Why Health Care Matters and the Current Debt Does Not

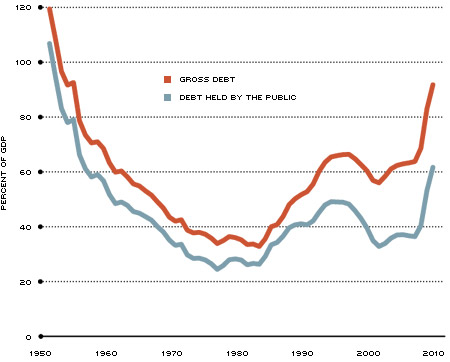

The global financial crisis and resulting Great Recession accelerated both national and international debate over the sustainability of U.S. government spending. This is the direct consequence of the crisis pushing the U.S. ratio of gross debt to GDP over 90 percent, due both to large increases in government spending and large decreases in tax revenue. (See Figure 1.) The fresh sense of urgency that this has ignited to solve the debt situation, however, obscures the fact that U.S. government spending was no more sustainable prior to the Great Recession than it is now. Put another way, the recent large deficits change almost nothing about the long-term fiscal prospects of the United States. The overwhelming obstacle to a sustainable fiscal path for the United States, regardless of the size of the current debt, remains health-care spending.

The U.S. Federal Debt

{kind=link}

SOURCE: Office of Management and Budget.

Data for 2008 through 2010 are estimates. Debt held by the public is gross debt less intra-governmental debt (i.e., government debt held by the government; the primary such holder is the Social Security fund) and financial assets owned by the government.

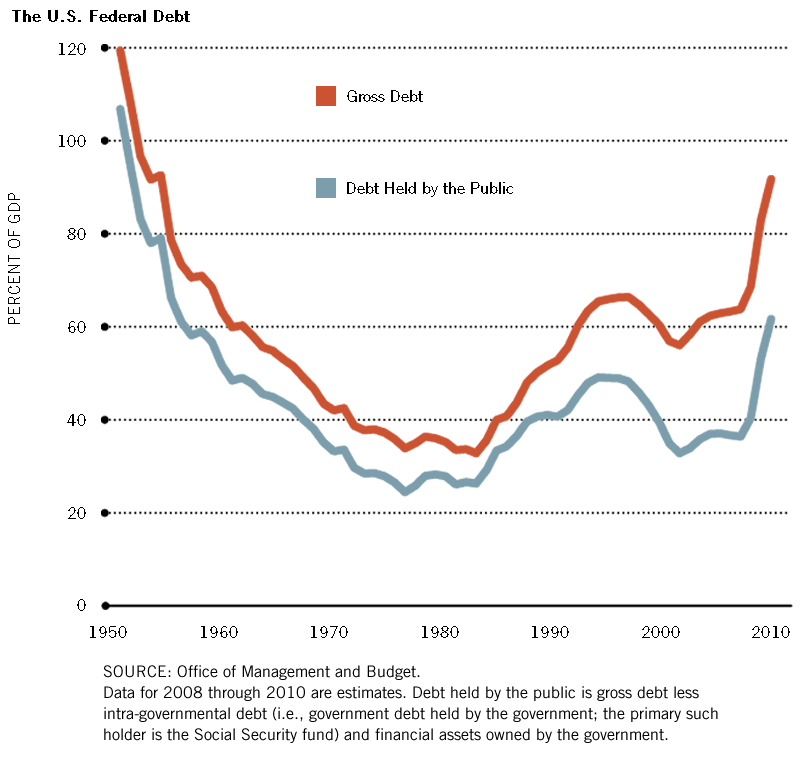

The Congressional Budget Office's Long-Term Outlook for Federal Outlays

{kind=link}

SOURCE: CBO.

NOTE: The solid lines denote the CBO baseline forecast where revenues increase as a share of GDP, while the dotted lines denote the CBO alternative forecast under constant tax revenues as a share of GDP. See endnote No. 2 for additional differences between scenarios.

The Long-Run Outlook

The basic picture of the U.S. debt situation is presented by the Congressional Budget Office (CBO) in its Long-Term Budget Outlook.1 Figure 2 shows the CBO's forecast of federal spending on net interest payments, Medicare/Medicaid and Social Security under two different scenarios. The primary differences between the extended-baseline scenario (solid lines) and alternative scenario (dotted lines) are the assumptions made regarding growth in government revenue.2 The extended-baseline scenario adheres, in the words of the CBO, "closely to current law": The 2001 tax cuts expire, the reach of the alternative minimum tax grows, the tax provisions of the recent health-care legislation remain in place and the tax code remains largely in place. Under this scenario, the increase in health-care spending and Social Security is roughly offset by the steady growth in tax revenue. In contrast, the alternative scenario takes the opposite assumptions of the baseline and assumes that tax revenue will remain near its historical average of 18 percent of GDP. From Figure 2, three key inferences can be made:

- If growth in government spending on health care and Social Security is matched by growth in government revenue, the cost of servicing the debt, and moreover the debt itself, will largely stabilize as a percent of GDP from 2020 to 2030. In other words, the current level of the debt is not by itself an obstacle to fiscal sustainability.

- If, on the other hand, the government increases spending on health care and Social Security without raising additional revenue, the debt, and the cost of servicing the debt, will skyrocket toward unmanageable levels.

- As a share of GDP, outlays on Social Security are expected to largely stabilize by 2030. Hence, the overwhelming driver of increases in government spending is health care.

Health care is often thought of as a "superior" good: The wealthier that individuals are, the greater their share of income that they would prefer to spend on health care.3 Therefore, it is sensible that the United States would wish to spend a larger and larger fraction of income on health care. The reality, though, is that rising health-care spending in the absence of revenue increases is unambiguously unsustainable, which was both true and well-documented prior to the current debt crisis.4 At some point, tough decisions have to be made regarding whether health care is a universal right, and, if it is, who is going to pay for it.

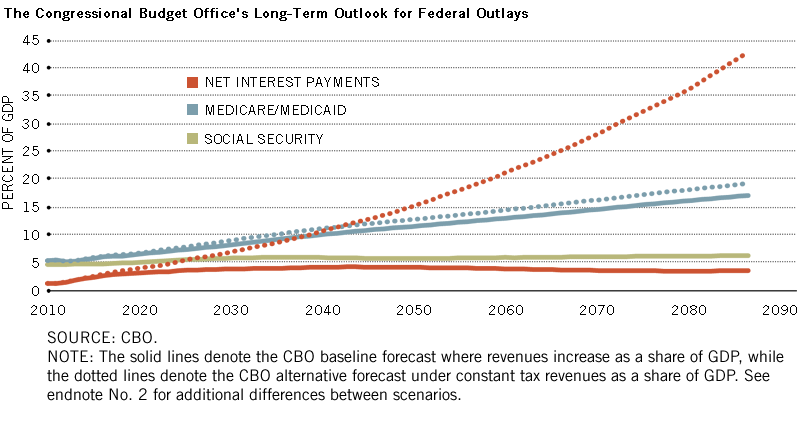

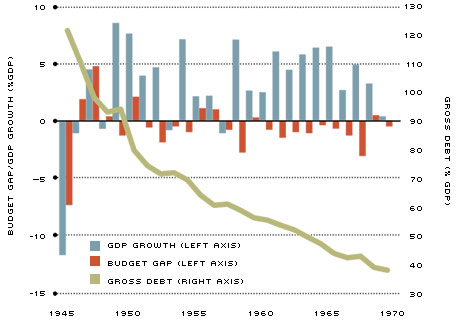

The Evolution of the U.S. Debt: 1946-1970

{kind=link}

SOURCES: Bureau of Economic Analysis and Office of Management and Budget.

The Current Situation

As seen in Figure 2, net interest payments, and by association the debt level, should largely stabilize and even begin to fall as a fraction of GDP, provided future spending increases on health care are met by future revenue increases. Obviously, one critical part of this equation is GDP growth.

Historically, GDP growth has been the key ingredient for reducing the effective size of the U.S. debt. Figure 3 shows that the U.S. gross debt-to-GDP ratio declined from a post-war high of over 120 percent in 1946 to just under 38 percent by 1970. Figure 3 also shows that this decline was not due to the government running surpluses, but almost entirely due to GDP growth: The average budget gap was a deficit equal to a half percent of GDP, as the government ran deficits in over two-thirds of the years covered. But because GDP grew on average 3 percent per year over this period, the ratio of gross debt to GDP fell precipitously.

One fair charge is that, in the current situation, we cannot rely on GDP growth to magically wipe away the debt. In particular, the assertion that a causal link exists between high debt and low growth is particularly worrisome, as it would imply a reinforcing cycle between low growth and rising debt.5 But this is where it is important to remember that the government differs critically from businesses and individuals.

As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills.6 In this sense, the government is not dependent on credit markets to remain operational. Moreover, there will always be a market for U.S. government debt at home because the U.S. government has the only means of creating risk-free dollar-denominated assets (by virtue of never facing insolvency and paying interest rates over the inflation rate, e.g., TIPS—Treasury Inflation-Protected Securities). Together with the unusually high, but manageable, level of the current debt, these facts imply that the current U.S. government can wait out any short-term economic developments until long-run growth is restored.7 Further, without an immediate need to drastically reduce the debt, the mechanism between high debt and slow growth loses most of its credibility.

Of course, as we have already seen with health care, the government does not have the ability to systematically increase spending without any regard for funding it. And government borrowing can be extremely costly. The cost of government borrowing is the "crowding out effect": Investment funds mobilized by the government cannot be used in the private sector. It is in this framework, though, that classical economic theory argues the government should neither borrow nor lend, not because it has a moral obligation to run balanced budgets, but because it must consider the cost of diverting investment funds away from potentially more-productive uses.

In an economic environment like today's, where real interest rates are practically zero, if not negative, and the unemployment rate remains high, the opportunity cost to society of the government's mobilizing capital and labor is unprecedentedly low: The private sector is not fully utilizing these resources; so, no opportunities are lost if the government uses them. Assuming investment projects with a positive net expected return exist, as they surely do, there has hardly been a less costly time to start such projects.8 What no country can afford, however, are permanent increases in government spending without increasing tax revenue.

Endnotes

- See Congressional Budget Office. [back to text]

- In addition to altering its assumptions about tax revenue in the alternative scenario, the CBO relaxes some of the assumptions that it makes regarding the full implementation of the recent health-care bill. This slightly modifies its projections for health-care spending, though this is of secondary importance to the tax revenue assumptions. The alternative scenario contains no changes in assumptions regarding Social Security; so, the solid and dotted lines fully overlap. [back to text]

- See Scheiber. [back to text]

- See Wasylenko. [back to text]

- See Reinhart and Rogoff. [back to text]

- Technically, the debt ceiling could render the government unable to pay its bills, but the law has little credibility because enforcing it would almost certainly cause more harm than good. [back to text]

- The long-run GDP growth assumed by the CBO is a fairly conservative 2.1 percent. [back to text]

- Note that we are drawing a strict distinction between investment projects, e.g., infrastructure, which enhances the capacity of the economy and will likely be needed down the line, and current spending, which only provides services today. [back to text]

References

Congressional Budget Office. "CBO's 2011 Long-Term Budget Outlook." June 2011. See www.cbo.gov/doc.cfm?index=12212

Reinhart, Carmen M.; and Rogoff, Kenneth S. "Growth in a Time of Debt." National Bureau of Economic Research Working Paper No. 15639, January 2010. See www.nber.org/papers/w15639

Scheiber, George J. "Health Care Expenditures in Major Industrialized Countries: 1960-1987." Health Care Financing Review, Summer 1990, Vol. 11, No. 4, pp. 159-67.

Wasylenko, Michael. "Health Care and the Looming Fiscal Crisis in the United States." Revista Chilena de Administracion Publica (Chilean Journal of Public Administration), June 2007, Issue 9, pp. 65-78. See http://surface.syr.edu/cgi/viewcontent.cgi?article=1003&context=ecn

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us