Viewing the U.S. Financial Structure from the Financial Crisis to the Pandemic

During the 2007-08 financial crisis and the current COVID-19 pandemic, the Federal Reserve had to take aggressive steps to protect the U.S. financial system. A recent Regional Economist article looked at how actions taken in the aftermath of the financial crisis shaped the U.S. financial system in the years leading to the pandemic.

Research Officer and Economist Fernando M. Martin examined shifts in assets held by key sectors in the U.S. economy from 2007 to 2019 and found that in some ways little changed.

“In the years following the financial crisis, liquidity was abundant and interest rates remained low; the financial sector underwent a significant regulatory overhaul and was subjected to even closer monitoring and supervision,” he wrote. “Yet, the overall financial structure of the U.S. changed remarkably little from 2007 to 2019.”

In his analysis, Martin grouped financial assets into six broad categories:

- Cash, reserves and deposits, which are the safest and most liquid assets in the economy

- Treasuries and agency- and GSE-backed securities, which are safe, liquid securities issued or backed by the federal government

- Other securities and shares of mutual funds, which consist of holdings of all other debt securities, mostly corporate and municipal bonds, plus shares of mutual funds, with the exception of money market funds

- Loans, which include mortgages and consumer credit

- Equities and foreign direct investment, which include corporate and noncorporate equity holdings

- Other assets, which group the remaining financial asset holdings

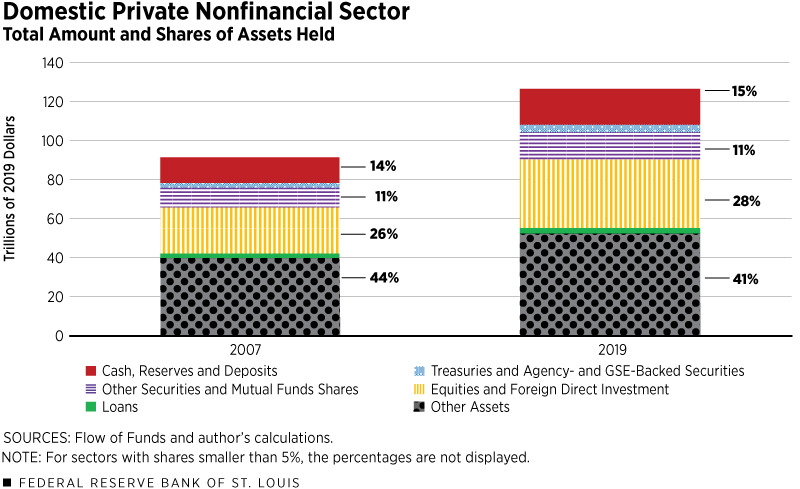

The Domestic Private Nonfinancial Sector

Martin first analyzed the domestic private nonfinancial sector, which comprises households, nonprofits and nonfinancial businesses.

Noting that this is the biggest of the three sectors he examined, the author said the sector’s total financial assets reached $127 trillion—six times the U.S. gross domestic product (GDP)—by December 2019. From 2007 to 2019, assets grew by 39% in real terms, outpacing the 22% growth in real GDP over the same period.

“Remarkably, when grouping asset holdings in the six main categories described above, little changed during those 12 years,” he wrote, referring to the figure below.

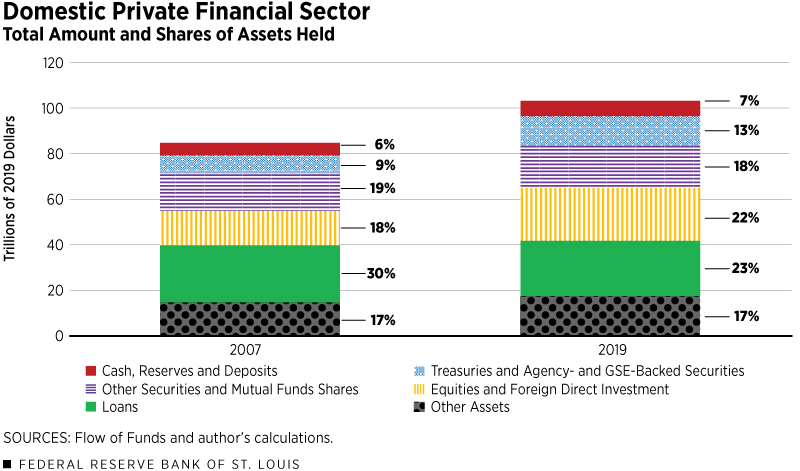

The Domestic Private Financial Sector

The author then examined the domestic private financial sector, which includes private depository institutions, insurance companies, private and public pension funds, mutual funds, government-sponsored enterprises and various other financial entities. This sector is slightly smaller; it held $104 trillion in assets as of December 2019. The sector grew at the same pace as GDP between 2007 and 2019.

In his analysis, Martin found that there was a shift toward safer and more liquid assets such as cash, reserves, deposits, Treasuries and agency- and GSE-backed securities. He also noted a shift toward corporate equity holdings.

“These increases occurred at the expense of a relative contraction in loans, which went from 30% to 23% of total financial assets,” he wrote.

The Foreign Sector and the “Flight to Safety”

Although the smallest of the three sectors, the foreign sector—U.S. financial assets held by nonresidents—experienced the biggest growth from 2007 to 2019, rising about 82% in real terms to reach $35 trillion, the author noted, adding that much of this growth came from Treasuries, corporate equities and direct investment.

“Arguably, the increase in foreign investments in the U.S. was due to its safety, relative to the rest of the world,” and this “flight to safety” benefited the public and private sectors, Martin wrote.

Pandemic Reveals Fragilities

In the wake of the 2007-08 financial crisis and Great Recession, the Fed’s footprint grew and financial regulation and oversight increased. These changes reshaped U.S. financial activity, yet the composition of financial asset holdings by key sectors of the economy stayed largely unchanged between 2007 and 2019, Martin observed.

However, some important changes also occurred during that time:

- The financial sector became more liquid and safe.

- There was a significant increase in foreign investment.

When the COVID-19 pandemic began, the safety and liquidity of the financial markets were tested, Martin noted. Similar to what happened during the financial crisis, institutional investors built up reserves, which exerted stress on money market funds and commercial paper markets. Also, highly leveraged financial firms were forced to sell liquid assets, and corporate debt yields increased sharply.

“Early Fed intervention, in the form of lower rates and the opening of various credit facilities, may have prevented this stress from developing into a wholesale panic,” Martin concluded. “Still, the experience highlighted the fact that, despite the lessons learned from the previous crisis and the actions taken to address them, the nonbank financial sector continues to exhibit areas of fragility.”

Additional Resources

- Regional Economist: The U.S. Financial Landscape on the Eve of the Pandemic

- On the Economy: The Impact of the Fed’s Response to COVID-19 So Far

- On the Economy: Ready for the Pandemic? Household Debt before the COVID-19 Shock

Citation

ldquoViewing the U.S. Financial Structure from the Financial Crisis to the Pandemic,rdquo St. Louis Fed On the Economy, Sept. 24, 2020.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions