Chasing Returns Has a High Cost for Investors

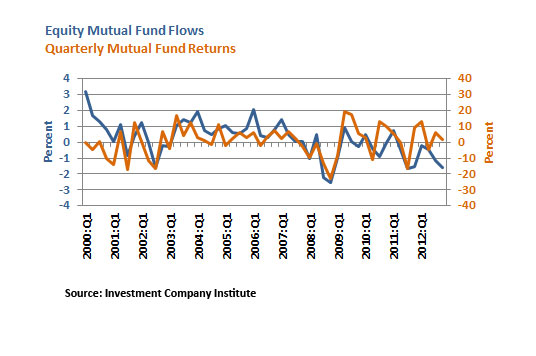

The investment behavior of households could be influenced by their own past experience, especially by the return performance of their portfolios. We can see this through U.S. equity mutual fund flows being positively correlated with their past returns. In other words, an average equity mutual fund investor tends to buy when past returns are high and sell otherwise. This is called return-chasing behavior.

I used quarterly equity mutual fund flow and return data from the Investment Company Institute for the period 2000-2012. The figure shows two data series: equity mutual fund flows and past quarter returns. The flow data at period t is measured as a percentage of the total value of U.S. equity mutual funds. The return plotted at period t is the return over the previous quarter. Clearly, equity mutual fund flows correlated positively with past return. The correlation coefficient between the returns and flows was 0.49.

This is important because such return-chasing behavior might cost mutual fund investors. Given that stock market returns are almost unpredictable in the short run and the return reverts to the mean (or moves back toward the average) in the long run, the tendency to buy high and sell low when exhibiting return-chasing behavior could eventually reduce part of their profits.

To assess how much return-chasing behavior costs investors, I compared the actual realized return of return-chasing behavior in our sample to a simple buy-and-hold investment strategy (a strategy in which investors simply buy equity and hold it for an extended period of time). We set the holding period of the buy-and-hold strategy to five years. (The result would be even stronger if the holding period was longer.)

Return-chasing behavior involves the size of investors’ equity positions changing over time, so the returns of both investment behaviors were evaluated in terms of so-called asset-weighted return. Note that the asset-weighted return of the buy-and-hold strategy simply equaled the time-weighted return during the holding period, which is the standard definition of average equity return reported on financial statements.

The result shows that return-chasing behavior had a significant impact on the performance of return. The buy-and-hold strategy earned an average annual return of 5.6 percent in the sample period, while return-chasing behavior only realized 3.6 percent. In other words, chasing returns caused the average U.S. mutual fund investor to miss around 2 percent return per year, which is very significant.

This post was updated to include a references section.

Notes and References

- Dolan, Karen. “Who Are Fickler Fund Investors: Advisors, Institutions, or Individuals?” Morningstar, June 10, 2010.

- Greenwood, Robin and Shleifer, Andrei. “Expectations of Returns and Expected Returns.” Working paper, January 2013.

Additional Resources

- Economic Synopses: Currency Returns During the Financial Crisis and Great Recession

- Economic Synopses: Quantitative Easing in Japan: Past and Present

- In the Balance: Housing Crash Continues to Overshadow Young Families’ Balance Sheets

Citation

YiLi Chien, ldquoChasing Returns Has a High Cost for Investors,rdquo St. Louis Fed On the Economy, April 14, 2014.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions