Government Budget Surpluses Head South: Will They Come Back?

Government finances typically deteriorate during recessions. When the economy weakens, growth of incomes and, hence, of tax receipts slows, while expenditures on unemployment insurance and other income-support programs increases. This effect can be compounded during times of war. In 2001, the U.S. economy experienced all of these. The result was about as expected: Government surpluses at the federal, state and local levels diminished markedly. Because there is a distinct possibility that some of these developments will persist in 2002, will government budget balances bounce back?

An Update on Federal Finances

After running deficits that averaged almost $200 billion a year from 1989 to 1997, the federal government recorded a budget surplus of $69.2 billion in fiscal year 1998. This was the first surplus in more than 25 years.1 Over the next two years, as the economy strengthened, the federal surplus nearly quadrupled, rising to just under $240 billion in fiscal year 2000, or 2.4 percent of GDP. In May 2001, this trend was expected to continue: The Congressional Budget Office (CBO) projected federal surpluses totaling just over $5.6 trillion between fiscal years 2002 and 2011.

Some economists, however, thought it unlikely that future surpluses of this magnitude would ever materialize.2 The reason, as the CBO itself cautioned policy-makers, was that these medium- term budget projections were highly conditioned on the assumptions that the economy would continue to grow robustly and that there would be no new tax cuts or increases in government spending. Given the magnitude of the dollars involved (trillions), even small projection errors in these "conditioning" assumptions have the potential to become quite large when compounded over a decade. To see this, one need only remember that as late as 1997, the CBO and most private forecasters were projecting relatively large and rising budget deficits over the next decade.

The pendulum has now swung modestly in the opposite direction. In its latest report, issued in January 2002, the CBO now projects that federal surpluses for fiscal years 2003 to 2012 will sum to about $2.2 trillion, with small deficits projected for fiscal years 2002 (–$21 billion) and 2003 (–$14 billion). Of course, the CBO in its May 2001 report could not have foreseen the events of Sept. 11, the subsequent war on terrorism and the 2001 recession. And while budget forecasters might have surmised from the 2000 presidential campaign that, if elected, Gov. George Bush planned to pursue cuts in marginal tax rates, the rules of the game prevented the forecasters from adjusting their budget projections accordingly.3

An Update on State and Local Finances

State and local government finances also benefited from a strongly growing U.S. economy during the second half of the 1990s and into early 2000. In fact, state finances saw a remarkable turnaround from the financial difficulties they endured during the late 1980s and early 1990s. From 1980 to 1994, total state and local government receipts grew by an average of 7.5 percent a year, while expenditures were rising by an average of 7.7 percent a year. This situation reversed itself from 1995 to 2000: Growth of state and local receipts averaged 5.9 percent a year, while their expenditures increased by 5.7 percent a year.4 Accordingly, budget surpluses built up: By 1998, state and local budget surpluses as a percent of GDP rose to a 12-year high of 0.5 percent. In response, net tax reductions occurred at the state level each year for fiscal years 1995 to 2001.5

But as the U.S. economy turned down in late 2000, state and local budgets once again came under increasing pressure. After averaging almost $22 billion (annual rate) over the first half of 2001, aggregate budget surpluses of state and local governments fell to $1.9 billion by the third quarter of 2001. As the growth of tax receipts slowed dramatically, many states, most of which operate under some sort of balanced-budget requirement, were forced to trim planned outlays, raise taxes and/or redirect money from "rainy day" funds.6 By late November 2001, the National Conference of State Legislatures (NCSL) reported that 44 states (including the District of Columbia) were reporting that revenues were coming in under projection, while 22 reported that expenditures were over budget. As a result, 36 states were in the process of, or were considering, cutting expenditures planned for fiscal year 2002.

State budget shortfalls appeared to increase further early this year. In October 2001, the National Association of State Budget Officers reported that actual expenditures were running ahead of planned receipts by a total of $15 billion. By late January 2002, total projected shortfalls had jumped to about $40 billion. Although nearly one-third ($12.4 billion) of the shortfall in January stemmed from the budget problems in California, some Eighth District state governments were also reporting significant financing problems. The shortfall projected in Illinois was $400 to $500 million; in Indiana, $800 to $950 million; in Kentucky, $533 million; in Missouri, $536 million; and in Tennessee, $300 to $400 million. Moreover, Tennessee lawmakers expect their problems to worsen appreciably: A shortfall of between $800 million and $1 billion is projected in fiscal year 2003. By contrast, projected state budget shortfalls are much smaller in Arkansas ($19.7 million) and Mississippi ($80 million).

Will the Surpluses Return?

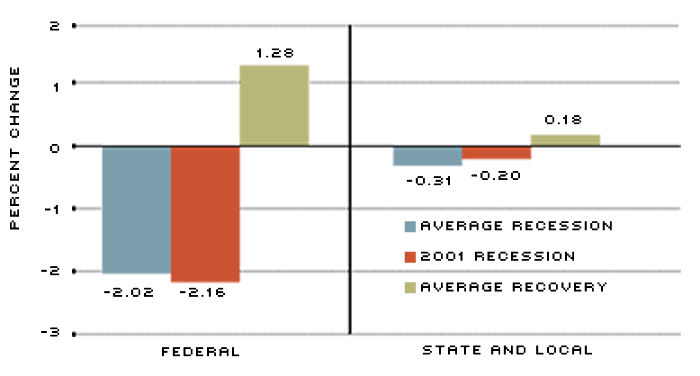

Because government budget balances tend to move in tandem with the economy, it seems reasonable to conclude that the fiscal outlook will improve once the turmoil of recession and war passes. The figure below, which shows government budget balances as a percent of GDP, offers some evidence in support of this assertion. On average, federal budget balances fall by about 2 percent during recessions. The deterioration in state and local budget balances is much less, 0.3 percent, which is expected given their balanced-budget requirements. Although results for the fourth quarter of 2001 were not yet available, it appears that the decline in the federal budget balance during the 2001 recession was somewhat larger than average. By contrast, the decline in state and local government budget balances has been pretty close to average.

The green bars in the figure show the average increase in budget balances as a percent of GDP over the four quarters immediately following the recession's trough. During the early phase of an economic expansion, the federal government's budget balance increases by 1.3 percent of GDP. Thus, if forecasters are correct in their assessment of how strong the economy will be in 2002, and if history is any gauge, then the federal budget balance may improve by as much as $137 billion this year, meaning a possible return to the black by the end of the year.7 A similar accounting exercise for state and local budget balances suggests that their budget balances could increase by as much as $19 billion between the fourth quarter of 2001 and the fourth quarter of 2002.8

A Caveat

This projection, though, is conditional on an average recovery. But this recession has not been average in several respects. Moreover, it ignores some emerging trends in fiscal policy that may preclude, or limit, the improvement in fiscal balances that occurs during a typical recovery. First, at the federal level, President Bush requested sizable increases in spending on defense and homeland security in his fiscal year 2003 budget, submitted to Congress in February 2002.

At the state and local level, policy-makers are struggling to cope with large increases in Medicaid spending.9 From 1987 to 2000, state spending on Medicaid had risen by nearly 12 percent a year, outstripping the percentage growth of all other major expenditures. As a result, Medicaid is now the second-largest expenditure of state governments, just behind spending on elementary and secondary education. An additional uncertainty is the extent to which federal resources will be diverted to state and local governments to implement several of the new initiatives designed to enhance homeland security.

Average Changes in Federal and State and Local Budget Balances During and After Recessions

NOTE: Budget balances shown as a percent of nominal GDP. Data shown are on a National Income and Product Accounts (NIPA) basis and exclued the short 1990 recession and recovery.

Endnotes

- The federal budget is reported on a unified basis, which is the sum of off-budget and on-budget items. The off-budget includes Social Security and the U.S. Post Office, whereas the on-budget is everything else. [back to text]

- See Kliesen and Thornton (2001). [back to text]

- According to CBO estimates published in January 2002, the Economic Growth and Tax Relief Reconciliation Act of 2001 is expected to reduce the cumulative unified budget surplus (relative to the baseline before the tax cut) by $1.3 trillion from 2002 to 2011--or roughly one-third of the projected $4 trillion in reduction in 10-year budget surplus cited earlier. [back to text]

- Some of this improvement likely also stemmed from the 1996 Welfare Reform legislation, as welfare rolls nationally fell by 53 percent between August 1996 and June 2000. [back to text]

- See National Association of State Budget Officers (December 2001). [back to text]

- In 45 states, the governor must submit a balanced budget, while in 41 states a legislature must pass a balanced budget. Only 35 states require that a governor must sign a balanced budget. [back to text]

- This article assumes that the recession ended during the fourth quarter of 2001. The federal deficit (using national income and accounts data) totaled –$13.6 billion during the third quarter of 2001 and was likely even more negative during the fourth quarter. [back to text]

- These numbers are derived by taking 1.28 percent and 0.18 percent, respectively, of the projected value of current-dollar GDP in the fourth quarter of 2002. The projection assumes that nominal GDP increases 4.5 percent, which was the Blue Chip Consensus forecast issued on Feb. 10, 2002. [back to text]

- Medicaid is a joint federal-state health program for the poor. [back to text]

References

Congress of the United States. The Budget and Economic Outlook: Fiscal Years 2003-2012. A Report to the Senate and House Committees on the Budget, Washington, D.C.: Congressional Budget Office, January 2002.

Kliesen, Kevin L. and Thornton, Daniel L. "The Expected Federal Budget Surplus: How Much Confidence Should the Public and Policymakers Place in the Projections?" Federal Reserve Bank of St. Louis Review, March/April 2001, Vol. 83, No. 2, pp. 11-24.

National Association of State Budget Officers and the National Governors Association. The Fiscal Survey of the States, December 2001.

________. State Expenditure Report, Summer 2001. National Conference of State Legislatures. State Fiscal Outlook for FY 2002, Fiscal Affairs Program, December 2001.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us