Unemployment Insurance: Payments, Overpayments and Unclaimed Benefits

Overpayments in the U.S. unemployment insurance system have received increasing attention of late. For example, CNN.com cited a recent study by the Department of Labor in reporting that 11 percent of all unemployment benefits were overpaid.1 Vice President Joe Biden, charged with leading the Campaign to Cut Waste, said: "Unemployment checks are going to people in prison. Unemployment checks are going to graveyards."

In this article, we examine the U.S. unemployment insurance system's expenditures over a longer horizon. We begin by illustrating the benefits paid from 1989 to 2011. Next, we take a look at the overpayments. Finally, we discuss a fact that is less well-known: Not everyone who is eligible for unemployment benefits actually collects them. Over the longer horizon, these unclaimed benefits are much larger than the overpayments that have received recent attention.

Unemployment Insurance

Unemployment insurance programs insure workers against the risk of lost income if they lose their job through no fault of their own. In the U.S., the program is run at the state level. Each state sets its benefit level and eligibility criteria, and finances these benefits through payroll taxes.2

Typically, the unemployment benefits last for a maximum of 26 weeks. These regular unemployment benefits paid by the states increased sharply during the recent recession. Measured in 2005 dollars, these benefits more than doubled, from $31 billion in 2007 to almost $72 billion in 2009. Since 2009, these regular benefits have decreased to levels below what they were after the previous recession: In 2011, the unemployment insurance program spent less than $42 billion on regular benefits, while the corresponding figure in 2002 was more than $46 billion.3

In periods of high unemployment, benefits may be continued for additional weeks beyond the regular cap of 26. Most states offer an additional 13 weeks of benefits when the unemployment rate in that state remains above a certain threshold. The federal government may also finance more benefits. For example, the federal government recently provided financing to some states to extend their benefits to a maximum of 99 weeks. During the early 1990s, the extended benefits added 60 percent to the regular benefits. During the past two years, the extended benefits have added more than 125 percent.

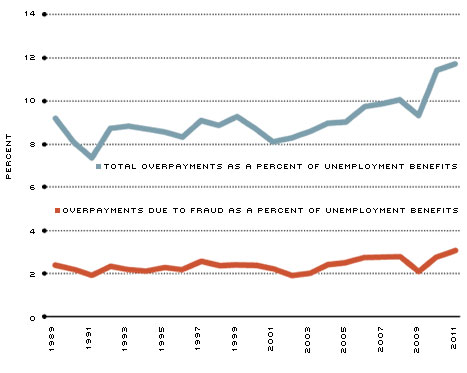

Overpayments and Fraud

{kind=link}

SOURCES: Benefit Accuracy Measurement (BAM) program, U.S. Department of Labor; authors' calculations.

NOTES: The fractions reported by the blue line are the total dollar amount of overpayments in a calendar year divided by the total dollar amount of benefits paid in the same year. Both amounts were obtained directly from the BAM sample and include only the payments by states for the standard 26 weeks. A similar calculation was used to compute the fraction reported by the red line.

Overpayments and Fraud

Some of the unemployment benefit payments were indeed overpayments, as recent newspaper reports suggest. Figure 1 illustrates the amounts overpaid. As a fraction of benefits, the average overpayment during 2007-2011 was 11 percent. During the middle of the recent recession, in 2008, the unemployment benefits amounted to $40 billion and the overpayment was $4 billion (both amounts in 2005 dollars).

The overpayments could stem from simple typographical errors on one extreme to out-right fraud on the other extreme. For example, an individual's benefit may be inadvertently set too high because the wrong formula was applied. This represents a simple error. Fraud, on the other hand, is a deliberate act. During 2007-2011, the overpayments due to all 28 categories of fraud accounted for 3 percent of the benefits on average; see Figure 1.4 Put differently, the overpayments due to fraud were roughly a fourth of the total overpayments.

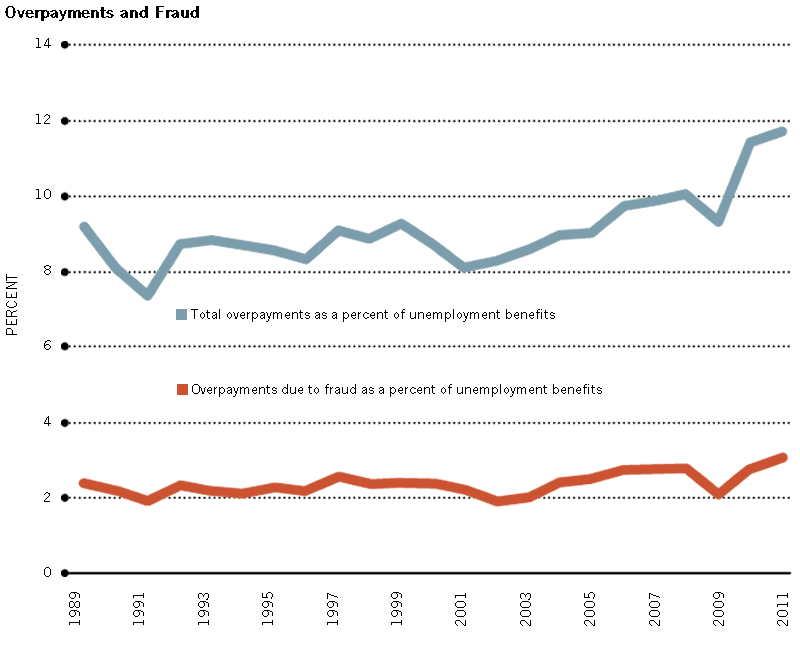

The dominant form of unemployment insurance fraud in recent years is what's classified as "Concealed Earnings" fraud: collection of unemployment benefits by individuals who are gainfully employed. As Figure 2 illustrates, overpayments from Concealed Earnings fraud have been steadily rising over the past 22 years and were almost 70 percent of the overpayments due to fraud in recent years.5

Overpayments due to Fraud by Cause

{kind=link}

SOURCES: Benefit Accuracy Measurement (BAM) program, U.S. Department of Labor; authors' calculations.

NOTES: The calculations use dollar amounts, not number of cases. To calculate the numbers in the figure, we first sum up the dollar amounts of overpayments due to all 28 types of fraud. Then, for each of the three forms of fraud discussed in the article, we calculate the total dollar amount of overpayments from the category. The numbers reported in the figure are the latter amount divided by the former.

Meanwhile, overpayments due to "Insufficient Job Search" (cases where the unemployed individual did not meet the mandatory work search requirement, such as minimum number of job applications to be filed each week) have been declining and are down to less than 5 percent of fraud.

Recent headlines on prisoners collecting unemployment benefits fall under "Unable and Unavailable to Work" fraud.6 This category includes cases where an unemployed person is not healthy enough to work or is in school, for example. Overpayments due to the entire Unable and Unavailable to Work category amounted to barely 5 percent of fraud in 2011. For the states in the Eighth District of the Federal Reserve (based in St. Louis), this category accounted for 2 percent of fraud in 2011.

Some Don't Seek Benefits

Although overpayments have grabbed recent headlines, only 35 percent of the unemployed have been collecting benefits over the past 22 years on average. Not all of these people are eligible to collect benefits, however. For instance, the typical duration of unemployment benefits is 26 weeks, and a person who continues to be unemployed past 26 weeks is not eligible. But not all of those who are eligible to collect unemployment benefits actually collect the benefits.

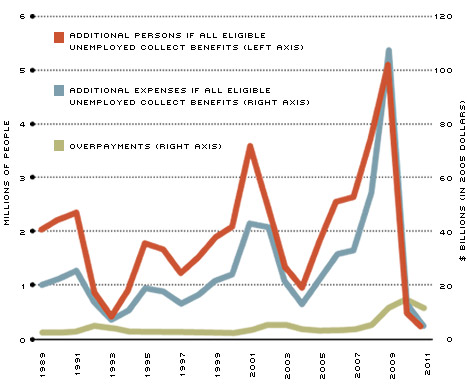

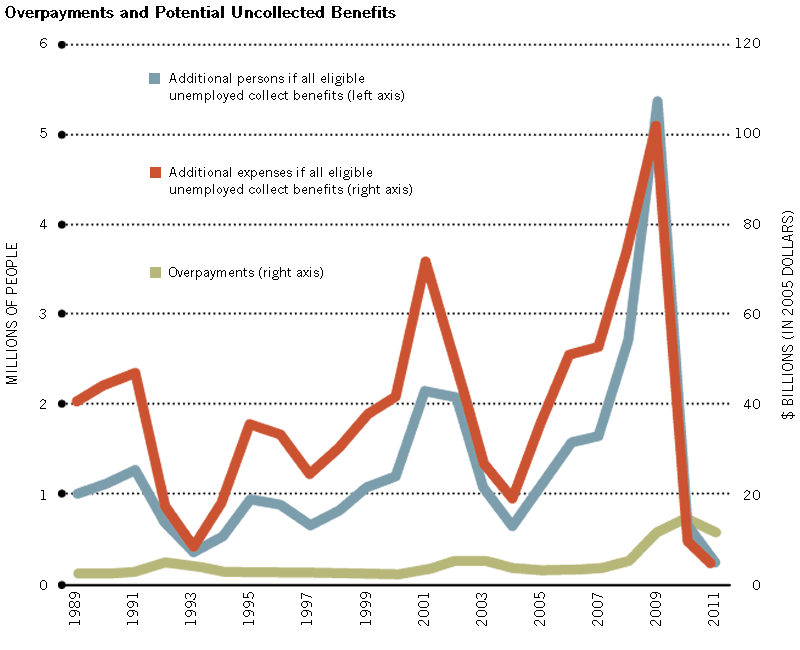

During the recent recession (2007-2009), roughly 50 percent of those eligible were collecting benefits. The fraction increased to 95 percent in 2011. In Figure 3, we illustrate the number of people who could have collected unemployment benefits but chose not to do so.

Figure 3 also illustrates a back-of-the-envelope calculation. If all of those who are eligible to collect unemployment benefits were to indeed collect the benefits, what would be the additional expenditures for the unemployment insurance program? The additional expenditures in 2009, toward the end of the recent recession, would have been a whopping $108 billion (in 2005 dollars). As Figure 3 illustrates, the overpayments in 2009 were $11 billion. On average, the unclaimed benefits are much larger than the more frequently discussed overpayments.

Overpayments and Potential Uncollected Benefits

{kind=link}

SOURCES: Overpayments: Benefit Accuracy Measurement (BAM) program,

U.S. Department of Labor; authors' calculations.

NOTES: We calculate the numbers for the gold line by multiplying the overpayment rate in Figure 1 by the amount of total unemployment benefits paid (that is, including extended benefits) reported by the Department of Labor. To obtain how many additional people could collect benefits, we use the calculations in Auray, Fuller and Lkhagvasuren. They compute the fraction of eligible unemployed who are collecting benefits by using Current Population Survey data and details on eligibility requirements for all U.S. states. We increase their fraction to 100 percent (as if all eligible unemployed collect benefits) and calculate the additional number of unemployed who could legitimately collect benefits. Additional expenses are calculated as follows: We divide the total unemployment benefit expenditures each year by the number of unemployed people collecting benefits in that year to obtain a benefit amount per person. Both of these numbers are tabulated by the U.S. Department of Labor; We then multiply the additional number of people by the benefit/person to obtain "Additional expenses if all eligible unemployed collect benefits."

Looking at the unemployment insurance program over the longer horizon, overpayments are less than one-tenth of the benefits paid, overpayments due to fraud are less than 3 percent of the benefits paid and unclaimed benefits are nearly seven times the overpayments. Although reducing the overpayments would clearly help reduce the expenditures for the unemployment insurance program, a higher fraction of eligible people choosing to collect unemployment benefits would significantly increase the expenditures for the program.

Endnotes

- See http://money.cnn.com/2012/07/09/news/economy/overpaid-unemployment-benefits/index.htm [back to text]

- There are three primary criteria for eligibility. First, the individual must have accumulated enough earnings or worked a minimum number of weeks during the previous year. Second, only those who lost their job through no fault of their own are eligible; thus, people who quit their job or are fired because of poor performance are not eligible. Finally, the duration of benefits is limited. [back to text]

- We obtain the nominal actual outlays from the Department of Labor, www.doleta.gov, and convert them to 2005 dollars using the GDP deflator in the FRED database, http://research.stlouisfed.org/fred2/ [back to text]

- These data are obtained from the Benefit Accuracy Measurement (BAM) program run by the U.S. Department of Labor. BAM lists 28 possible categories of fraud. The stated goal of BAM is to audit the paid benefits. The BAM program chooses a random sample of weekly unemployment insurance claims, and BAM investigators audit these claims to determine their accuracy. The investigators also interview some claimants if necessary. BAM investigators calculate statistics of the unemployment insurance program (see BAM State Operations Handbook ET No. 495, 4th Edition). Fraud investigators, on the other hand, look to recapture overpayments. [back to text]

- Fuller, Ravikumar and Zhang examine how to provide benefits and monitor individuals to deter Concealed Earnings fraud. [back to text]

References

Auray, Stephane; Fuller, David L.; and Lkhagvasuren, Damba. "Unemployment Insurance Take-up Rates in an Equilibrium Search Model." Working Paper, Concordia University, 2012.

Fuller, David L.; Ravikumar, B.; and Zhang, Yuzhe. "Unemployment Insurance Fraud and Optimal Monitoring." Federal Reserve Bank of St. Louis, Working Paper 2012-024A, July 2012.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us