Rising Oil Prices and Economic Turmoil: Must They Always Go Hand in Hand?

After falling sharply during the Asian financial crisis in late 1998, market prices of crude oil and other energy products climbed in November 2000 to their highest levels since the Gulf War. The oil price shock, as economists have coined it, occurred as monetary policy-makers acted to keep the economy from overheating. This combination of events has raised a few red flags in certain quarters, since nearly all post-World War II recessions were preceded by higher oil prices and a restrictive monetary policy. Unlike other oil price shocks since the 1970s, however, the current run-up in energy prices has not yet raised the alarm one might have expected. Indeed, while the pace of U.S. economic activity appeared to slip noticeably during the fourth quarter of 2000, most forecasters continue to project solid growth and moderate inflation for the next two years. Is the U.S. economy better positioned today to withstand the body blows of sharply higher oil prices than it was in the past?

Oil Price Shocks in U.S. Economic History

An oil price shock is one of several possible disturbances to a country's aggregate price level. Its significance reflects the fact that crude oil is an important energy source for most industrialized countries, who use energy as a direct or indirect input in the production of most goods and services. Because higher oil prices tend to raise the prices of petroleum-based products and alternative sources of energy, such as natural gas, the aggregate price level will rise unless the prices of all other goods and services fall to offset the rise in oil prices. Of course, oil price shocks are not always one-sided. Prices of crude oil can also fall in significant fashion, as they did in 1986 and 1998. On balance, though, the public and policy-makers tend to think of oil price shocks as energy price increases, hence, the adverse connotation.

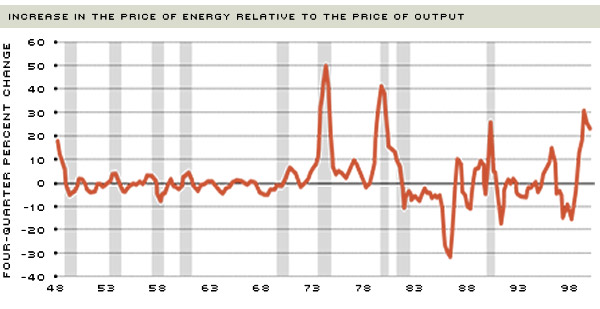

In the early post-World War II period, the run-up in energy prices prior to economic downturns was comparatively mild. During the four quarters preceding the onset of the 1948-49, 1953-54, 1957-58, 1960-61 and 1969-70 contractions, the relative (real) price of energy increased a little more than 1.5 percent, on average. These increases, however, were tempered by the fact that the relative price of energy actually declined 2.4 percent and 1 percent prior to the 1960-61 and 1969-70 contractions, respectively—though energy prices subsequently rose sharply in the midst of these two recessions.

The figure below shows that energy price changes have been much more pronounced (relative to output prices) since the early 1970s. The average increase in real energy prices prior to the onset of the four recessions during this period—1973-75, 1980, 1981-82 and 1990-91—was 17.5 percent, much greater than in earlier recessions. Except for the 1990-91 recession, one of the mildest since World War II, the contractions of the 1970s and 1980s were the deepest since the Great Depression. Though U.S. economic growth remained solid through the third quarter of 2000, the 23 percent increase in real oil prices from four quarters earlier is nevertheless large in historical terms.

Rising Oil Prices Have Usually Preceded Most Recessions

As the figure shows, nearly all post-World War II recessions in the United States were preceded by, or accompanied by, a sharp increase in energy prices relative to the aggregate price level. As a result, oil price shocks tend to be viewed with alarm by macroeconomists, markets and public policy-makers. This heightened sense of concern is largely an outcropping of the 1970s and 1980s.

NOTE: Producer Price Index for Fuels and Related Products and Power (not seasonally adjusted) divided by the price index for Business Sector Output. Shaded areas are periods of recessions, as defined by the National Bureau of Economic Research.

SOURCE: U.S. Bureau of Labor Statistics.

One reason why oil prices have been more volatile since the 1970s has been the advent of the Organization of Petroleum Exporting Countries (OPEC). Economically, OPEC is a cartel—a type of oligopoly that attempts to keep prices above their competitive levels by actively adjusting crude oil supplies. Last year, for example, OPEC oil ministers announced that they intended to alter production to keep the market price of crude oil between $22 and $28 a barrel. OPEC has also tried to manipulate prices for political reasons. The best-known example was the 1973 Arab oil "embargo," which sought to punish the United States for its support of Israel during the Arab-Israeli War.

Ultimately, OPEC's ability to manipulate market prices is limited, since oil is a readily fungible commodity—that is, it is traded internationally and its U.S. price depends not only on domestic supply and demand, but also on foreign supply and demand. Moreover, its power is further limited because many of the largest oil-producing countries—such as the United States, Russia, Mexico and Norway—are not OPEC members.

Nevertheless, the cartel has considerable influence on crude oil prices simply because OPEC countries control roughly 40 percent of world production. But OPEC is not the only reason for increased volatility of world energy prices during the past 30 years or so. Another possible reason is the deregulation of U.S. energy markets in the late 1970s and early 1980s. Because price determination is now largely a function of market forces, economic or political developments can sometimes engender wide swings in oil prices if markets are caught unaware.

A salient feature of most oil price shocks since the 1970s has been a change in the amount of oil supplied, or the expectation of a disruption in the oil supply (such as during the Gulf War). But oil price shocks can also occur when the demand for oil rises or falls relative to the supply.1 Indeed, the price of imported oil plummeted to below $10 a barrel in late 1998 because of a marked slowing in the growth of world oil consumption—reflecting, importantly, the significant declines in economic activity in South-east Asia. Even though the subsequent run-up in prices during the past two years occurred while OPEC was trying to limit output to boost prices, steadily faster rates of worldwide economic growth suggest that demand-side influences have also been important in pushing up the price of oil.

Forecasting the future pace of real GDP growth is a high-risk venture even in the best of times. But when the economy is hit with an oil price shock and a modestly restrictive monetary policy, the degree of difficulty increases by several magnitudes. At present, higher energy prices seem not to have rattled consumer confidence. This could obviously change if events take a turn for the unexpected or, as government forecasters expect, household energy expenditures climb markedly higher this winter than they did during last year's relatively benign winter. And whereas the cost structure of firms in industries that are fairly intensive users of energy, like manufacturers, transportation firms and agriculture, also tend to be hit disproportionately when energy prices turn higher, most firms—and by extension, the U.S. economy—have managed to cope with the latest oil price shock rather well.

In view of this development, is there something fundamentally different in the structure of the economy that explains this development, or have policy-makers, particularly the Federal Reserve, done a better job of coping with the current oil price shock?

What's Different This Time?

In December 1998, the price of imported oil plunged to around $9 a barrel. In real terms, this was its lowest level since late 1973. All else equal, this positive price shock should have been good for the economy. But with considerable uncertainty hanging in the air because of the Asian financial crisis, Russian debt devaluation, and the failure of Long Term Capital Management, a majority of U.S. forecasters were predicting a downshift in the pace of U.S. real GDP growth in 1999 to just over 2 percent; they also expected CPI inflation to rise to about 2.3 percent.2 When the first forecasts for 2000 were published in January 1999, Blue Chip forecasters expected continued moderate real GDP growth (2.4 percent) and inflation (2.5 percent), and not much change in the unemployment rate (4.9 percent).3 Needless to say, these forecasts missed their mark by a wide margin. Real GDP growth turned out to be 5 percent in 1999, the strongest growth since 1984, while the unemployment rate dropped to a shade over 4 percent. The brisk pace of economic activity continued into 2000, with real GDP growing at a 4.2 percent annual rate during the first three quarters, and the civilian unemployment rate staying near its 30-year low of 4 percent. CPI inflation tracked higher in 1999 and 2000, as forecasters expected, but largely not for the reasons they cited. And while the oil-induced acceleration in consumer prices in 2000 (3.5 percent through November) is more than most forecasters expected—and, rather troubling when viewed against the relatively good inflation performance from 1992 to 1998—there appears to be little erosion in long-term inflation expectations by the public and most forecasters. Indeed, judging from its continued strong performance, the economy is better positioned to weather this combination of oil price shock and monetary tightening than it was previously.4

On the surface, the recent poor performance of forecasters and—thus far, at least—the ability of the U.S. economy to weather the recent oil price storm appear unconnected.5 But in fact, three developments suggest a closer correspondence. Two developments are largely an outcropping of ongoing structural improvements in the economy stemming from the upsurge in spending on high-tech capital goods. The third development, though somewhat harder to quantify, is better monetary policy,which has resulted in the achievement of near price stability.

Explanation #1: A More Productive Economy

Perhaps the largest difference between the macroeconomic effects of this oil price shock and previous shocks is the underlying performance of the U.S. economy. In particular, it appears that there has been a marked upswing in the economy's capacity to produce goods and services with a given level of inputs like labor, capital and energy. As inputs become more efficient, they earn a higher rate of return: Real wages of labor increase, as do the returns to capital. Invariably, these efficiency gains boost the nation's living standards. Since 1995, per capita real GDP has grown at a 3.2 percent annual rate, far exceeding the 1.8 percent rate of gain from 1973 to 1995. In fact, per capita output growth during the past five years surpasses even the heyday of strong productivity growth from 1947 to 1973, when living standards grew at a 2.4 percent annual rate.

Most forecasters and many academic researchers seem to believe that this improvement is permanent. They have concluded that the U.S. economy can now grow much faster on a sustained basis without sparking an acceleration in inflation—the potential rate of output. For example, in a survey of recent research on this topic, the consensus was that gains in labor productivity stemming from the technological innovations and other advancements have boosted the economy's potential rate of growth by about 1 percentage point during the past five years.6 As a result, compared with the period of slow growth that existed from 1973 to 1995, when most economists figured that potential output growth was around 2 to 2.5 percent, many economists now believe that the economy can grow by around 3.5 percent per year.

The primary reason for this productivity upswing has been the proliferation of computers, advances in telecommunications equipment and the Internet, all of which have dramatically lowered the cost of information-gathering and retooled production and distribution processes. These innovations are embodied in the equipment, software and business practices of firms, enabling a greater amount goods and services to be produced and distributed with proportionately fewer inputs.

One obvious example is in the production of crude oil. Innovations such as horizontal or directional oil drilling techniques, and 3-D and 4-D seismic imaging, today allow energy producers to lift oil from the ground in areas previously considered inaccessible or infeasible. Other innovations include the development of deep-sea drilling and floating production platforms. Soon, the maximum feasible depth of useful production is expected to drop to 7,500 feet, more than triple what it was in the late 1980s.

In the parlance of economists, the economy's production possibilities frontier has been shifting outward from the origin. The ability to produce proportionately more output, accordingly, has enabled firms to keep labor and nonlabor costs in check. At a time when margins are being squeezed by higher labor costs and, more recently, by the sharp increase in energy prices, firms have been able to post significant profits, which have, accordingly, boosted equity prices and engendered other economy-wide benefits.7

Explanation #2: The U.S. Economy is More Energy Efficient

Since energy is an important input into the production of goods and services, efficiency gains arising from technological innovations have necessarily meant that, over time, the United States uses less energy per unit of output. For example, since the early 1970s, the average efficiency of a new refrigerator has nearly tripled, while the average fuel economy of vehicles sold in the United States has doubled. Further improvements are on the horizon. The inevitable switch from the current 14-volt electrical system in automobiles to the more powerful 42-volt system is expected to boost future fuel efficiency by as much as 10 percent.

Whether bushels of corn or wheat, tons of steel, or millions of board feet of lumber, the energy component of U.S. output has been dwindling over time. In 1973, for example, a little more than 18,000 BTUs (British Thermal Units) were required to produce $1 of real GDP in the United States (measured in 1996 dollars). By 1983, the number of BTUs required to produce $1 of real GDP was cut by nearly one-fourth to about 13,750. By 1999, only about 10,500 BTUs were needed to produce $1 of real GDP—more than 40 percent below the 1973 requirements.8

From a competitive standpoint, firms and industries that have most successfully adopted energy-efficient production processes should have an advantage. One way to see how changes in energy efficiency affect economic performance is by considering energy usage by state. In general, states that have above-average increases in energy-efficiency gains—measured as the growth of gross state product relative to total energy consumption from 1977 to 1997—have also experienced faster growth in employment. Conversely, states whose industries have experienced below-average increases in energy efficiency have had modestly slower employment growth.

Explanation #3: Better Monetary Policy

The price system plays an important role in a market economy like the United States. Scarce resources tend to flow to those areas where after-tax returns are the highest (or opportunity costs are the smallest). Crucial in this regard is a low and stable inflation rate—because it helps to minimize risk and uncertainty about future real returns. Indeed, the contours of our record-setting business expansion suggest that price stability has been a key ingredient in firms' decisions to add to their productivity-enhancing stock of capital goods. Firms will thus be less apt to alter investment plans when the believe that rampant inflation will not be the ultimate outcome of an oil price shock.

A key lesson learned by policy-makers during the 1970s was that the amount of money supplied in response to an oil price shock will eventually determine the course of inflation. If the money supply increases relative to the fewer amount of goods and services produced after the shock, then the relative value of money will fall (too much money chasing too few goods). If this continues, the Fed runs the risk of fueling even more inflation, possibly leading people to revise upward their expectation of future inflation. With higher actual inflation and expectations for future inflation now greater than before, the degree of action required by the Fed to bring inflation under control—as the early 1980s demonstrated—will be stronger than if it had acted vigilantly in the first place.

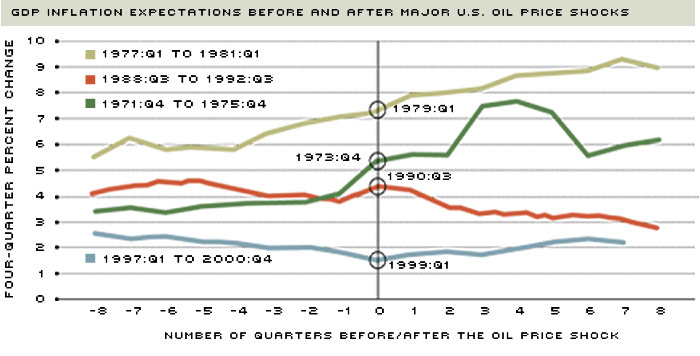

As the figure below shows, monetary policy-makers failed to quell the higher inflation expectations that followed the 1973 and 1979 oil price shocks—that is, they were too accommodative. In the aftermath of those events, expectations of higher inflation were built into planned adjustments in wages and prices, further eroding the purchasing power of the consumer's dollar. Although expected inflation has climbed noticeably since the first quarter of 1999, markets appear confident that the Federal Reserve will not let inflation expectations and, hence, actual inflation, get out of hand—something they appeared to do successfully following the ephemeral 1990 oil price shock. In short, current monetary policy performance has been much better than it was in prior episodes.

Forecasters Expect Much Better Inflation Performance in the Aftermath of the Latest Oil Shock

SOURCE: Survey of Professional Forecasters.

The figure above plots market expectations of inflation (GDP prices) eight quarters before and after four major oil price shocks since the early 1970s. It shows another reason why economic activity has not been appreciably hampered by the current oil price shock: Not only were inflation expectations prior to the oil price surge in the first quarter of 1999 fairly low and stable, but inflation expectations were falling as well. A similar pattern was seen before the Gulf War, though expected inflation was somewhat higher and modestly more volatile. In contrast, prior to the 1973 and 1979 shock, expected inflation was not only higher than in 1999, but it was also rising.

Are Oil Price Shocks Now Off Our Backs?

Oil price shocks have periodically dotted the post-World War II economic landscape. Thus far, however, the severe economic disruption and dislocation that usually followed the spike in oil prices during the 1970s and early 1980s has not come to pass. Indeed, the current outlook for the U.S. economy suggests that oil-induced turbulence might be a relic of the past. The torrent of investment in information and communications technology equipment in recent years appears to have led to significant structural improvements in U.S. labor productivity and energy efficiency, allowing firms to offset higher energy and non-energy costs. But perhaps more important, since the Great Inflation of the 1970s and early 1980s, the Federal Reserve has implemented, and largely achieved, a policy designed to maintain price stability. As long as these factors persist, current forecasts calling for continued solid growth and moderate inflation may turn out to be right for a change.

Endnotes

- The supply of oil tends to be fixed in the short term, since it takes time to explore for new reserves or tap proven reserves. In economist lingo, the supply curve for oil is inelastic in the short run. Accordingly, an increase or decrease in the demand for oil will engender a disproportionate response on the price side.[back to text]

- Real GDP grew at about a 4.25 percent annual rate through the first three quarters of 1998; CPI inflation averaged 1.5 percent during the same period.. [back to text]

- Blue Chip Economic Indicators dated December 10, 1998, and January 10, 1999, respectively. [back to text]

- The Experimental Recession Index developed by Harvard Professor James Stock and Princeton University Professor Mark Watson, which attempts to predict turning points in the business expansion, showed that as of November 2000, the probability of the U.S. economy being in recession in May 2001 was only 7 percent. The report can be obtained at http://ksghome.harvard.edu/~.JStock.Academic.Ksg/xri/INDEX.HTM. [back to text]

- In recent years, the "average" forecaster has tended to underpredict the strength of U.S. economic activity (real GDP growth and unemployment rates) and overpredict the run-up in inflation. See Kliesen (2000). [back to text]

- International Monetary Fund (2000), pp. 48-52. [back to text]

- For example, realized capital gains have boosted consumer incomes and thus spending (the wealth effect); in addition, increases in realized capital gains have caused individual tax payments to the Treasury to skyrocket, helping to produce record federal budget surpluses. [back to text]

- U.S. energy use per unit of real GDP declined at annual rates of 2.7 percent from 1973 to 1983; 1.4 percent a year from 1983 to 1995, and 2.6 percent a year from 1995 to 1999. [back to text]

- See articles by Rasche and Tatom (1977, 1981) and Hamilton (1983). [back to text]

- This is a standard aggregate production function framework which follows a Cobb-Douglas model. See Auerbach and Kotlikoff (1998) for a textbook treatment. [back to text]

References

Auerbach, Alan J., and Laurence J. Kotlikoff. Macroeconomics: An Integrated Approach (Cambridge, Mass.: The MIT Press, 1998).

Blue Chip Economic Indicators. Aspen Publishers, Inc.

Hamilton, James D. "Oil and the Macroeconomy Since World War II," Journal of Political Economy (April 1983), pp. 228-48.

International Monetary Fund. World Economic Outlook, Washington, D.C., October 2000.

Kliesen, Kevin L. "The Economic Out-look for 2000: Bulls on Parade?" Federal Reserve Bank of St. Louis National Economic Trends (January 2000).

Rasche, Robert H., and John A. Tatom. "The Effects of the New Energy Regime on Economic Capacity, Production and Prices," Review, Federal Reserve Bank of St. Louis (May 1977), pp. 2-12.

____________. "Energy Price Shocks, Aggregate Supply, and Monetary Policy: The Theory and the International Evidence," Supply Shocks, Incentives and National Wealth, Carnegie-Rochester Conference Series on Public Policy, volume 14, Karl Brunner and Allan H. Meltzer, eds., Amsterdam: North-Holland (Spring 1981), pp. 9-94.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us