Real-Life Examples of Opportunity Cost

What do economists think about strawberry smoothies? That depends on how good the kiwi flavor is instead—plus a range of other choices. Which stirs up the idea of opportunity cost.

How is opportunity cost defined in everyday life?

“Opportunity cost is the value of the next-best alternative when a decision is made; it's what is given up,” explains Andrea Caceres-Santamaria, senior economic education specialist at the St. Louis Fed, in a recent Page One Economics: Money and Missed Opportunities.

The Scoop on Scarcity

We can’t have everything we want in life. This is where scarcity factors in. Our unlimited wants are confronted by a limited supply of goods, services, time, money and opportunities. This concept is what drives choices—and, by extension, costs and trade-offs, Caceres-Santamaria says.

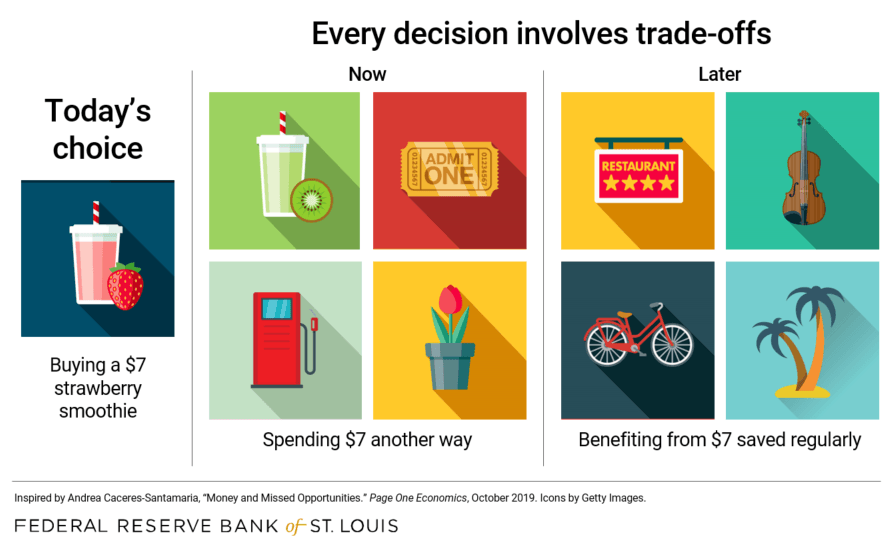

She uses the example of deciding to buy a $7 smoothie at the mall. She notes that many people would view the choice as a single one based on whether you want the drink.

Instead, she suggests wearing “a unique pair of ‘economist glasses’” to see the decision differently, asking:

- How much do I value this?

- What am I giving up now to have this?

- What am I giving up in the future to have this now?

Costs That Are Seen and Unseen

Our inclination is to focus on immediate financial trade-offs, but trade-offs can involve other areas of personal or professional well-being as well—in the short and long run.

That’s why Caceres-Santamaria challenges us to consider not only explicit alternatives—the choices and costs present at the time of decision-making—but also implicit alternatives, which are “unseen” opportunity costs.

“It's about thinking beyond the present and assessing alternative uses for the money—that is, not being shortsighted,” she writes.

What are some other examples of opportunity cost?

- A student spends three hours and $20 at the movies the night before an exam. The opportunity cost is time spent studying and that money to spend on something else.

- A farmer chooses to plant wheat; the opportunity cost is planting a different crop, or an alternate use of the resources (land and farm equipment).

- A commuter takes the train to work instead of driving. It takes 70 minutes on the train, while driving takes 40 minutes. The opportunity cost is an hour spent elsewhere each day.

Is Opportunity Cost a Big Deal?

We might not consider lost studying time or $7 spent on a smoothie costly decisions, but what about bigger choices—like the decision to stretch and buy a more expensive home versus a starter home, or to spend $1,500 more on an upgraded trim package for your next car?

Caceres-Santamaria describes how opportunity costs are neglected even more when making higher priced purchases. Using the car-buying example, a consumer might default to thinking of the relative value of the $1,500 upgrade to the base price of the car, say, $18,500.

Rather than comparing the fancier configuration to the vehicle itself, it might be more helpful to ask what else that $1,500 could buy outright.

Why the Rush?

“Most of our decisionmaking that involves money is based on immediate or sooner-than-later consumption,” Caceres-Santamaria notes. “The excitement of consuming today is valued significantly more than the thought of consuming in the future.”

It’s human nature: We grow impatient, tugged by the immediacy of a promised benefit versus a payoff that’s possibly years down the road.

If seeing is believing, it’s worth looking at the future value of money—a concept many of us have read about in retirement plan literature or heard from financial advisors.

The Future Value of Money

Example 1: The one-time windfall

Let’s say you got a surprise $4,000 windfall and want to use it for a getaway trip. Why not? It’s found money, so there’s no loss to you—unless you think about the opportunity cost.

If you nixed the trip and plunked your money into an income-producing product that earned an average annual interest rate of 3%, compounded monthly, you could find yourself with a cool $5,397 in 10 years.

Notes: Chart is for illustrative purposes only. Created with Compound Interest Calculator on Investor.gov

Wait another five years, and your funds could grow to $6,270. (Neither example factors in the effects of inflation and taxes owed.)

That’s the added benefit in money terms. You’ll also want to consider the experiences that an extra $1,400 or more—the future earnings on your $4,000—could make possible.

Example 2: Small, regular savings over time

That’s an example of investing a single lump sum over time. What about the opportunity cost associated with daily purchases, such as the $4.49 caffè mocha you pick up three times a week? How much money could you find yourself with if investing that $54 each month rather than spending it?

If you dropped the coffee (careful!), invested $54 per month and earned the same 3%, compounded monthly, you’d have $7,619 to dunk your doughnut into in 10 years.

Notes: Chart is for illustrative purposes only. Created with Compound Interest Calculator on Investor.gov

Too long to forego that regular mocha? Cutting the time frame in half to five years would still give you $3,554 in savings. (Again, these sums don’t include the impact of inflation and taxes.)

These examples are striking, especially when considering that a $4.49 caffè mocha habit over time can dwarf the seemingly larger decision to splurge on a $4,000 getaway trip.

Want to test some of your own opportunity cost what-ifs? Caceres-Santamaria encourages consumers to avoid “autopilot” mode when it comes to financial decisions. Start small—even with a pack of gum—and brainstorm as many alternative uses for your money as you can.

Additional Resources

- Opportunity Cost - Online Course for Consumers

- There is No Such Thing as a Free Lunch

- How Does Compound Interest Work?

- Opportunity Cost - Economic Lowdown Podcast Series

This blog explains everyday economics and the Fed, while also spotlighting St. Louis Fed people and programs. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us