its commitment to the target is not that strong. Second, very low inflation is typically associated with an increased probability of falling into deflation, in which prices and wages are declining on average. Deflation, in turn, is a phenomenon associated with weak economic conditions.

The prime example of the aforementioned concerns is Japan. Since the late 1990s, Japan has experienced a long period of low inflation that is associated with a secular stagnation. In past years, low inflation in the U.S. triggered concern that the country may be heading to a Japanese-style low inflation trap.1

Because inflation cannot be measured by an increase in the price of one product or service, or even several products or services, there are many different indexes to measure inflation, each index signaling different information about inflation. The Federal Open Market Committee (FOMC), the Fed’s main monetary policymaking body, prefers to look at personal consumption expenditures (PCE) because, among other reasons, the PCE price index covers a wide range of household spending.

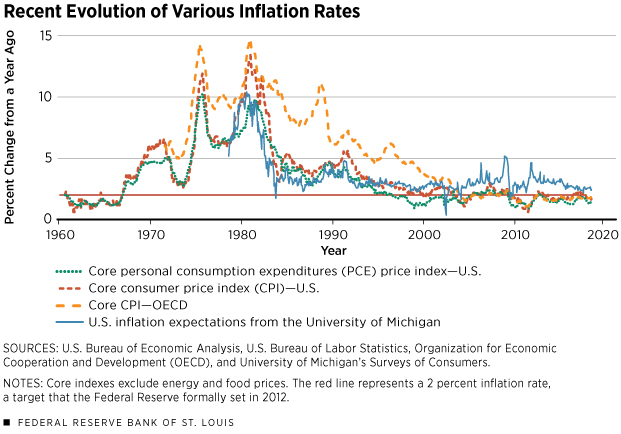

Figure 1 displays the recent evolution of the core PCE and core consumer price indexes (CPI) for the U.S. since the 1960s. Both indexes are seasonally adjusted and are computed as a year-over-year percentage change. It is also important to note that these indexes are “core” indexes, which exclude food and energy items that fluctuate dramatically. Looking at core indexes, rather than focusing on a short episode of spikes in inflation, helps to observe the inflation trend.2 The PCE inflation in November 2017 was 1.5 percent, well below the inflation target of 2 percent.

Low inflation not only is a phenomenon observed in the United States, but also has been a concern around the world. Figure 1 includes the average core CPI for countries in the Organization for Economic Cooperation and Development (OECD). While the average inflation rate in OECD countries has historically been higher than the inflation rate in the U.S., inflation in these two areas has been sluggish in recent years, with CPI in OECD countries hitting 1.9 percent in October 2017 and CPI in the U.S. hitting 1.7 percent in November 2017.

Finally, Figure 1 also includes inflation expectations from the University of Michigan’s Surveys of Consumers. It shows that expectations have also been on a declining trend since 2011 but remain above the target, at 2.5 percent in November 2017.

Technological Progress

Alan Greenspan, then chairman of the Federal Reserve, stated in testimony before the U.S. Congress in 2005: “The past decade of low inflation and solid economic growth in the United States and in many other countries around the world … is attributable to the remarkable confluence of innovations that spawned new computer, telecommunication, and networking technologies, which, especially in the United States, have elevated the growth of productivity, suppressed unit labor costs, and helped to contain inflationary pressures.”

His idea, echoing the voices of many other economists, is that technological advancement has brought down the price of goods that use new technologies intensively. Indeed, innovation of smart electronic gadgets like smartphones has reduced the demand for various other gadgets, exemplified by the fact that the smartphones today can provide better cameras than professional equipment a decade ago. According to the U.S. Bureau of Labor Statistics, prices of general tuition and medical care have risen 29 percent and 25 percent, respectively, while prices of television and photographic equipment have decreased 73 percent and 24 percent, respectively, since 2010.

Arguably, technological advancement has also increased labor productivity, therefore reducing unit labor cost. With the help of easily accessible information, improved communication, and useful software/applications, it is not too hard to imagine that the recent advances in technology have contributed to improved productivity.

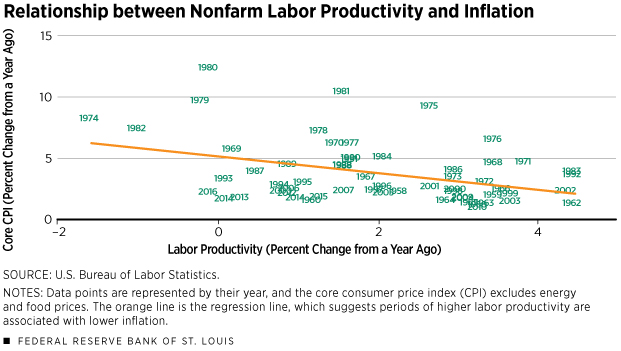

Figure 2 reports the correlation between labor productivity in nonfarm business and core CPI in the United States. The downward trend illustrates that periods with higher labor productivity are associated with lower inflation. According to the estimated relationship, an increase in labor productivity of 3 percentage points is associated with a reduction in inflation by approximately 2 percentage points.

Economists Ian Dew-Becker and Robert J. Gordon have argued that indeed the slowdown in productivity growth had major effects in boosting inflation during 1965-1979, while a hike in productivity growth between 1995 and 2005 had played a role in low inflation.

But why would inflation be low now if productivity has not grown faster than before? The most recent wave of technological progress that has drawn attention among economists is the “sharing economy.”

While there is no consensus on the exact definition of the term, the sharing economy usually refers to the idea of a crowd-based market that allows the exchange of privately owned goods and services. Airbnb and Uber are prime examples of the sharing economy. Although it is not easy to see this in the official productivity statistics, it is clear that the rise of the sharing economy has improved productivity by allowing for the utilization of otherwise idle goods and services, which then has led to the reduction in prices.

For example, economists Georgios Zervas, Davide Proserpio and John Byers studied the impact of the introduction of Airbnb into the Texas market. They reported that Airbnb’s entry into the hospitality market has had a quantifiable negative impact on local hotel room prices, with lower-end hotels and hotels not catering to business travelers being most vulnerable to the increased competition from Airbnb. They have estimated that a 10 percent increase of Airbnb rooms is associated with a 0.39 percent decrease in hotel room revenue, whereas a 10 percent increase in the supply of hotel rooms has resulted in a 1.6 percent reduction in hotel room revenue; this implies that the effects of introducing Airbnb are about one-fourth that of creating new hotel rooms. With a massive surge of Airbnb rooms opening recently, this impact is non-negligible.

Demographic Transitions

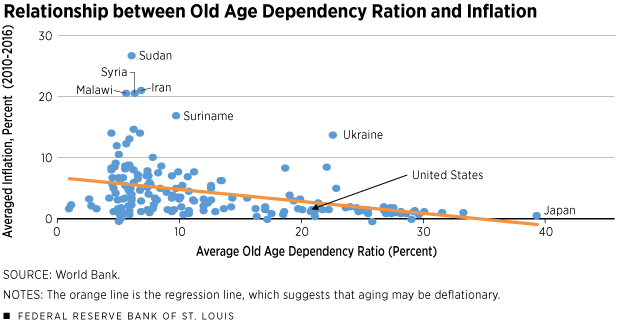

It is incontrovertible that the population of the world’s developed economies is living a longer life, and the age demographic is shifting upward. How does this shift in population demographic affect inflation? Figure 3 reports cross-country correlation between average inflation and the average old age dependency ratio between 2010 and 2016.3 Old age dependency ratio is calculated as the ratio of population aged 65 and above to the population aged 15 to 64.

The negative correlation suggests that aging may be deflationary. Notice that in Figure 3, Japan has the highest old age dependency ratio and one of the lowest inflation rates. Indeed, there is a string of literature that studies how the aging Japanese labor force is associated with low inflation.

A study by economists Shigeru Fujita and Ippei Fujiwara explores a causal link between aging of the labor force and deflationary pressure in Japan. Their argument is that in an economy where skills are very specific to each individual firm, a growing share of old workers who lose their jobs also lose their firm-specific skills and flow into entry-level jobs. This inflow of old workers to entry-level jobs negatively impacts young workers’ wages, creating deflationary pressure in the long run.

While the effect of longevity is clear, there is certain disagreement about the effect of changes in the birth rate. On the one hand, economists Mitsuru Katagiri, Hideki Konishi and Kozo Ueda argue that the effect of aging depends on its causes. Their model concludes that aging is deflationary when caused by an increase in longevity but inflationary when caused by a decline in the birth rate. On the other hand, economist Pawel Gajewski extends the analysis to OECD countries and argues that a decline in the birth rate is also deflationary in the data.4

How does this Japanese experience translate to the U.S.? We have measured the effects of the young age dependency ratio (the ratio of the population aged 0-14 to the population aged 15-64) and the old age dependency ratio on U.S. inflation using the coefficients obtained by Gajewski. Between 1960 and 2016, the old age dependency ratio increased by about 50 percent, and the young age dependency ratio decreased by about 43 percent in the U.S.

Focusing on the post-crisis period from 2010 to 2016 that experienced persistent low inflation, both decreasing young age dependency and increasing old age dependency are associated with a 0.1 percentage point decrease in inflation annually. Since inflation was lower than the target by 0.4 percentage points on average during that period, about 25 percent of the difference could be accounted for by the changes in demographics since 2010.

Globalization

As noted above, low inflation is not uniquely observed in the United States. While some countries, notably Argentina and Venezuela, have suffered from very high inflation in recent years, many of the developed countries are experiencing persistent low inflation. Some economists have argued that widespread low inflation may be due to globalization. Particularly, economists Claudio Borio and Andrew Filardo argue that current inflation models are too “country-centric,” failing to acknowledge the growing role of global factors on the inflation process. They point out that the sensitivity of inflation to domestic output gaps (the difference between current output and potential output) has been falling, while the importance of global output gaps has been increasing.

The significance of globalization’s impact on inflation is at least debatable, however. The World Economic Outlook report in 2006 from the International Monetary Fund (IMF) describes that the direct effect of globalization on inflation through import prices has, in general, been small in the industrial economies. In addition, speeches by Federal Reserve Chair Janet Yellen and former Federal Reserve Vice Chairman Donald Kohn also stressed that the impact of foreign factors on U.S. prices is rather limited.

One of the factors that may explain this is that the exchange rate in cheap-labor countries would eventually appreciate as real wages catch up to past gains in productivity. Along the same lines, more recent empirical papers that analyze cross-country data seem to conclude that globalization has a limited influence on a country’s inflation. A study of 11 developed countries by economists Jane Ihrig, Steven Kamin, Deborah Lindner and Jaime Marquez produced no meaningful evidence for the globalization hypothesis, which asserts that the internationalization of goods and financial markets has been changing the determinants of national macroeconomic outcomes such as inflation.

Another study that observed 50 countries around the world also concluded that while global economic fluctuations affect the dynamic of domestic inflation, foreign output gaps are still not as important as domestic output gaps, and trade openness is still too small to justify significant brakes in inflation dynamics.5

Inflation Targeting and Central Bank Independence

What if inflation is simply very low because monetary policy is too tight? There are at least two reasons to believe that this hypothesis may be relevant. First, inflation targeting has become widespread since its introduction in 1989 by New Zealand. Nine advanced economies and 21 emerging market economies are now “inflation targeters.”6 This means that a growing number of countries are making inflation the primary goal of monetary policy. Not surprisingly, this results in lower rates of inflation. Although inflation targeting does not necessarily imply inflation that is too low, the fact that inflation lower than the target is often considered better than inflation higher than the target may contribute to an inflation rate that, on average, is lower than the target.

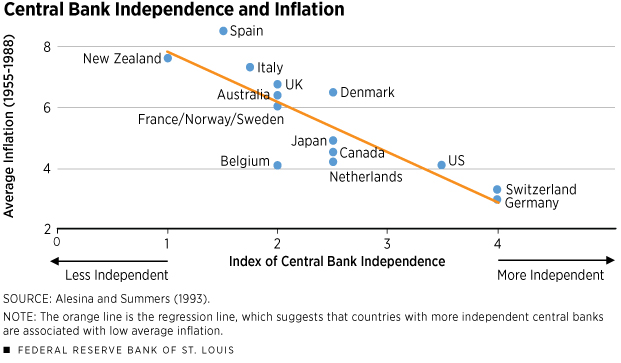

The second reason is central bank independence, which is closely related to inflation targeting. The fact that central banks can focus solely on reducing inflation depends crucially on their ability to act independently. Indeed, economists Alberto Alesina and Lawrence Summers have empirically shown a negative relationship between inflation and central bank independence by devising indexes to measure the autonomy of the central bank.7 This clear negative relationship is shown in Figure 4. It suggests that countries with more-independent central banks are associated with low inflation.

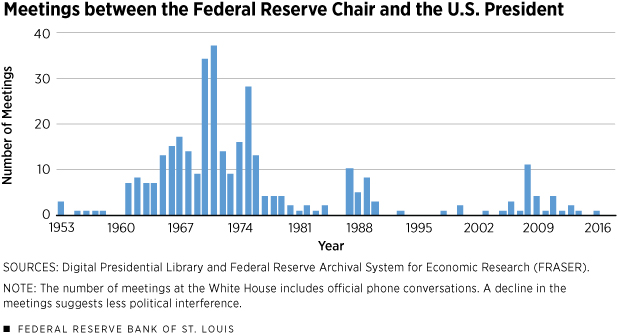

Why is this relevant today? Because the number of countries that are inflation targeters has been increasing, and central banks have become more independent. In particular, the index of central bank independence proposed by economist Fernando Martin, which counts the number of meetings between the chair of the Federal Reserve and the U.S. president, shows a clear downward trend in the U.S., as shown in Figure 5.

Neo-Fisherism

Finally, some economists have argued that the relationship between interest rates and expected inflation proposed by Irving Fisher implies that low policy rates for a long period of time must imply low inflation.8 The Fisher relationship indicates that the nominal interest rate can be approximated by the sum of the real interest rate and the expected inflation rate. In the past, this relationship has been interpreted to mean that the real interest rate is the independent variable. Thus, the expected inflation rate has a unidirectional causal relationship with the nominal interest rate, that is, a higher expected inflation rate will result in a rising nominal interest rate.

However, in an environment in which the monetary authority keeps the relevant nominal interest rate very close to zero for a long period of time, this relationship would simply imply that the expected inflation rate is equal to the negative of the real rate. Recall that under the Fisher hypothesis, the real rate is independent of monetary policy (it depends on factors like long-term economic growth). Thus, if the real rate is close to zero, it must be that, under this hypothesis, expected inflation is close to zero as well. The solution to low inflation in this context is to increase the nominal interest rate.

Some evidence for this argument is derived from Japan, where the nominal interest rate has been close to zero since the late 1990s, and the inflation rate shows no sign of increasing.9

Conclusion

Overall, we find that there are several reasons pushing inflation down, not just in the U.S. but also in other developed countries. The new sharing economy and the demographic transition come up as the most likely explanations. However, it is hard to rule out that long periods of near zero policy rates have implied that only low expected inflation is compatible with the current fundamentals of the economy.

Endnotes

- See Bullard, 2010. [back to text]

- However, some economists proposed that the FOMC should focus more on headline inflation. See Bullard, 2011. [back to text]

- South Sudan and Venezuela are excluded from the sample because both countries experienced a hyperinflation, in which averaged inflation was greater than 80 percent between 2010 and 2016. [back to text]

- See Canon, Kudlyak and Reed for more details. [back to text]

- See Bianchi and Civelli. [back to text]

- See presentation by Murray. [back to text]

- See Cukierman et al., among many others, for more details. [back to text]

- See Williamson, 2016. [back to text]

- See Cochrane, and Williamson (forthcoming). [back to text]

References

Alesina, Alberto; and Summers, Lawrence H. Central Bank Independence and Macroeconomic Performance: Some Comparative Evidence. Journal of Money, Credit and Banking, 1993, Vol. 25, No. 2, pp. 151-62.

Bianchi, Francesco; and Civelli, Andrea. Globalization and Inflation: Evidence from a Time-Varying VAR. Review of Economic Dynamics, 2015, Vol. 18, No. 2, pp. 406-33.

Borio, Claudio; and Filardo, Andrew. Globalization and Inflation: New Cross-Country Evidence on the Global Determinants of Domestic Inflation. BIS Working Papers No. 227.

Bullard, James. Seven Faces of “The Peril.” Federal Reserve Bank of St. Louis Review, 2010, Vol. 92, No. 5, pp. 339-52.

Bullard, James. Measuring Inflation: The Core Is Rotten. Federal Reserve Bank of St. Louis Review, 2011, Vol. 93, No. 4, pp. 223-33.

Canon, Marie E.; Kudlyak, Marianna; and Reed, Marisa. Aging and the Economy: The Japanese Experience. The Regional Economist, Vol. 23, No. 4, pp. 12-13.

Cochrane, John H. Do Higher Interest Rates Raise or Lower Inflation? Unpublished manuscript, February 2016. See https://faculty.chicagobooth.edu/john.cochrane/research/papers/fisher.pdf.

Cukierman, Alex; Webb, Steven B.; and Neyapti, Bilin. Measuring the Independence of Central Banks and Its Effect on Policy Outcomes. The World Bank Economic Review, 1992, Vol. 6, No. 3, pp. 353-98.

Dew-Becker, Ian; and Gordon, Robert J. Where Did the Productivity Growth Go? Inflation Dynamics and the Distribution of Income. NBER Working Paper 11842.

Fujita, Shigeru; and Fujiwara, Ippei. Aging and Declining Trends in the Real Interest Rate and Inflation: Japanese Experience. Unpublished manuscript, August 2015. See http://cepr.org/sites/default/files/Fujiwara%20-%20FF August2015.pdf.

Gajewski, Pawel. Is Ageing Deflationary? Some Evidence from OECD Countries. Applied Economics Letters, 2015, Vol. 22, No. 11, pp. 916-19.

Greenspan, Alan. Economic Outlook. Nov. 3, 2005. See www.federalreserve.gov/boarddocs/testimony/2005/20051103/default.htm.

Helbling, Thomas; Jaumotte, Florence; and Sommer, Martin. How Has Globalization Affected Inflation? World Economic Outlook, April 2006, pp. 97–134.

Ihrig, Jane; Kamin, Steven B.; Lindner, Deborah; and Marquez, Jaime. Some Simple Tests of the Globalization and Inflation Hypothesis. International Finance, 2010, Vol. 13, No. 3, pp. 343-75.

Katagiri, Mitsuru; Konishi, Hideki; and Ueda, Kozo. Aging and Deflation from a Fiscal Perspective. Federal Reserve Bank of Dallas Working Paper No. 218. November 2014.

Kohn, Donald L. The Effects of Globalization on Inflation and Their Implications for Monetary Policy. June 16, 2006. See www.federalreserve.gov/newsevents/speech/kohn20060616a.htm.

Martin, Fernando M. Debt, Inflation and Central Bank Independence. European Economic Review, 2015, Vol. 79, pp. 129-50.

Murray, John. Inflation Targeting After 28 Years: What Have We Learned? Jan. 16, 2017. See www.regjeringen.no/contentassets/adcde72c116c4804b50e8e44b851569e/1_murray.pdf

Williamson, Stephen. Neo-Fisherism: A Radical Idea, or the Most Obvious Solution to the Low-Inflation Problem? The Regional Economist, 2016, Vol. 24, No. 3, pp. 5-9.

Williamson, Stephen. Inflation Control: Do Central Bankers Have It Right? Forthcoming in Federal Reserve Bank of St. Louis Review.

Yellen, Janet. Monetary Policy in a Global Environment. May 27, 2006. See www.frbsf.org/our-district/press/presidents-speeches/yellen-speeches/2006/may/monetary-policy-in-a-global-environment.

Zervas, Georgios; Proserpio, Davide; and Byers, John W. The Rise of the Sharing Economy: Estimating the Impact of Airbnb on the Hotel Industry. Journal of Marketing Research, 2017, Vol. 54, No. 5, pp. 687-705.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us