Serious Mortgage Delinquencies Fell during Fourth Quarter

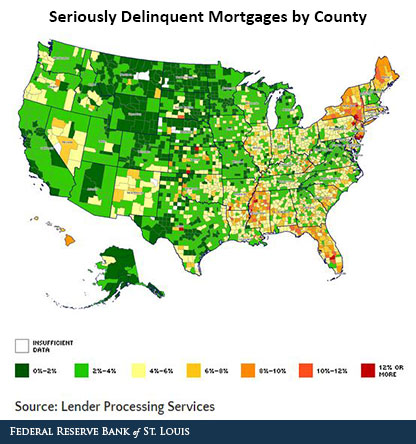

The latest issue of Housing Market Conditions, produced by the Federal Reserve Bank of St. Louis, reported that 3.99 percent of mortgages in the United States were seriously delinquent in December. (These are mortgages delinquent 90 days or more or in foreclosure.) The figure below shows the percent of seriously delinquent mortgages by county for September.

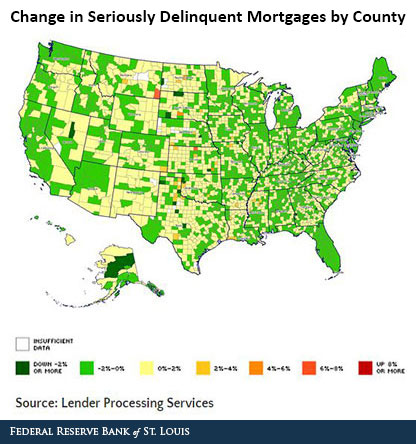

The share of seriously delinquent loans in the U.S. decreased 8 basis points (bps) between September and December. Loans that were delinquent 90 days or more increased 2 bps, while foreclosures decreased 12 bps. The figure below shows the change in seriously delinquent mortgages by county over this period.

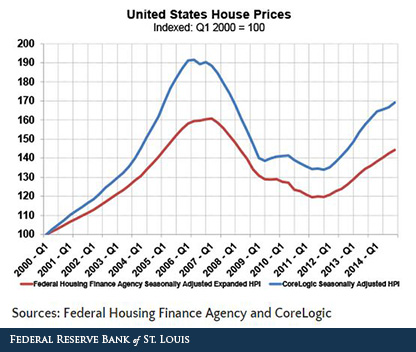

The next figure shows changes in U.S. house prices since 2000 according to two indexes:

- Federal Housing Finance Agency Seasonally Adjusted Expanded HPI (FHFA)

- CoreLogic Seasonally Adjusted HPI (CoreLogic)

For the fourth quarter of 2014, house prices in the U.S. were 1.3 percent higher according to FHFA and 1.5 percent higher according to CoreLogic when compared with the third quarter of 2014. Since the fourth quarter of 2013, house prices have risen 6.0 percent and 5.0 percent according to FHFA and CoreLogic, respectively.

Additional Resources

- On the Economy: Beige Book: Economic Activity Expands across Most Regions

- On the Economy: The Differences between House Price Indexes

Citation

ldquoSerious Mortgage Delinquencies Fell during Fourth Quarter,rdquo St. Louis Fed On the Economy, March 10, 2015.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions