The Market’s Expectations about FOMC Meetings

There are eight scheduled Federal Open Market Committee (FOMC) meetings each year. However, not all FOMC meetings are created equal. A prescheduled press conference follows four of the eight meetings (those held in March, June, September and December in 2017). This allows the chairperson to present the FOMC's current economic projections and provide additional context for policy decisions.

Many believe that the FOMC prefers to make policy changes at meetings with a press conference because the opportunity for communication reduces uncertainty in the markets. A brief examination of the data suggests that markets hold this belief.

The Federal Funds Rate Target

The federal funds rate target is an important policy tool controlled by the FOMC, allowing it to influence short-term and long-term interest rates. As the FOMC continues the rate hike cycle it began in December 2015, future target rates are the subject of much speculation by market participants.

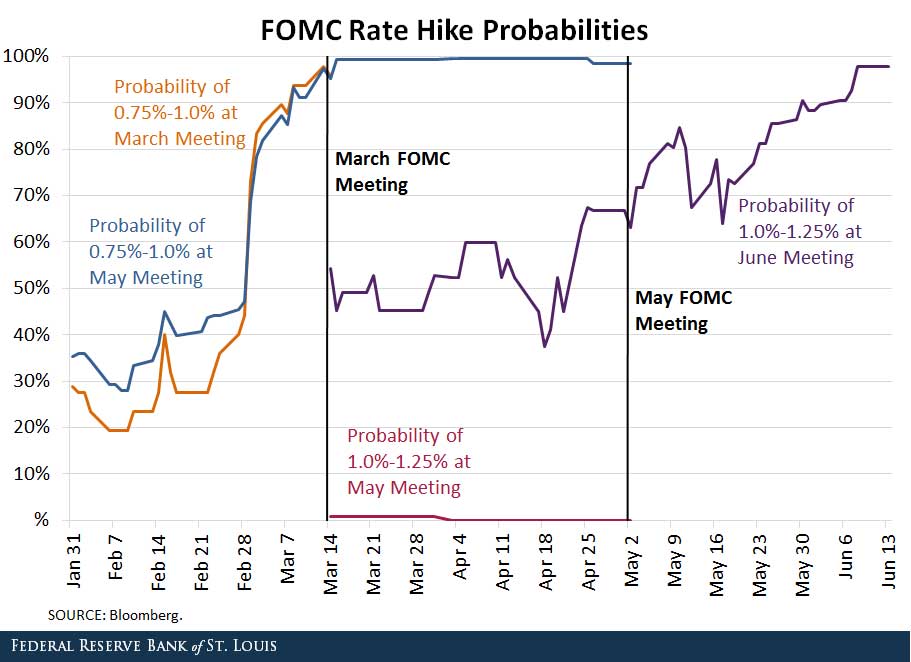

Using federal funds rate futures, projections of future target rates are computed each trading day. The figure below plots the market estimates of rate increases at future FOMC meetings following the Jan. 31-Feb. 1 meeting, which affirmed a target range of 0.5 to 0.75 percent.

The orange line indicates the probability that the federal funds rate target is between 0.75 to 1.0 percent at the March meeting for each trading day between Jan. 31 to March 14, the date of the March meeting.

For example, on Feb. 1, the market gave a 28.8 percent chance that the target would be at 0.75 to 1.0 percent at the March meeting. Given that the next meeting as of Feb. 1 was the March meeting, the 28.8 percent was indeed the rate hike probability for the March meeting.

Similarly, the blue line plots the same probability for May. On Feb. 1, the market gave a 35.9 percent probability that the target would be at 0.75 to 1.0 percent after the May meeting.

However, the May meeting would be the second meeting after Feb. 1, so the interpretation of this 35.9 percent probability is slightly different. It represents the probability of a rate hike at either the March meeting or the May meeting.

Market Expectations of Rate Increases

Does the market expect the FOMC to change the federal funds rate target only at meetings accompanied by a press conference? We can answer this question by comparing changes in the market's projection between two consecutive meetings.

Let’s first compare the market's expectation between the press conference meeting in March and the nonconference meeting in May.

The March and May FOMC Meetings

As discussed earlier, the orange line indicates the rate hike probability for the March meeting, and the blue line indicates the rate hike probability for the March or May meeting. Hence, the difference between these two probabilities can be thought of as the probability of a rate hike only at the May meeting.

If the market expects that the federal funds rate target can only be changed at the conference meeting in March and remain the same at the nonconference meeting in May, then we should see that the orange line and the blue line follow each other closely until the date of the March meeting with a difference that is close to zero.

This is exactly what we observe. Right before the March meeting, both probabilities approached 100 percent, indicating that the market expected a rate hike at the March meeting followed by no change at the nonconference meeting in May.

The May and June FOMC Meetings

Similarly, we can compare the rate hike probabilities between the nonconference meeting in May and the press conference meeting in June, which are indicated by the red line and the purple line:

- The red line represents the rate hike probability for the May meeting.

- The purple line indicates the rate hike probability for the May meeting or the June meeting.

Hence, the difference between the lines indicates the probability of a rate hike at the June meeting only.

The red line suggests that the probability of a rate hike at the May meeting is essentially zero after the March meeting occurred. Given that the market assigned a rate hike probability of zero for the May meeting, the rate hike probability for the June meeting is essentially equal to the probability indicated by the purple line. It started around 50 percent right after the March meeting and gradually approached 100 percent right before the June meeting. This is additional evidence that market participants expect rate hikes to occur only at the conference meetings.

Effects of FOMC Press Conferences

The market seems to believe that important policy changes can only be done at meetings accompanied by a press conference. If that is the intention of the FOMC, then the role of these nonconference meetings becomes ambiguous. In addition, if economic conditions change enough that a policy response is required at a nonconference meeting, should the FOMC pursue the policy change or wait until the next meeting with a press conference? If this is not the intention of the FOMC, should the FOMC consider equalizing the meetings to correct the bias expected among market participants?

Additional Resources

- A History of FOMC Dissents

- On the Economy: Consumer Surveys, Inflation Expectations and the FOMC

- On the Economy: Inflation and the Role of Fed Credibility

Citation

YiLi Chien and Paul Morris, ldquoThe Market’s Expectations about FOMC Meetings,rdquo St. Louis Fed On the Economy, July 13, 2017.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions