Trapped: Few Developing Countries Can Climb the Economic Ladder or Stay There

The low- or middle-income trap phenomenon has been widely studied in recent years. Although economic growth during the postwar period has lifted many low-income economies from poverty to a middle-income level and other economies to even higher levels of income, very few countries have been able to catch up with the high per capita income levels of the developed world and stay there. As a result, relative to the U.S. (as a representative of the developed world), most developing countries have remained, or been "trapped," at a constant low- or middle-income level.

Such a phenomenon raises concern about the validity of the neoclassical growth theory, which predicts global economic convergence. Specifically, economics Nobel Prize winner Robert Solow suggested in 1956 that income levels in poor economies would grow relatively faster than income in developed nations and eventually converge with the latter through capital accumulation. (See sidebar.) He argued that this would happen as technologies in developed nations spread to the poor countries through learning, international trade, foreign direct investment, student exchange programs and other channels.1

But the cases in which low- or middle-income countries have successfully caught up to high-income countries have been few.

Many poor countries today have a per capita income that is 30 to 50 times smaller than that of the U.S. and sometimes even lower (less than $1,000 per year in 2014). For such countries to catch up to U.S. living standards, it may take at least 170 to 200 years, assuming that the former could maintain a growth rate that is constantly 2 percentage points over the U.S. rate (which is about 3 percent per year). This would be difficult, if not impossible. It is even harder to imagine that such countries could reach U.S. living standards within one to two generations (40 to 50 years), similar to how North American and Western European economies caught up to Britain during the 1800s after the Industrial Revolution. To achieve that speed of convergence today, the developing countries would need to grow about 8 percentage points faster than the U.S. (or about 11 percent per year) nonstop for 40 to 50 years. In recent history, only China came close to this; it was able to maintain a 10 percent annual growth rate (7 percentage points above the U.S. rate) for 35 years, but per capita income in China was still only one-seventh of that in the U.S. in 2014.

Hence, the lack of income convergence and the relative income traps appear to be real problems.

In this article, we first define the concept of an income trap and describe evidence that points to the existence of both low- and middle-income traps. Second, we analyze the historical probability of transitioning to higher relative income groups and test the persistence of the traps over time. Finally, we offer some hypotheses on the existence of income traps, as well as their policy implications.

Defining the Income Trap

The economic development literature provides various ways to classify countries by income groups, as well as several definitions of the "poverty trap" and the "middle-income trap."2 Most researchers have used absolute measures of income levels (such as median income per capita) or growth rates to define what constitutes a low- or middle-income trap, but in doing so, they have ignored the more pervasive phenomenon of the lack of convergence.

Although many so-called middle-income countries have experienced persistent economic growth, their growth rates never surpassed the U.S. growth rate; consequently, these countries have been unable to close their income gaps with the U.S. In other words, these countries remain "trapped" at relatively lower income levels compared to the living standards of the developed countries, contrary to the neoclassical growth theory's predictions that they will converge due to technology spillover and international capital flows.

The lack of relative income convergence implies that income per capita in the U.S., as well as general living standards, will continue to be 10 to 50 times higher than in low-income economies and two to five times higher than in middle-income economies. Therefore, redefining the low- and middle-income traps as situations in which income levels relative to those of the U.S. remain constantly low and without a clear sign of convergence allows us to study the issue of economic convergence (or lack of it) more directly.

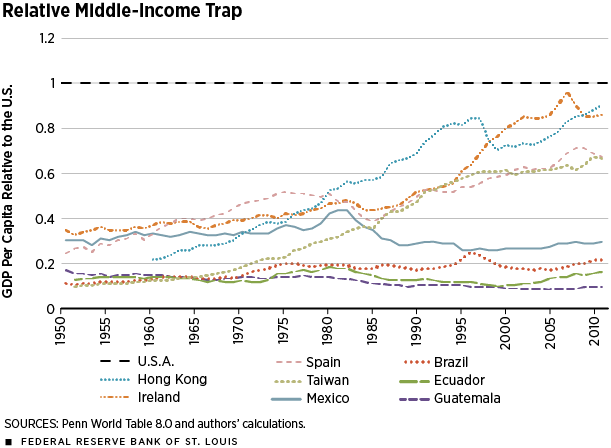

The most common examples of rapid and persistent relative income growth (leading to convergence) are the Asian Tigers (Hong Kong, Singapore, South Korea and Taiwan); other countries include Spain and Ireland.3 Figure 1 shows a sample of these economies where relative per capita income grew significantly faster than in the U.S. beginning in the late 1960s all through the early 2000s, catching up or converging to the higher level of per capita income in the U.S. In sharp contrast, per capita income relative to the U.S. remained constant and stagnant between 10 percent and 40 percent of U.S. income among the Latin American countries that are listed. Despite experiencing moderate absolute growth during the same period, they remained stuck in the "relative middle-income trap" and showed no sign of convergence to higher income levels.

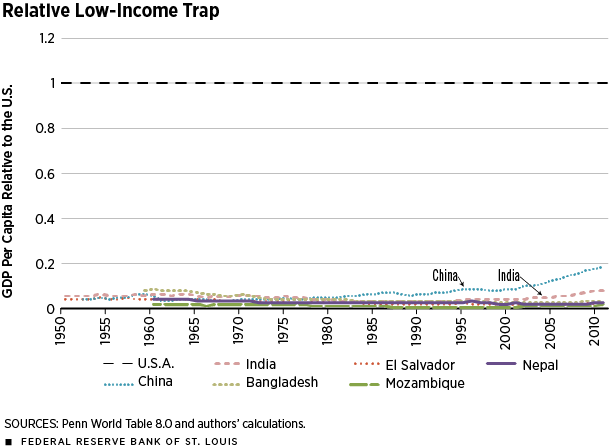

The lack of convergence is even more striking among low-income countries (Figure 2). For example, Bangladesh, El Salvador, Mozambique and Nepal are stuck in a poverty trap, where their relative per capita income is constant at or below 5 percent of the U.S. level. Even though their economies might have grown moderately in absolute terms, they have not grown at a rate faster than the U.S. growth rate; thus, their relative income levels have not increased. As a result, the income gap between these nations and the U.S. has permanently been at least 20 times their own income per capita.

In comparison, China has been able to grow relatively faster than the U.S. since about the early 1980s, breaking away from the relative low-income trap and reaching middle per capita income levels. India has also shown signs of escaping the low-income trap since the early 1990s. However, both countries still have a long way to go to catch up and converge to the levels seen in developed economies, and both have yet to encounter the relative middle-income trap.

Are the Traps Real?

Studying the historical evidence of how a country's relative income changed after a given number of years confirms the existence of both relative income traps. For each year between 1950 and 2011, we determined whether a country's relative income fell into a low range (≤15 percent of U.S. income), middle range (>15 to 50 percent of U.S. income) or high range (>50 percent of U.S. income). We then compared that relative income classification to the same country's relative income after 10 years, 20 years and at the end of the sample (30 to 61 years, depending on data available).4

As shown in Table 1, the relative low-income trap is highly persistent: The probability of remaining trapped in the low-income range is 94 percent after 10 years (Panel A), 90 percent after 20 years (Panel B) and 80 percent in the entire observational period, 30 to 61 years (Panel C). Meanwhile, the effects of the relative middle-income trap are strong in the 10-year period (with a probability of remaining in the middle-income status of 80 percent and a 9 percent probability of regressing to low-income status), but dissipate in the longer term. Still, Panel C shows that more than half of the economies that had a middle-income status at the beginning of the sample remained at or below that relative income status (with a cumulative probability of 47 percent + 17 percent = 64 percent), indicating that these economies experienced a small probability of relative convergence to higher levels of relative income even after having moderate absolute growth during the entire 30- to 61-year period.

In other words, the probability of escaping the middle-income trap is 11 percent after a 10-year period, 21 percent after a 20-year period and 36 percent after 30 to 61 years. Also interesting to note is that countries almost never degrade to low- or middle-income status once they have reached the high-income status: The probability of remaining at a high-income status is at least 97 percent.

Going back further in history, the general picture is not very different.5 Calculating the countries' transitions among relative income groups between 1870 and 2010, the low relative income trap is highly persistent even in the long run, and the probability of remaining in a middle-income trap is still substantial enough that it warrants a search for further explanations. (See Table 2.) These results also support our claim that both the relative low-income trap and the relative middle-income trap exist because the probability of transitioning from low income to middle income is only 5 percent and from middle to high income is only 18 percent—even in the very long run (140 years).

Explanations for Income Traps

The literature lacks systematic explanations for the lack of rapid convergence, especially the middle-income trap phenomenon. We discuss the theories that stand out, in our view, as the most prominent. The general theme underlying these theories is that there are barriers to technology spillovers and frictions in resource reallocation.

First, a developing country's local monopoly power can act as a barrier to new technology adoption and international capital flows. Interest groups in developing countries have little incentive to open up the domestic market and allow competition from foreign firms with more advanced technologies. There is empirical evidence to support this theory, but it does not explain why nations remain trapped in low- or middle-income levels even when they adopt policies to open domestic markets or when they enact radical economic reforms that lift barriers to international capital flows. In fact, many nations have tried to attract foreign direct investment (FDI) but have not been very successful; even if they do attract FDI, they are still unsuccessful in climbing out of the income trap.6 For example, Mexico adopted financial liberalization in the 1970s, accumulating a large amount of debt. But when the U.S. hiked interest rates in the early 1980s, Mexico suffered a debt crisis, partly because of its lack of capital controls. As another example, Russia also adopted dramatic economic and political reforms to lift capital controls, starting in the early 1990s, but the result was a collapsing economy, not a reviving one.

A second popular theory to explain the income traps focuses on institutions. This theory proposes that poor nations fail to develop because of bad political institutions, such as a dictatorship. Under bad political institutions, the elite class builds extractive economic institutions to expropriate profits from the grass-roots population. Hence, the rule of law and private property rights are not protected, and the private sector has little incentive to accumulate wealth and adopt new technologies to improve productivity.7 Notable examples of the institutional theory are the communist countries in Eastern Europe during the postwar period before their economic reform in the late 1980s and early 1990s, as well as today's North Korea.

The institutional economists also apply this theory to explain why the Industrial Revolution took place first in late 18th century England instead of in other parts of Europe. They argue that this was because England had the best political institutions in the world, thanks to the 1688 Glorious Revolution, which strengthened private property rights by restricting the British monarch's extractive power on the British economy.

However, the institutional theory's explanation of the Industrial Revolution based on the notion of better private property rights has been criticized by many economic historians; they argue that private property rights and the rule of law in many countries outside England, such as 18th century China, were just as secure (or even more so) as those in England, yet the Industrial Revolution did not happen there.8

Furthermore, the institutional theory does not entirely explain the mechanism of economic development, and it is inadequate to explain instances such as Russia's dismal failure to grow after the shock therapy economic reform in the 1990s or China's miracle growth since 1978 under an authoritarian political regime. A similar case can be made about areas with identical political and economic institutions, such as the different counties within the American cities of St. Louis or Chicago, or the different parts of northern and southern Italy, where there are sharp contrasts of both pockets of extreme poverty and blocks of extreme wealth, both violent crime and obedience to the rule of law.

Instead, both regional economic inequality and the failure or success stories of nations that have attempted industrialization could be explained by the specific development strategies and industrial policies adopted, rather than by the political institutions per se.9 In what follows, we will use the experience of Mexico and Ireland to shed light on the middle-income trap.

The Cases of Ireland and Mexico

To further investigate the issue of why some countries have failed to climb the income ladder and others have succeeded, we dig deeper into the diverging cases of Ireland and Mexico. Both countries maintained a roughly similar level of development in terms of per capita income going back as early as the 1920s. However, each took dramatically different approaches to development in the postwar era, leading to the different outcomes seen, especially after the 1980s. This occurred despite both nations' adopting political democracy: Mexico in 1810 and Ireland in 1921. Ireland's economy did not experience fast growth between the 1920s and the 1950s because of anticolonial policies based on the since-discredited strategy of import substitution industrialization. However, since the 1950s, Ireland used its state's capacity built in the previous period and adopted industrial policies to gradually open up to global markets to attract FDI, instead of fully liberalizing its capital markets at once. Moreover, special government agencies were created to guide and steer such foreign investment through preferential policies (subsidies) and proper regulations to nurture its manufacturing sector. Ireland also increased government spending on public education for all and adopted new tax, fiscal and monetary policies to control high government deficits and inflation; in addition, it promoted domestic investment and targeted its exports to Europe and the U.S.10

On the other hand, Mexico was a far more open economy than Ireland between the 1920s and 1970s, but Mexico lacked sufficient government effort and discipline to build its state capacity to steer the economy. Mexico's exposure to international oil markets as an oil exporter, as well as the rapid expansion of public debt in the 1970s, made the economy susceptible to more liquid short-term capital flows, instead of longer-term foreign investment. Its large government debt became very expensive after the interest rates in the U.S. were increased drastically to curb inflation, pushing the Mexican economy into default and prompting a large currency devaluation.

Moreover, Mexico did not invest highly in education, nor did it establish government agencies to design industrial policies to promote both foreign and domestic investment in areas consistent with Mexico's comparative advantages. Economic reform and nationalization of the banking system in the early 1980s prompted investors to look for financing outside of the banking system, changing the financial landscape and failing to stimulate industrial growth that would invigorate the economy.11 Financial liberalization at the end of the 1980s, oil export-led growth and eventual debt restructuring helped stabilize the economy, though rapid economic growth did not return.

Comparing the divergent growth paths of Mexico and Ireland in the 20th century suggests that state capacity and industrial policies are critical in explaining the issue, rather than differences in political institutions or vast interests of local monopolies, per se. Unlike what the Solow growth model suggests, technology is embedded in tangible capital, which is most likely to originate from the manufacturing sector instead of the agricultural and natural resource sector or service sector. Hence, advanced technology only flows from developed nations into developing nations through costly fixed investment in manufacturing. Financial capital investors from developed countries are typically interested in short-term capital gains (especially in real estate and natural resources), not in the foreign nation's long-term development.

Such types of capital flows should be controlled, instead of encouraged, by developing countries' governments. Thus, those nations that can find ways to grow their manufacturing sector through continuous investment and domestic savings are more capable of achieving technological and income convergence to the technology frontier of the world.12

Income Transition Probabilities between 1950 and 2011

| A: 10-Year Transitions | ||||

| Ending Point | ||||

| ≤15% | >15 to 50% | >50% | ||

| Starting Point |

≤15% | 0.94 | 0.06 | 0.00 |

| >15 to 50% | 0.09 | 0.80 | 0.11 | |

| >50% | 0.00 | 0.03 | 0.97 | |

| B: 20-Year Transitions | ||||

| Ending Point | ||||

| ≤15% | >15 to 50% | >50% | ||

| Starting Point |

≤15% | 0.90 | 0.10 | 0.00 |

| >15 to 50% | 0.14 | 0.65 | 0.21 | |

| >50% | 0.00 | 0.03 | 0.97 | |

| C: Start-to-End Transitions (30 to 61 Years) | ||||

| Ending Point | ||||

| ≤15% | >15 to 50% | >50% | ||

| Starting Point |

≤15% | 0.80 | 0.16 | 0.03 |

| >15 to 50% | 0.17 | 0.47 | 0.36 | |

| >50% | 0.00 | 0.00 | 1.00 | |

SOURCES: Penn World Tables 8.0 and authors' calculations.

Income Transition Probabilities between 1870 and 2010

| A: 10-Year Transitions | ||||

| Ending Point | ||||

| ≤15% | >15 to 50% | >50% | ||

| Starting Point |

≤15% | 0.94 | 0.06 | 0.00 |

| >15 to 50% | 0.08 | 0.83 | 0.09 | |

| >50% | 0.00 | 0.10 | 0.90 | |

| B: 20-Year Transitions | ||||

| Ending Point | ||||

| ≤15% | >15 to 50% | >50% | ||

| Starting Point |

≤15% | 0.92 | 0.08 | 0.00 |

| >15 to 50% | 0.13 | 0.75 | 0.12 | |

| >50% | 0.00 | 0.12 | 0.88 | |

| C: Start-to-End Transitions (30 to 140 Years) | ||||

| Ending Point | ||||

| ≤15% | >15 to 50% | >50% | ||

| Starting Point |

≤15% | 0.93 | 0.05 | 0.02 |

| >15 to 50% | 0.31 | 0.51 | 0.18 | |

| >50% | 0.00 | 0.17 | 0.83 | |

SOURCES: Maddison Project (2013) and authors' calculations.

NOTES FOR TABLES 1 AND 2: Each number represents the percent of economies that transitioned from a given relative income range at the beginning of the period (row headers) to the respective relative income range at the end of the period (column headers) during the period specified. For example, Panel A in Table 1 shows that between 1950 and 2011, a country with a relative income lower than 15 percent of that of the U.S. had a 94 percent probability of remaining in the relative low-income trap after 10 years, while a middle-income country had an 80 percent probability of remaining in the relative middle-income trap and a 9 percent probability of regressing to a low relative income status. In other words, the probability of escaping the low-income trap after 10 years was 6 percent and that of escaping the middle-income trap was 11 percent.

Endnotes

- See Solow for a theoretical description of the neoclassical growth model. More recently, economist Robert Barro presented the "iron law of convergence," suggesting poor countries can constantly reduce their income gap with the developed economies by half every 35 years. [back to text]

- "Middle-income trap" is a term that was first used by economists Indermit Gill and Homi Kharas in 2007 in reference to countries that have maintained a middle-income status for decades without being able to reach high-income status. [back to text]

- The countries in Europe's periphery were strongly affected by the housing bubble burst and financial crisis during the late 2000s. [back to text]

- A similar analysis was done by Im and Rosenblatt. We calculated income relative to that of the U.S. using real GDP data at chained purchasing power parities (PPPs) from Penn World Table 8.0 for 107 countries that have a population larger than 1 million and at least 30 years of data between 1950 and 2011. We excluded Middle Eastern countries because most are oil-rich economies. [back to text]

- We repeated the procedure using income data from the Maddison Project, available since 1870 for 104 countries in our sample. U.S. income per capita was more than 75 percent of that of Great Britain in the 1870s; so, the U.S. was still a good representative of the developed world at the time. [back to text]

- See Parente and Prescott. [back to text]

- See Acemoglu and Robinson. [back to text]

- See Allen. [back to text]

- See Wen. [back to text]

- For a report on Ireland's development process, see http://www.heritage.org/europe/report/executive-summary-how-ireland-became-the-celtic-tiger. [back to text]

- See research.stlouisfed.org/publications/review/07/09/HernandezMurillo.pdf. [back to text]

- For example, Wen analyzes China's growth miracle. [back to text]

References

Acemoglu, Daron; and Robinson, James A. Why Nations Fail: The Origins of Power, Prosperity, and Poverty. New York: Crown Publishers, 2012.

Allen, Robert C. The British Industrial Revolution in Global Perspective. New York: Cambridge University Press, 2009.

Barro, Robert J. "Convergence and Modernization." The Economic Journal, June 2015, Vol. 125, No. 585, pp. 911-42.

Gill, Indermit; and Kharas, Homi. An East Asian Renaissance: Ideas for Economic Growth. Washington, D.C.: The World Bank, 2007.

Im, Fernando G.; and Rosenblatt, David. "Middle-Income Traps: A Conceptual and Empirical Survey." Policy Research Working Paper No. 6594, The World Bank, September 2013.

Maddison Project. See www.ggdc.net/maddison/maddison-project/home.htm for the 2013 version.

Parente, Stephen L.; and Prescott, Edward C. Barriers to Riches. Cambridge, Mass.: MIT Press Books, 2002.

Solow, Robert M. "A Contribution to the Theory of Economic Growth." The Quarterly Journal of Economics, February 1956, Vol. 70, No. 1, pp. 65-94.

Wen, Yi. "The Making of an Economic Superpower—Unlocking China's Secret of Rapid Industrialization." Working Paper No. 2015-006B, Federal Reserve Bank of St. Louis, June 2015.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us