National Overview: Signs Point to Stronger Real GDP Growth in 2012 than Last Year's 1.6

The macroeconomic environment continued to improve over the first half of 2012, despite some headwinds that dampened confidence among small businesses, households and investors. Among the key headwinds have been the renewed turmoil in Europe, high gasoline and diesel prices, and uncertainty about the current and future direction of economic and regulatory policies. Impressively, though, the nation's unemployment rate, while still high, has fallen much faster than forecasters had expected a year earlier. On balance, recent data and forecasts suggest that economic activity remains on pace to surpass last year's lackluster rate of growth (1.6 percent).

GDP Growth Slows

Real GDP growth slowed to an annual rate of about 2 percent in the first quarter after rising at an annual rate of 3 percent in the fourth quarter of 2011. An early reading

of the data in April and May suggests that the pace of growth may have been somewhat faster in the second quarter than in the first quarter. In particular, consumer expenditures and business outlays for equipment and software remain solid, as does the pace of U.S. exports. In response, the manufacturing sector has flourished, and private-sector payroll gains have averaged about 170,000 per month since the first of the year—notwithstanding the weaker-than-expected May employment report. Importantly, residential homebuilding activity continues to pick up and home prices appear to have stabilized—and have even risen slightly by some measures. However, a noticeable pullback in real government expenditures over the past year and a half has tempered the overall gains in economic activity.

In further signs of improving sentiment, consumer credit growth has accelerated over the past six months, and commercial and industrial loans have risen sharply. Residential mortgage lending also has begun to pick up. Extremely low interest rates have helped to fuel the rebound in bank lending and credit growth and have allowed homeowners to refinance existing mortgages. The sharp decline in long-term interest rates in May and June—along with a modest correction in stock prices—probably reflects recent developments in Europe, which have, at least temporarily, reversed the depreciation of the U.S. dollar that began in late 2009.

The recovery from the 2007-09 recession has been one of the weakest in the post-World War II period and has raised questions about the economy's underlying pace of growth (also termed the growth of real potential GDP). One possibility is that the recession and financial crisis have permanently lowered the economy's growth of potential output. Another possibility is that the economy is growing faster than the GDP numbers suggest, as evidenced by a modestly faster rate of growth of the income-side measures of the national accounts. Hopefully, the annual revision to the national income accounts in late July will resolve this tension in the data.

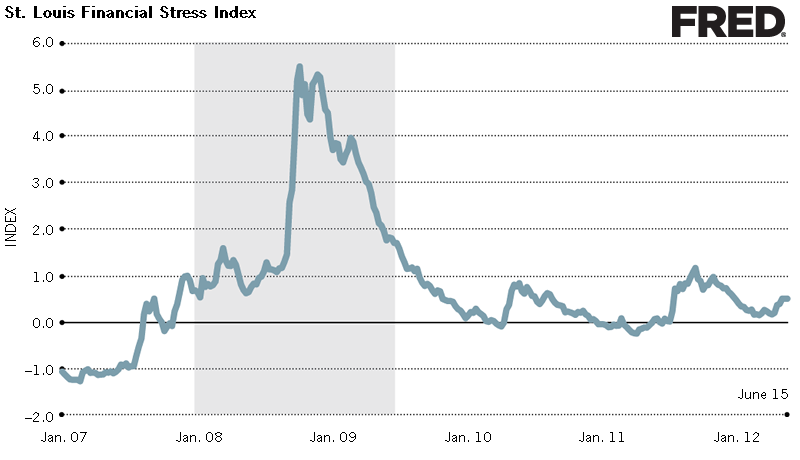

The Greek Drama: Round Three

Economic and political developments in Europe dominated the financial headlines in May and early June. Citing concerns about the possibility of a Greek withdrawal from the Economic and Monetary Union (EMU), some European officials have warned of a significant short-term economic disruption. These fears have elevated uncertainty among U.S. financial market participants and firms that have important linkages to Europe. A further complication is the likelihood that Europe—except for Germany and a few other northern countries—has slipped back into recession. Unlike in the spring of 2010 and the summer of 2011, round three of the European turmoil has spurred only a modest upturn in the St. Louis Financial Stress Index; it remained only modestly above normal (which is zero) in mid-June.

{kind=link}

Some Good News on Inflation

Headline price pressures have eased since the fall of 2011. Following an increase of nearly 4 percent in September 2011 (measured on a 12-month basis), Consumer Price Index (CPI) inflation slowed to a rate of about 2.25 percent in April 2012. This moderation reflects a weaker trajectory of oil and commodity prices beginning in early March and a significant slowing in food prices. Some slowing in global growth prospects, arising from weaker growth in China and Europe, has reinforced the view of many forecasters that oil prices could continue to fall. However, recent tension in the Middle East poses a risk to the profile of future oil prices. Nevertheless, concerns about the possibility of faster inflation rates over the near term do not appear widespread in financial markets. Moreover, professional forecasters expect the CPI inflation rate to be between 2 and 2.5 percent this year, modestly below the 3 percent rate of last year. These expectations have changed little in recent months.

FRED® is a registered trademark of the Federal Reserve Bank of St. Louis.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us