Leaning Against the Wind: Does the Fed Engage in Countercyclical Monetary Policy?

Economists have carried on a longstanding debate about the role of monetary policy over the business cycle—the alternating sequence of expansion and contraction in economic activity.

The prevailing view seems to be that the Federal Reserve, as the nation's monetary authority, pursues an activist, countercyclical monetary policy. In economic parlance, this is referred to as "leaning against the wind." But is this perception real or imagined? Moreover, is it appropriate for the Federal Reserve to engage in countercyclical monetary policy? If so, how easy is it in practice to pursue such a policy?

Countercyclical monetary policy can be thought of in the following manner: When the Fed perceives economic activity to be waning, it attempts to boost output and employment by increasing the supply of money, thereby putting downward pressure on interest rates and stimulating growth in such interest-sensitive sectors as housing and consumer durables. When the Fed perceives inflation to be accelerating, it does just the opposite—it restricts the growth of money, which tends to put upward pressure on interest rates and ease inflationary pressures. Thus, by altering the money supply, the Fed attempts to sufficiently influence interest rates to affect overall economic activity and inflation.

This policy prescription, of course, is overly simplistic and subject to numerous caveats. For instance, should the Fed concern itself with short-term disturbances to output, employment or changes to the price level? Many economists believe that by attempting to offset these short-term disturbances—instead of adhering to the Fed's traditional goal of long-run price stability ("wringing inflation out of the economy over time")—the Fed merely adds to the instability of an already uncertain situation.

The Fed is beset with several constraints, each of which presents substantial problems in the successful implementation of countercyclical monetary policy. To begin with, if it attempts to stimulate economic growth by boosting the money supply for too long, the Fed runs the risk of igniting inflationary pressures. Accordingly, it will face the specter of having to offset these pressures in the future. Most economists agree that inflation is primarily a monetary phenomenon over time. Statistical evidence demonstrates that those countries with relatively low money growth rates in the long run have relatively low rates of inflation.

Second, the Fed's ability to explicitly influence market-determined interest rates is tenuous at best. While the Fed has some influence over very short-term rates like the federal funds rate (the interest rate banks charge each other for loans, typically made on an overnight basis), it has far less control over important long-term interest rates like those on corporate bonds or 30-year Treasury bonds. One reason for this is that long-term rates—those that crucially affect capital formation and economic output—contain an expected inflation component. If the Fed attempts to lower short-term interest rates too aggressively and subsequently ignites inflation, long-term rates could actually rise.

Third, it is not altogether clear that the Fed can reliably influence output and employment over the short term, say, within a few quarters or so. While changes in the money supply may show up within a very short period of time in the financial markets, it takes several quarters—in some cases, years—before this monetary stimulus begins to affect output, employ mentor prices. Failure to recognize these long and variable lags can create much distortion. For example, on several occasions since December 1990, the Fed has seemingly reduced the fed funds rate target on the same day that a weak employment report was released. The distortion from these policy actions is magnified in two ways: (1) it perpetuates the premise that the Fed can control employment, leading to (2) the view that the Fed should attach more weight to short-term disturbances than to long-term price stability.

A final constraint, which follows directly from the previous one, is that these lags make economic forecasting a risky proposition. As a result, the Fed formulates policy based on notoriously unreliable short-term economic forecasts. Neither Fed economists nor private forecasters have an exemplary record when it comes to anticipating recessions or expansions. For example, the economy was about four months into the latest recession before economists reached a consensus that a recession had even begun. As a result, policy actions that may have helped counteract some of the recession's more negative aspects were delayed or rendered ineffective.

How these constraints affect the implementation of a countercyclical monetary policy is difficult to ascertain. Economists cannot determine, for example, whether Fed policy actions prevented the onset of recessions that never came to pass. Nor can we accurately determine how much lower or higher inflation would have been in the absence of certain policies. Economists can, however, effectively gauge Fed policy over previous business cycles, by examining those monetary aggregates over which the Fed has a measurable degree of control.

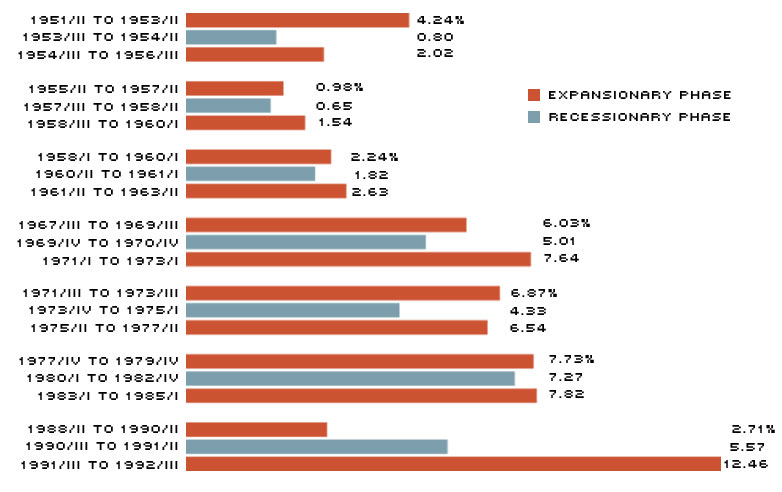

Conventional wisdom is that the Fed routinely pursues countercyclical monetary policy. A casual examination of the evidence, however, reveals quite the opposite—money typically grows faster during economic expansions than it does during economic contractions (see below). This pattern has been pointed out by many economists, and is too persistent to be shrugged off. Is this perverse behavior on the part of the Fed? Or simply a demonstration of how difficult it is to conduct an activist countercyclical policy? Many economists, believing in the latter, have advanced the argument that a consistent monetary policy that targets the supply of money, rather than the federal funds rate, can avoid some of these pratfalls. A countercyclical policy that strives to lean against the wind, perhaps wise in theory, is akin in practice to whistling past the graveyard.

M1 Growth Over the Business Cycle

NOTE: The 1980 and 1981-82 recessions are grouped together in the chart to prevent overlapping. This chart is adapted from Alan H. Meltzer, The Fed at Seventy-Five," In Monetery Policy on the 75th Anniversary of the Federal Reserve System, Proceedings of the Fourteenth Annual Economic Policy Conference of the Federal Reserve Bank of St. Louis, Michael T. Belongia, ed. (Kluwer, 1991).

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us