Millennials and Gen Z Are Not Doomed to Rent Forever

By William R. Emmons

KEY TAKEAWAYS

- U.S. households headed by someone 18 to 39 years old in 2019 are more likely to be renters today than their same-aged counterparts were in 2004.

- Millennials are closer to the historical norm for homeownership for their current ages than the typical member of Generation X was in 1994.

- The high share of young adults that rents today doesn’t suggest the Great Recession or other events have pushed them far off course.

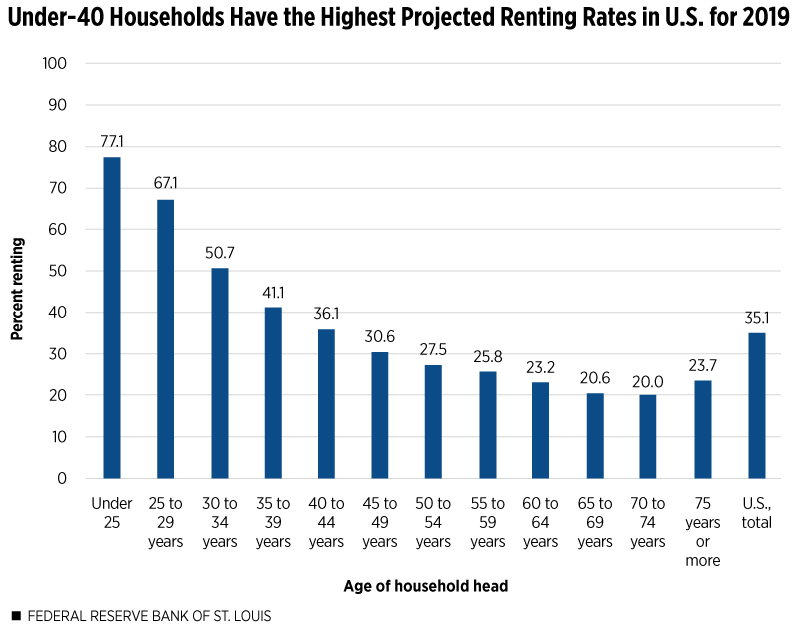

Most U.S. households headed by someone under 35 are renters. (See Figure 1.) Many young adults rent because they are not financially ready to be homeowners, or they have not yet settled where they want to buy a house. The rising cost of higher education, the job-market impact of the Great Recession, and rapidly rising house prices in some areas also may have pushed more young people into renting in recent years.

But a large majority of all previous generations born in the 20th century transitioned into homeownership as they moved into middle age. Will today’s young adults be different?

NOTES: In the bar graph, millennial households are covered by the age groups 25-29, 30-34 and 35-39, with rental rates of 67.1, 50.7 and 41.1 percent, respectively. The under 25 bar is the tallest, showing that 77.1 percent of very young households rent.

SOURCE: Author’s projections for 2019 based on Census Bureau annual data through 2018.

Millennials Are Renting More than Young Adults Did in 2004

As of 2016, the typical household headed by someone born in the 1980s (a millennial) appeared to be seriously behind all previous generations at a similar age in accumulating wealth.See William R. Emmons, Ana H. Kent and Lowell R. Ricketts, “A Lost Generation? Long-Lasting Wealth Impacts of the Great Recession,” The Demographics of Wealth 2018 Series, May 2018, https://www.stlouisfed.org/household-financial-stability/the-demographics-of-wealth/wealth-impacts-of-great-recession-on-young-families. A decline in the apparent income- and wealth-boosting power of higher education, due to a variety of causes, also darkens the outlook for this group.See William R. Emmons, Ana H. Kent and Lowell R. Ricketts, “Is College Still Worth It? It’s Complicated,” On the Economy blog, Feb. 7, 2019, https://www.stlouisfed.org/on-the-economy/2019/february/is-college-still-worth-it-complicated.

Getting off to a slow start financially may translate into permanently lower levels of attaining goals like homeownership for many millennials. In Figure 1, millennial households—which we define as birth years 1980 through 1994—are covered by the age groups 25-29, 30-34 and 35-39. Compared to the shares of each age group that rented in 2004, current renting shares are 7.3 to 8.1 percentage points higher.

Among those born in 1995 or later, known as Generation Z, it’s too soon to make confident predictions about their economic future. But the 77.1 percent of very young households that rent today (see the under-25 bar in Figure 1) is 2.3 percentage points higher than the renting share among under-25 households in 2004.

Under-40 Group Escaped the Worst Recession Housing Effects

It’s true that broad measures of the financial strength of millennials, including median household wealth and the homeownership rate, are weaker today than the same measures for previous generations when they were the same ages in 2004. But a longer view that takes a generational perspective reveals that millennials and members of Gen Z may not be doomed to “rent forever,” or, more precisely, achieve historically low homeownership rates at each age in their life cycles. (The table shows how old the various generations discussed here were in several important years.)

| Generation | Age | ||

|---|---|---|---|

| 1994 | 2004 | 2019 | |

| Baby boomers: born 1945-64 | 30-49 | 40-59 | 55-74 |

| Gen X: born 1965-79 | Under 30 | 25-39 | 40-54 |

| Millennials: born 1980-94 | Under 25 | 25-39 | |

| Gen Z: born 1995 or later | Under 25 | ||

The key point is that people born in 1980 or later generally were too young to experience directly the worst housing effects of the housing bubble and the Great Recession, including the millions of mortgage foreclosures and other involuntary exits from homeownership. While today’s under-40 group is undoubtedly off to a slow start financially, they do not carry the financial scars that previous generations do. In particular, members of Generation X and younger baby boomers appear much more likely to fall short of the financial benchmarks laid down by previous generations at each stage of their life cycles.

A Generational Perspective Helps Peer through the Housing Bubble

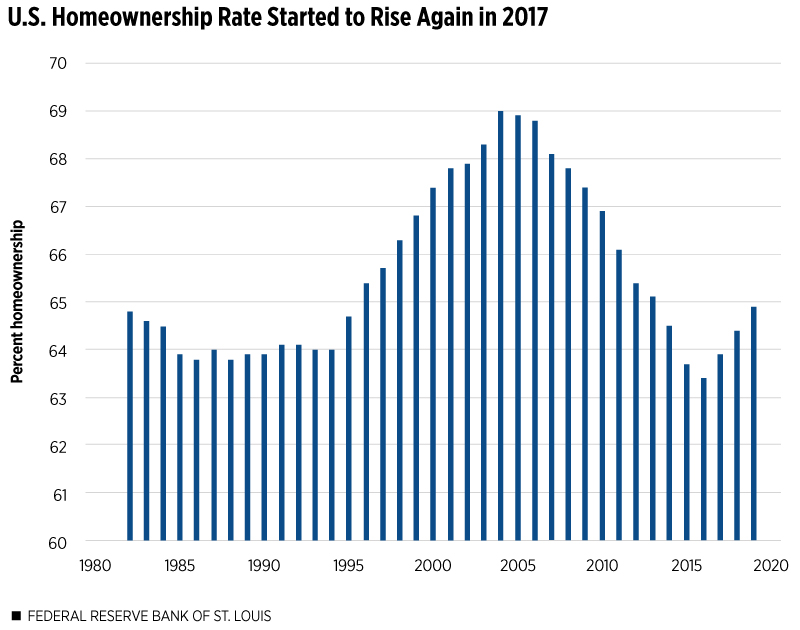

The national homeownership rate began to rise notably after 1994. (See Figure 2.) The share of renting households is simply 100 minus the homeownership rate. I designated 1994 as the last pre-bubble year based on the subsequent rapid rise of the homeownership rate and 2004, when the homeownership rate reached 69.0 percent, as the peak of the housing bubble.

NOTES: The bar graph shows homeownership rates from 1982 to 2019 and has a y-axis with a 60 percent to 70 percent range. Peak homeownership, 69 percent, is in 2004, with rates declining until 2016, when the rate was 63.4 percent, before starting to rise again.

SOURCES: U.S. Census Bureau for annual data, 1982-2018; author’s projections for 2019 based on census annual data through 2018.

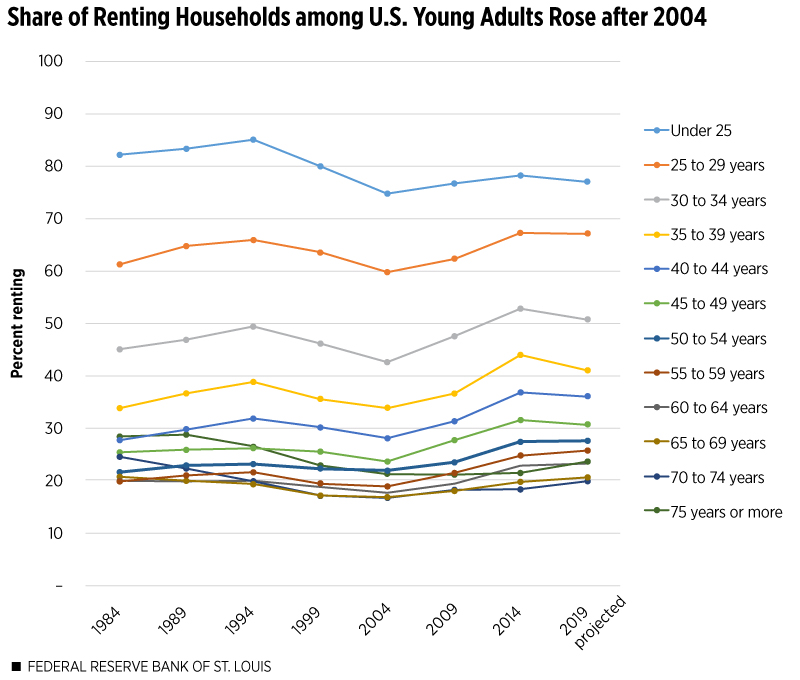

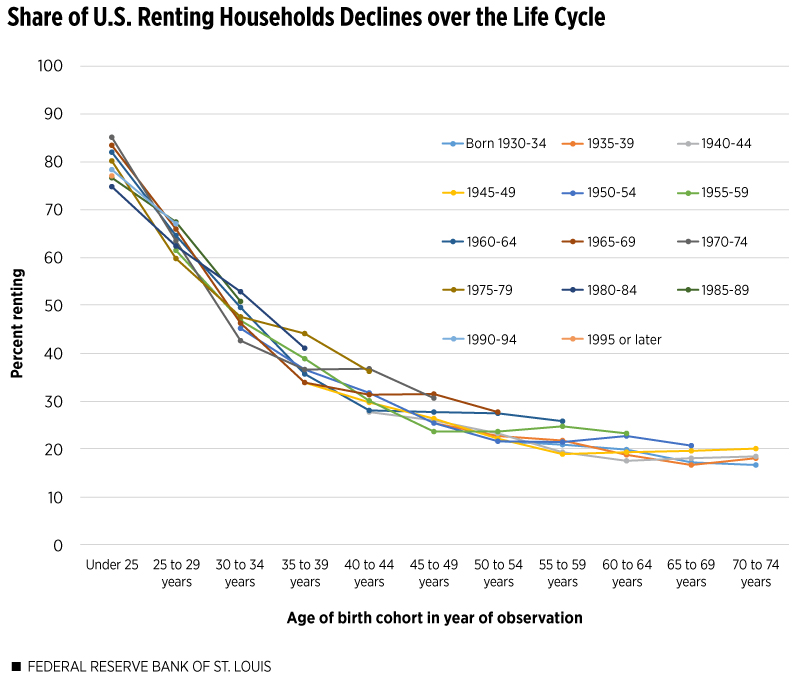

To transform the five-year age ranges available in census homeownership data precisely into generational terms, I concentrated on each cohort’s share of renting households at five-year intervals beginning in 1984. Figure 3 shows the untransformed census rental-share data by age group; Figure 4 displays the data from a generational perspective, as each birth cohort’s path of actual rental shares declines over the life cycle.

NOTES: A line graph shows the untransformed census rental-share data by age group, with each cohort’s share at five-year intervals beginning in 1984. The under-25 age group has the highest rental rate across all years. The share of renting households in all age groups declined for 10 years starting in 1994 and started to rise after 2004.

SOURCES: Census Bureau for annual data, 1984-2014; author’s projections for 2019 based on census annual data through 2018.

NOTE: Figure 4 displays data from a generational perspective, showing each birth cohort’s path of actual rental shares declining over the life cycle.

SOURCES: Census Bureau for annual data, 1984-2014; author’s projections for 2019 based on census annual data through 2018.

Gen X Has the Largest Increases in Rental Share

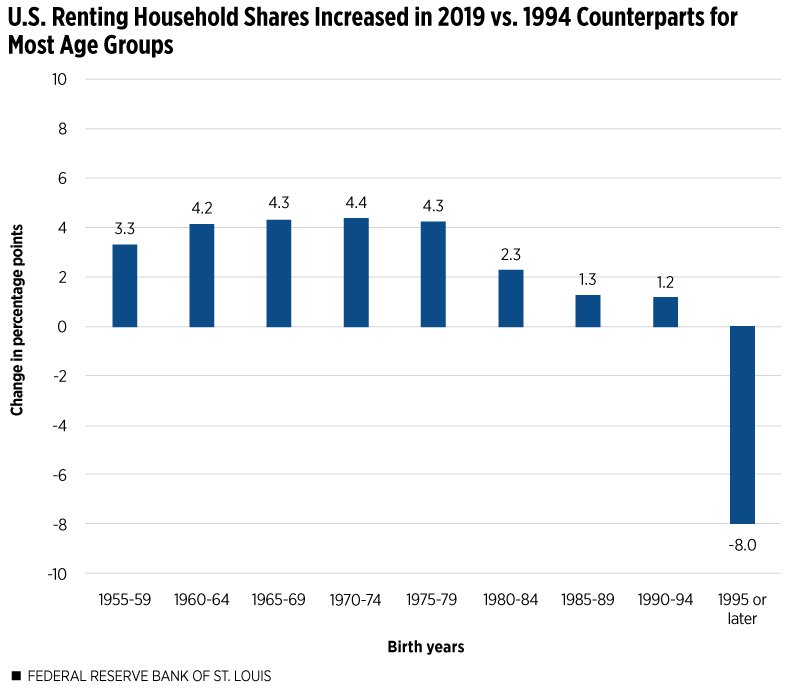

Figure 5 shows that the largest increases in the renting share of households as of 2019—compared to the share of renters at matched ages precisely 25 years earlier, in 1994—are among members of Generation X (born 1965-79) and, with somewhat smaller increases, younger baby boomers (born 1955-64).It is not possible to make these comparisons for cohorts born before 1955 because age-specific homeownership data do not reach back far enough. Millennials (born 1980-94) rent at a slightly higher rate than their same-age counterparts 25 years earlier, while members of Gen Z actually are much less likely to rent than their same-age peers in 1994.Comparing the homeownership rates of very young households at different times is complicated by the fact that household formation rates among young adults vary greatly over time. For example, the number of households headed by someone under 25 increased by 25.6 percent between 1994 and 2004, even though the number of adults aged 16-24 increased by only 11.9 percent (U.S. Census Bureau). Between 2004 and 2018, the number of under-25 households decreased by 6.0 percent while the number of adults aged 16-24 increased by 4.4 percent.

NOTES: A bar graph shows percentage point changes in the share of renting households in 2019 compared to the same age groups in 1994. The largest increases of 4.3 and 4.4 percentage points are among members of Generation X and, with increases of 3.3 and 4.2 percentage points, younger baby boomers (born 1955-64). Millennials rent at a slightly higher rate than their same-age counterparts 25 years earlier, while members of Gen Z are 8 percentage points less likely to rent than their same-age peers in 1994.

SOURCES: Census Bureau for annual data, 1984-2014; author’s projections for 2019 based on census annual data through 2018.

A generational perspective on the recent rise in the share of young households that rent therefore reveals that millennials and members of Gen Z are not far away from the longer-term norm that excludes the housing bubble. Members of Gen X and younger baby boomers, on the other hand, appear to have suffered more disruption in their housing patterns as a result of the housing crash. Despite a relatively high share of under-40 households that rent today, we should not expect them to be forced to “rent forever.”

Endnotes

- See William R. Emmons, Ana H. Kent and Lowell R. Ricketts, “A Lost Generation? Long-Lasting Wealth Impacts of the Great Recession,” The Demographics of Wealth 2018 Series, May 2018, https://www.stlouisfed.org/household-financial-stability/the-demographics-of-wealth/wealth-impacts-of-great-recession-on-young-families.

- See William R. Emmons, Ana H. Kent and Lowell R. Ricketts, “Is College Still Worth It? It’s Complicated,” On the Economy blog, Feb. 7, 2019, https://www.stlouisfed.org/on-the-economy/2019/february/is-college-still-worth-it-complicated.

- It is not possible to make these comparisons for cohorts born before 1955 because age-specific homeownership data do not reach back far enough.

- Comparing the homeownership rates of very young households at different times is complicated by the fact that household formation rates among young adults vary greatly over time. For example, the number of households headed by someone under 25 increased by 25.6 percent between 1994 and 2004, even though the number of adults aged 16-24 increased by only 11.9 percent (U.S. Census Bureau). Between 2004 and 2018, the number of under-25 households decreased by 6.0 percent while the number of adults aged 16-24 increased by 4.4 percent.

This article originally appeared in our Housing Market Perspectives publication.

Citation

ldquoMillennials and Gen Z Are Not Doomed to Rent Forever,rdquo St. Louis Fed On the Economy, March 25, 2019.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions