Where's the Wage Pressure?

A classic TV advertisement is the "Where's the beef?" commercial. For those not up-to-speed on '80s pop culture, customers at a fast-food restaurant order a hamburger, express enthusiasm over the large bun and expect to find a sizable patty inside. Instead, they find a tiny piece of meat, and a woman exclaims, "Where's the beef?!"

The analogy to the current discussion in the press and in policymaking circles is that, while the recovery has brought improvement in many output and labor-market indicators, wages have been flat. In particular, many people expect that the decline in unemployment will cause a rise in the mean wage. The logic is simple: As jobs become more plentiful, workers have more alternatives, requiring employers to pay higher wages to keep them.

But the real world is more complicated. There are more powerful drivers of wages than the average ability of workers to quit and find another job. The changes in wages over a business cycle, such as the Great Recession and recovery, are minute compared with the gradual changes to the wage structure that have occurred over the past few decades.

The wide distribution of wages also complicates the relationship between wages and the unemployment rate. The spread is so wide that the mean wage is a poor measure of the well-being of most workers. Workers at the top of the wage distribution are affected much differently than workers at the bottom. High-wage earners have a higher job-finding rate and are already able to move more easily from job to job; so, labor market conditions have less of an impact on their bargaining power and, therefore, on their wages. In contrast, workers who earn less than the median wage have a lower job-finding rate and are less likely to be able to move directly from job to job. These workers have fewer alternatives than higher-paid workers; so, an improvement in labor market conditions more directly impacts their bargaining power and wages.

Furthermore, the distribution of wages has changed over time. Long-term trends, rather than short-term fluctuations, have widened the distribution. These increasing differences between rich and poor are vastly more important to workers than the small, cyclical differences in wages at a given point in the distribution. The higher percentiles of the wage distribution are pulling away from the median for reasons that pre-date the Great Recession of 2007-09. As the wage distribution changes, the impact of the unemployment rate on wages may also change.

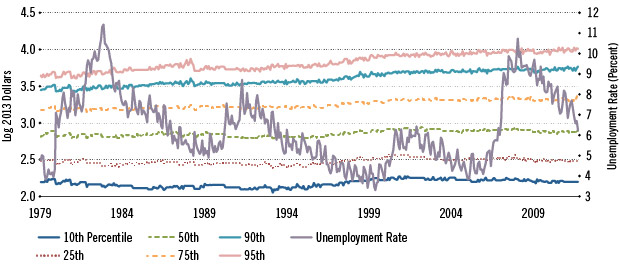

In the figure, we see that wages move slightly as the unemployment rate fluctuates, but that these movements are small compared to long-run trends. We also see that the gap between the highest and lowest earnings percentiles has widened independent of any movements in the unemployment rate.

With this in mind, we looked at the correlation between unemployment and wages at various percentiles of the wage distribution. (See table.) As we might expect, higher levels of wages were less correlated with the unemployment rate. However, at each level of wages, the correlation was quite low. This feature of the data is nothing new: The weakness in the cyclicality of wages is well-established. During the Great Recession, this correlation became slightly weaker, but the difference is not economically or statistically significant.

That is not to say that business cycle indicators do not tend to move together, nor is this article intended to be overly optimistic about the state of the labor market. However, reading too much into cyclical movements of the mean wage seems misguided. Wage pressure is not really the beef of the hamburger. If anything, it's the pickle.

Unemployment and Hourly Wages

SOURCES: Bureau of Labor Statistics and authors' calculations.

NOTE: Wages are adjusted for inflation and shown in log dollars. In log dollars, a straight line represents a constant rate of growth, with steeper lines indicating higher growth rates. The unemployment rate, as it goes up and down, has very little impact on wages for any group of earners. (The 10th percentile represents the lowest-wage earners, and the 95th percentile represents the highest.) Over the long term, wages are growing more for those at the top of the wage distribution than at the bottom.

Correlation between Wages and the Unemployment Rate

| 1979-2013 | |||||||

|---|---|---|---|---|---|---|---|

| Wage Percentile | 10th | 25th | 50th | 75th | 90th | 95th | Mean |

| Same Month | –0.17 | –0.20 | –0.14 | –0.15 | –0.14 | –0.08 | –0.14 |

| Two-Month Lead | –0.18 | –0.21 | –0.14 | –0.15 | –0.15 | –0.09 | –0.15 |

| Post-recession, 2007-2013 | |||||||

| Same Month | –0.12 | –0.17 | –0.09 | –0.13 | –0.17 | –0.18 | –0.09 |

SOURCES: Bureau of Labor Statistics and authors' calculations.

NOTE: To remove the effects of long-term trends, we detrended log wages at each percentile before calculating the correlations. Therefore, the correlations show how wages move relative to trend as the unemployment rate changes. Negative numbers indicate that the wage falls as the unemployment rate rises, and numbers farther from zero indicate a stronger relationship. The same-month numbers show the correlation between the unemployment rate and wages in the same month. The two-month lead numbers show the correlation between the unemployment rate in the current month and wages two months later. The two-month lead numbers are slightly more negative than the same-month numbers, indicating a delayed impact from the change in the unemployment rate. The correlation grows weaker as we move up the income distribution. However, for all percentiles and for the mean, the relationship is not strong.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us