Why Has the U.S. Net Foreign Asset Position Weakened?

Foreign investors hold more in U.S. assets than U.S. investors hold in foreign assets. And this gap has grown considerably over the past few years. Why has this been the case?

What Is the Net Foreign Asset Position?

The total value of foreign assets held by U.S. investors is referred to as U.S. external assets. The total value of U.S. assets held by foreigners is referred to as U.S. external liabilities. The difference between the values of U.S. external assets and liabilities is the U.S. net foreign asset (NFA) position. If the NFA position is positive, meaning that assets are higher than liabilities, the U.S. is a creditor country. When the NFA position is negative, the U.S. is a debtor country.

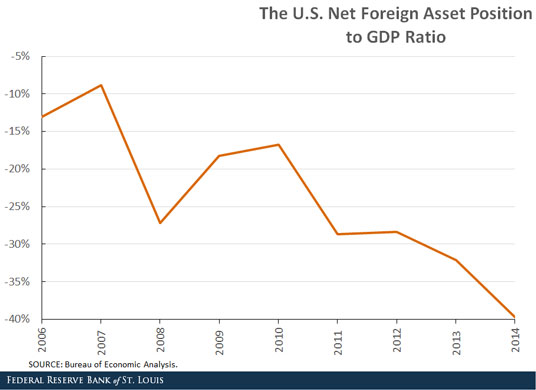

The figure above plots ratio of the U.S. NFA position to gross domestic product (GDP) over the period 2006-2014. During this period, the U.S. is always in debt.1 In addition, the debt is sizable (measuring nearly 23 percent of GDP on average) and volatile (ranging from nearly 8 percent to nearly 40 percent of GDP).

Notably, the U.S. NFA position has dropped rapidly since 2010. The U.S. net external debt increased from 17 percent of GDP to almost 40 percent of GDP. It is thus relevant to examine what factors generally drive the NFA position and what contributed to the rapid deterioration of the U.S.’s position.

Current Accounts

Intuitively, if people’s consumption is always higher than their income, then they must be in debt in the long run. The corresponding measure of a country’s net income and consumption is referred to as that country’s current account, which consists mainly of that country’s trade balance and net income account payments to other countries.

A trade deficit suggests that a country’s expenditures exceed its revenues in the foreign market. To finance this deficit, this country has to sell its external assets, increase its external liabilities or perform a combination of the two. Thus, a trade deficit tends to reduce a country’s NFA position.

On the other hand, the net factor income account measures net income from abroad. A positive net factor income account suggests a positive income receipt for the country and tends to increase the NFA position.

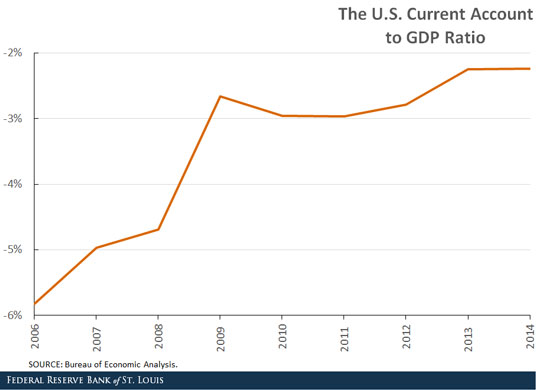

The ratio of the U.S. current account to GDP is plotted above for the period 2006-2014. The figure shows that the U.S. is running a current account deficit, meaning that the U.S. has consistently consumed more than its income. The negative current account definitely contributes to the deterioration of the NFA position, but the current account balance has actually improved over time, from just above -6 percent of GDP in 2006 to slightly below -2 percent in 2014. Thus, the change in the U.S. current account balance cannot explain the recent deterioration of its NFA position.

Valuation Effect

However, another factor—the valuation effect—also affects a country’s NFA position. Asset prices change over time and can often be volatile. Hence, the NFA position can vary greatly depending on asset price changes. For example, the U.S. NFA position tends to decrease if the return on its external assets falls behind the return owed on its external liabilities.

In addition, the exchange rate plays an important role in the valuation effect, as U.S. external liabilities (assets) are often denominated by U.S. dollars (foreign currency). The recent sharp appreciation of the dollar may thus help explain the large deterioration of the U.S. NFA position.

Notes and References

1 In fact, the U.S. NFA position has been negative since 1989.

Additional Resources

- On the Economy: How International Trade Affects the U.S. Labor Market

- On the Economy: How World War I Changed Marriage Patterns in Europe

- On the Economy: Why Does the U.S. Have Such a Large Trade Deficit with China?

Citation

YiLi Chien, ldquoWhy Has the U.S. Net Foreign Asset Position Weakened?,rdquo St. Louis Fed On the Economy, Aug. 17, 2015.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions