Excess Retirements Continue despite Ebbing COVID-19 Pandemic

During the COVID-19 pandemic, the U.S. labor force participation rate (LFPR) fell from 63.3% in February 2020 to 60.1% in April 2020, a 3.2 percentage point drop that was the largest on record. After a quick rebound, the LFPR remained 1.0 percentage point below its February 2020 level as of the end of 2022.

There are many reasons for why the LFPR may have fallen and failed to fully recover during this period. In this blog post, we explore one such potential explanation: the fact that people retired at greater numbers than what would have been expected under normal conditions.

Estimating Excess Retirements

A 2021 Economic Synopses essay by Miguel Faria e Castro covered the COVID-19 retirement boom, using trend analysis to compare actual retirees with the natural trend that results from the aging of the baby boomer generation (those born between 1946 to 1965). This simple model estimated that there were just over 2.4 million excess retirees as of August 2021.

In a forthcoming Review article,See our May 2023 working paper, “Pandemic Labor Force Participation and Net Worth Fluctuations,” for an earlier version of this work. we study the LFPR drop in greater detail, discussing how abnormal returns across financial asset classes may have contributed to excess retirements over the period of 2020-2022, and how much of the drop in LFPR can be attributed to these excess retirements. Further, we update the simple model of retirement in Faria e Castro’s 2021 essay, using the methodology from Joshua Montes, Christopher Smith and Juliana Dajon’s 2022 working paper (PDF).

In this post, we updated the results from our retirement model used in the Review article with the latest available data—April 2023—and investigated how the share of people retiring has compared with what we would expect under normal conditions in the final months of the COVID-19 emergency period, which ended in May 2023.

This updated model of retirement assumes that for a specific demographic group—defined as a combination of age, ethnicity, education and sex—the decision to retire depends on labor market conditions, the generosity of Social Security retirement benefits for that specific age group, and time trends that capture other secular changes to how different demographic groups approach labor market decisions.

We used these three factors to predict retirement shares for different demographic groups. We first divided the U.S. population into 780 demographic groups, with each subgroup being a combination of age (16 to 80 and older), sex (men and women), education (less than a bachelor’s degree, and a bachelor’s degree or more), and ethnicity (non-Hispanic white, non-Hispanic nonwhite, and Hispanic). For each of these 780 groups, we used a time trend, the unemployment gap, and the expected returns from Social Security to predict the expected share of retired people using historical, pre-COVID-19 data from 1995 to 2019.

The unemployment gap is simply the difference between the current unemployment rate and the natural rate of employment, as estimated by the Congressional Budget Office (CBO). We included this variable as there is a large body of research that finds that current labor market conditions affect people’s decision to participate in the labor force.

To calculate expected returns from Social Security, we calculated how much an individual would be penalized or rewarded for retiring at their current age. The Social Security Administration (SSA) provides information on your normal (full) retirement age—which is dependent on what year you were born—and the penalty or reward for retirement—which is based on how many months you are from the normal retirement age.The SSA provides a calculator to determine your benefits based on your birthdate and the month you want to start receiving benefits. We only calculated this variable for people in our sample who are ages 62 to 70, because 62 is the minimum age to begin receiving reduced benefits, and after 70 you can no longer accrue additional benefits from delaying retirement.

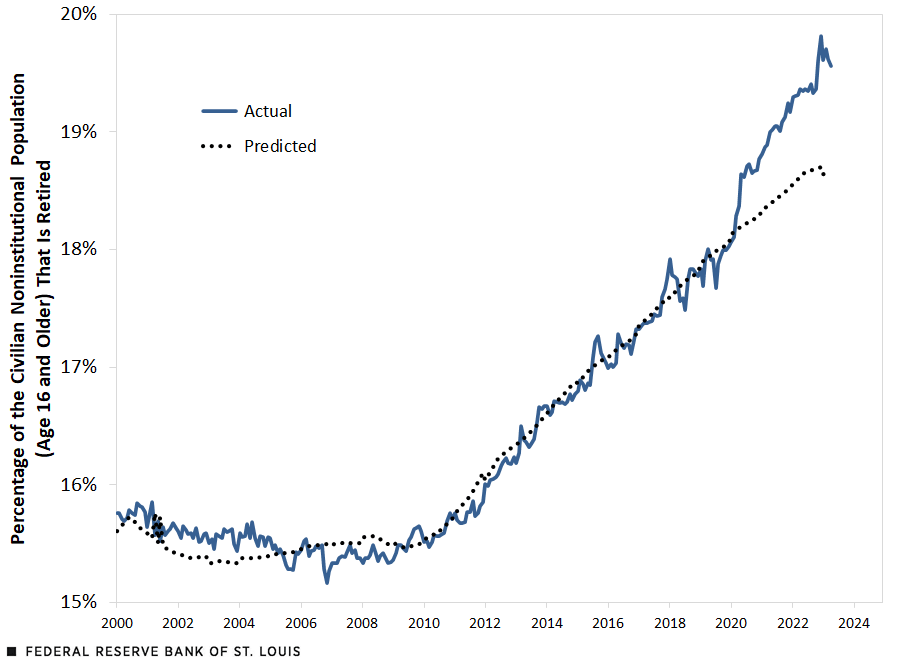

In the figure below, we compare the actual share of people who are retired, as a percentage of the civilian noninstitutional population age 16 and older, to our predicted share of retirements based on the model described above.

Actual Retirements Began to Greatly Surpass the Predicted Trend during the Pandemic

NOTES: The retirement shares are computed using Current Population Survey microdata with weights adjusted for changes in population controls as a result of the 2020 census. The model predicting the retirement share follows Montes, Smith and Dajon, 2022. Data are seasonally adjusted using the X13-ARIMA-SEATS procedure from the Census Bureau.

As shown in the figure, the actual share of retirements roughly tracked the predicted share from January 2000 through February 2020, when the actual share was 18.1%. In the first three months of the pandemic, however, actual share quickly increased to 18.6% versus a predicted share of 18.2%, implying just over one million excess retirees in May 2020.

The gap between actual and predicted shares of retirements continued to grow throughout the COVID-19 pandemic and peaked in December 2022, implying an estimated 2.95 million excess retirees in that month.

Starting in 2023, the model line begins to flatten out—meaning that predicted retirements are leveling off after consistently increasing from approximately 16% in 2012 to just over 18.6% in the first four months of 2023. In 2023, the actual share has also decreased since the peak of 19.8% in December 2022.

As of April 2023, we estimate that there were approximately 2.4 million excess retirees in the U.S. Excess retirements are still well above our predicted trend, which may be contributing to a continued tightness in the labor market and low unemployment rate since the recovery from the pandemic recession.

Notes

- See our May 2023 working paper, “Pandemic Labor Force Participation and Net Worth Fluctuations,” for an earlier version of this work.

- The SSA provides a calculator to determine your benefits based on your birthdate and the month you want to start receiving benefits.

Citation

Miguel Faria-e-Castro and Samuel Jordan-Wood, ldquoExcess Retirements Continue despite Ebbing COVID-19 Pandemic,rdquo St. Louis Fed On the Economy, June 22, 2023.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions