Sovereign Debt Crisis in Europe Recalls the Lost Decade in Latin America

The recent European debt crisis may seem like déjà vu. Many of its characteristics are reminiscent of the Latin American debt crisis of the 1980s, which led to what is known as the lost decade. In this article, we explore the similarities of and point out the differences between both crises.

Similarities

During the 1970s, Latin America was experiencing an era of high growth. Output, investment and per capita consumption were surging. The excess liquidity generated by oil-exporting countries when oil prices rose and the resulting high savings of those countries facilitated borrowing abroad. This borrowing was supposed to finance infrastructure projects but ended up financing consumption.

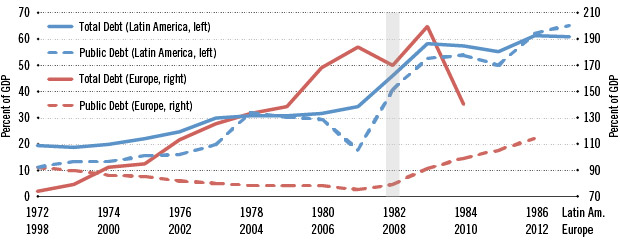

However, after 1979, an increase in oil prices by the Organization of the Petroleum Exporting Countries (OPEC) led to the start of what is known as the Volcker era. Paul Volcker, then the chairman of the Federal Reserve, increased interest rates sharply in order to control inflation in the U.S. economy, causing payments on foreign debt to become more expensive for Latin America, which had borrowed heavily from U.S. banks. Most Latin American countries were oil importers at the time; so, higher prices for imported oil, combined with the now more expensive debt, should have generated an adjustment in borrowing and spending. Instead, debt went from being 30 percent of gross domestic product (GDP) on average in 1979 to nearly 50 percent in 1982 for the larger Latin American countries. (See Figure 1.) This situation became unsustainable and ended up with Mexico's default in 1982, followed soon by the default of other countries in the region.

The picture is quite similar for peripheral Europe. Greece, Spain, Portugal and Ireland were getting capital inflows since the beginning of the 2000s. (See Figure 2.) These newfound resources were meant to finance investment. Instead, as in Latin America, the excess liquidity went to finance a consumption boom. Debt went from being 90 percent of GDP on average in 2000 to 200 percent in 2009 (see Figure 1), right before Greece first requested financial aid from the International Monetary Fund. Similarly, debt-to-GDP ratios soared in Spain, Portugal and Ireland, which also sought financial support to pay their sovereign debts in the following years.

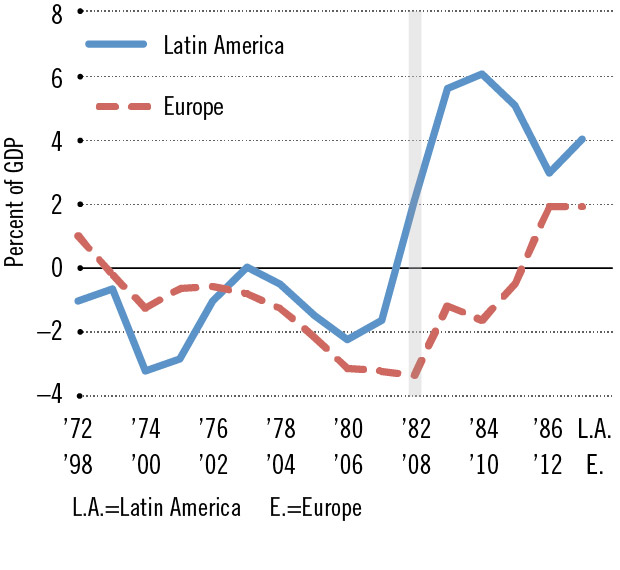

So, in both Latin America prior to the 1980s and peripheral Europe at the start of the 21st century, output, investment and consumption were growing rapidly. Liquidity levels were extraordinarily high and were accompanied by capital inflows and fast-rising levels of debt to GDP. Then, an external shock struck, making the situation unsustainable. Capital flows reversed (see Figure 2), and many countries defaulted.

What Was Different?

The kind of external shock that triggered each of the crises, the composition of the debt, the interest rates that the regions were facing and the relationships among the countries involved were different.

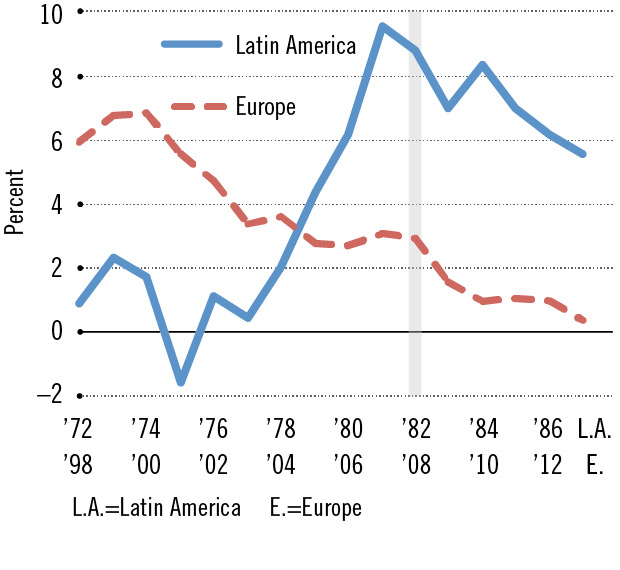

For Latin America, the external shock was the hike in U.S. interest rates, which was a consequence of the rise in oil prices. For Europe, the Great Recession of 2008-09 triggered the crisis.

Figure 1 shows the composition of the debt-to-GDP ratio in both regions. The solid lines depict total debt, while the dashed lines show only public debt. Note that for Latin America, public debt was driving the increase in total debt, while in Europe, private debt was actually driving the increase in total debt.

Figure 3 shows the respective real interest rate that was being faced by Latin America and peripheral Europe in the years preceding and during the crises.1 As discussed above, it is clear that Latin America was enjoying low interest rates prior to the crisis and then experienced a sharp rise in rates at the beginning of the 1980s. Europe, on the other hand, faced much higher interest rates from the start; those interest rates continuously decreased over time.

Figures 1 and 3 portray the main differences between both crises. The jump in interest rates for Latin America made the debt very expensive to repay, leading countries to default by failing to service their debt. The relatively high level of debt held by countries in Europe's periphery simply became unsustainable when output, investment and per capita consumption started to decline after the Great Recession.

The Aftermath

The Latin American debt crisis resulted in the well-known lost decade for the region, during which initial fiscal readjustments and austerity did little but reinforce anemic growth. Currency devaluation, an emphasis on trade expansion (see Figure 2) and eventually debt restructuring through what was known as the Brady Plan helped the countries in the region regain strength and return to economic growth.

As for the situation in Europe, being part of the Economic and Monetary Union (EMU) without having broader fiscal integration limited what policies could be implemented by the individual countries to jump-start the economy after the crisis. Austerity measures and some debt restructuring have been part of monetary authorities' response. But the European Union has moved to integrate even further by creating joint supervisory authorities and a closer fiscal union, including the most recent banking union, which took effect Nov. 4, 2014. Ultimately, more unified coordination and governance could strengthen the fiscal union and lead to greater economic stability.

Total Debt and Public Debt by Region

SOURCES: International Monetary Fund, Penn World Tables, Reinhart and Rogoff, and author's calculations.

Net Exports by Region

SOURCE: World Bank

NOTE: Net exports can be used as a proxy to reflect net capital flows, whereby negative net exports represent a positive capital inflow to the region.

Real (Inflation Adjusted) International Lending Rate

SOURCE: International Monetary Fund

NOTE FOR ALL FIGURES: Data in each figure represent aggregate averages for select Latin American countries between 1972 and 1987 and for select European countries between 1998 and 2013. The Latin American countries in the sample are Argentina, Brazil, Chile and Mexico, while the European countries in the sample are Greece, Ireland, Italy, Portugal and Spain. The gray vertical bar represents the start of the debt crisis in both regions: 1982 in Latin America and 2008 in Europe.

Endnote

- The interest rate for Latin America corresponds to the rate posted by a majority of the top 25 insured U.S.-chartered commercial banks (by assets in domestic offices), while that for Europe is the average of the respective rates posted by banks in Germany, France and Great Britain—the primary lenders for the peripheral European countries. The real lending interest rate is calculated using the GDP deflator. [back to text]

References

Eichengreen, Barry. "Latin Lessons for the Euro Zone." Manuscript, University of California, Berkley, January 2010.

European Central Bank. "ECB Assumes Responsibility for Euro Area Banking Supervision." Press release. Nov. 4, 2014. See www.ecb.europa.eu/press/pr/date/2014/html/pr141104.en.html.

Reinhart, Carmen M.; and Rogoff, Kenneth S. This Time Is Different: Eight Centuries of Financial Folly. New Jersey: Princeton University Press, 2009.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us