District Overview: Household Financial Stress Declines in the Eighth District

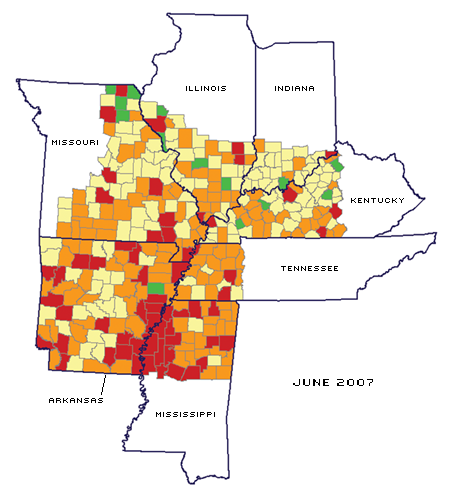

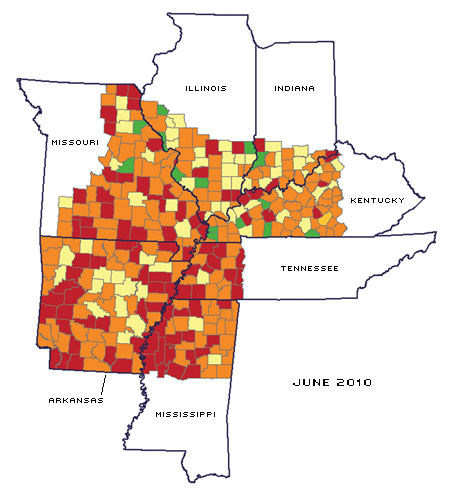

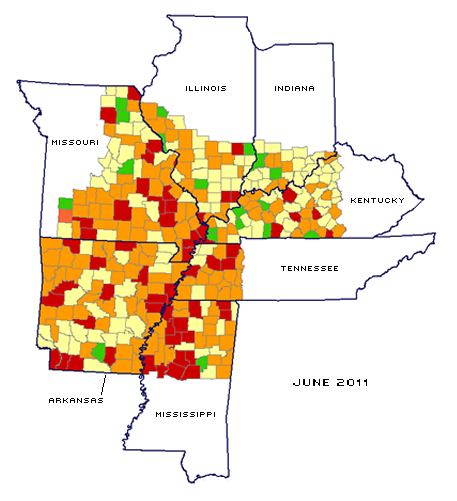

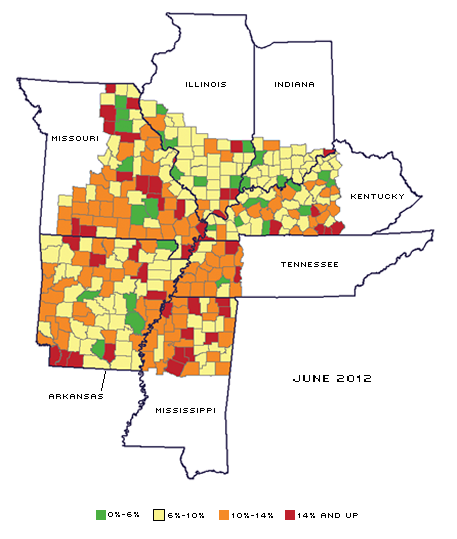

Recent data on consumer debt—particularly credit card loans, consumer finance loans and retail loans—suggest that more households in the Eighth Federal Reserve District are paying their debts on time. A measure of financial stress that is typically used in the consumer debt segment is the portion of consumer debt balance that is delinquent for at least 90 days, also known as the serious delinquency (SD) rate. In June 2012, this rate in the District fell to 9.94 percent, moderately lower than the 11.97 percent national average. Moreover, the District's rate not only recovered from its peak of 12.29 percent in March 2010, but also dropped below its prerecession level of 10.18 percent in June 2007.

Figure 1 shows how the delinquency rates across states in the District have witnessed a recovery.1 In 2007, Mississippi had the highest SD rate—13.58 percent. This rate dropped to 13.31 percent in June 2010 and dropped further to 10.75 percent in June 2012. The SD rate for Tennessee was 12.28 percent in 2007; it rose to 14.14 percent in June 2010, the highest among District states then. Although the SD rate in Tennessee recovered to 12.09 percent as of June 2012, it remains the highest among the District's states.

The SD rates for Arkansas, Illinois and Kentucky have also recovered; the rates currently are 9.63, 8.77 and 8.82 percent, respectively—below both their June 2010 and prerecession levels. In contrast, SD rates in Indiana and Missouri remain above their prerecession levels, although they are lower than their June 2010 peaks. They are currently at 8.58 percent and 10.44 percent, respectively.

Evolution of the Serious Delinquency (SD) Rate

SOURCE: Federal Reserve Bank of New York Consumer Credit Panel/Equifax.

NOTE: "Serious delinquency" refers to consumer debt that is at least 90 days past due.

Personal Bankruptcies

Trends in nonbusiness bankruptcy filings offer another indicator of financial stress for consumers. The most common forms of nonbusiness bankruptcy filings are either under Chapter 7 (straight liquidation) or under Chapter 13 (repayment plan) of the U.S. Bankruptcy Code. A Chapter 7 bankruptcy results in the liquidation of a debtor's nonexempt assets and the elimination of any unsecured debt, thus giving the debtor a fresh start. In contrast, a Chapter 13 bankruptcy offers a repayment plan and conditionally protects the debtor's properties. Such a petitioner can only become debt-free after fulfilling the terms and conditions set out in the repayment plan. (This usually involves repayment of a portion of the original debt within 3-5 years.)

During the late 1990s and early 2000s, bankruptcy filings under Chapter 7 witnessed a sharp increase, prompting creditors to lobby Congress for legal changes.2 Under the new Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, petitioners filing under Chapter 7 are required to (i) have monthly income less than or equal to the applicable state median income; or (ii) pass a means test.3 A debtor who does not qualify is still eligible to file under Chapter 13. Moreover, some debtors who initially declare bankruptcy under Chapter 13 can become eligible to file under Chapter 7 at a later date if their financial situation worsens.

Since factors such as state median income, local cost of living, family size and individual characteristics all affect the bankruptcy eligibility, the bankruptcy filings per capita vary across the metropolitan statistical areas (MSAs) of the Eighth District.

Bankruptcy filing rates (per 1,000 people) under Chapter 7 and 13 for selected MSAs in the Eighth District are given in the table. The Texarkana, Pine Bluff, Jackson and Jefferson City MSAs had the lowest Chapter 7 bankruptcy rates in 2011: below 2.5. Jonesboro with 7.75 and St. Louis, Bowling Green and Evansville with about four bankruptcies per 1,000 people were the MSAs with the highest Chapter 7 filing rates last year. Among other major District MSAs, Little Rock had 2.72, Louisville had 3.65 and Memphis had 3.49 Chapter 7 bankruptcies per 1,000 people. Out of a total of 19 MSAs in the Eighth District, the Chapter 7 bankruptcy rate last year in 14 MSAs had dropped from the 2010 levels but remained above the prerecession (2007) levels.

For Chapter 13 filings, the Owensboro, Bowling Green, Springfield and Columbia MSAs had the lowest rates in 2011. They all had one or fewer filings per 1,000 people. On the other hand, Little Rock, Jackson, Pine Bluff and Memphis were among the MSAs with the highest Chapter 13 filing rates, those being 3.40, 5.49, 6.39 and 8.41 per 1,000 people. Among other major District MSAs, filings in Louisville and St. Louis totaled 2.04 and 1.76 per 1,000 people, respectively, last year. In 12 out of the 19 District MSAs, the Chapter 13 bankruptcy filings last year dropped below the prerecession levels.

Interestingly, the Pine Bluff and Jackson MSAs are among the MSAs with the highest filing rates under Chapter 13 but also among MSAs with the lowest filing rates under Chapter 7. While the overall bankruptcies for these two MSAs are more or less in line with District-wide rates, their composition is widely different. It is possible that filings under Chapter 13 are high because most households declaring bankruptcies in these MSAs do not qualify to file under Chapter 7 under the new law. Similarly, Memphis had a Chapter 13 filing rate of 8.41 per 1,000 people last year but its Chapter 7 filing rate was only 3.49 then. On the other hand, the Bowling Green MSA had a high Chapter 7 filing rate but a low Chapter 13 filing rate—possibly because most residents are eligible under the new law.

Overall, despite the slow recovery nationwide, bankruptcy filing rates for most of the MSAs in the Eighth District are on the decline.

Endnotes

- All data on states and metropolitan statistical areas (MSAs) here refer to the portions that lie within the Eighth District. [back to text]

- See White. [back to text]

- A means test determines whether the debtor can repay a portion of the unsecured debt

defaulted upon with his or her current monthly income (less a set of allowed deductions stipulated by the IRS). If the debtor is unable to repay, he or she is deemed to have passed the means test. [back to text]

References

White, Michelle J. "Bankruptcy Reform and Credit Cards." Journal of Economic Perspectives, Vol. 21, No. 4, 2007, pp. 175-200.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us