The Recovery Act of 2009 vs. FDR's New Deal: Which Was Bigger?

The American Recovery and Reinvestment Act of 2009 has been called the federal government’s largest economic recovery plan ever. But was it really?

The Recovery Act was one of the first pieces of legislation passed during the presidency of Barack Obama.1 Besides being a massive stimulus program on the heels of the Great Recession (2007-09), the act provided fodder for the debate on when and how the government should intervene in the economy.

After all was said and done, the Recovery Act’s total cost was $840 billion. Michael Grabell, an author of a history of the act, called it “the biggest economic recovery plan in history.” Similar statements have been made in several media outlets.2 My focus will be on whether or not the act really holds this title. I will do this by comparing it to another massive fiscal stimulus in U.S. history, President Franklin D. Roosevelt's New Deal.

Multiple Ways to Compare

The New Deal began in 1933, when the federal government introduced an “alphabet soup” of programs meant to give economic relief during the Great Depression. For example, the Works Progress Administration (WPA) was created as a federal agency that hired millions of unemployed workers to carry out civil projects, such as constructing public buildings and roads. The Agricultural Adjustment Administration (AAA) oversaw the reduction in farm production by paying farmers to leave parts of their croplands fallow and to kill off a fraction of their livestock.

According to a 2015 study by economists Price Fishback and Valentina Kachanovskaya, total federal spending on New Deal programs was $41.7 billion at that time. Translated into dollars at the time of the Recovery Act's passage, New Deal spending equaled $653 billion. Without any other adjustment, one would conclude that the Recovery Act was the more expensive of the two stimulus programs, which also would make it the most expensive in U.S. history.

However, a lot has happened in the U.S. between the 1930s and the 2000s besides inflation that might lead one to make other adjustments to the numbers. For one thing, the U.S. population more than doubled. On a per capita basis in 2009-adjusted dollars, the Recovery Act cost $2,738, while the New Deal programs cost $5,231. Accordingly, one could reach the conclusion that the Recovery Act cost less than the New Deal but that the two were of a similar order of magnitude.

Let's not stop there. Even after accounting for population growth and inflation, the U.S. economy has grown because of productivity. With this in mind, one could compare the two stimulus programs in terms of the size of the economy when each was enacted. By this measure, the cost of the Recovery Act was equal to 5.7 percent of the nation’s 2008 output. On the other hand, the cost of the New Deal, based on the Fishback-Kachanovskaya numbers, was 40 percent of the nation’s 1929 output. A key reason that the New Deal programs cost substantially more than the Recovery Act is that the former continued for a longer time. Most of the Recovery Act spending took place over three years, but the New Deal spending stretched over seven years, Fishback and Kachanovskaya reported.

Of course, factors besides these programs affected fiscal policy during each of the two time periods. First, the tax liabilities of households and businesses changed because their incomes were falling. Second, other transfer programs (such as unemployment insurance and food stamps), particularly during the Recovery Act period, were at work putting resources into the economy. These are known as “automatic stabilizers.” There were other programs during the Recovery Act period, such as the Education Jobs Fund and the Car Allowance Rebate System program (CARS, also known as Cash for Clunkers).

As a Share of GNP

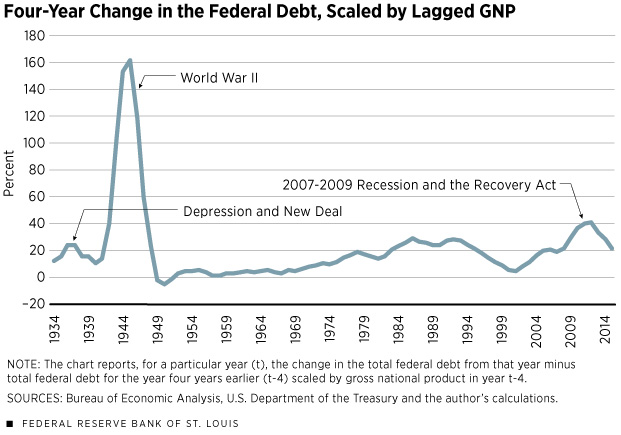

One more broad way to measure the relative size of the two fiscal stimuli is to compare their effect on the federal debt as a fraction of gross national product (GNP). A larger increase in the debt may be interpreted as greater fiscal easing. The cost of programs such as CARS is reflected by an increase in the federal debt.

To get at this measure, I first calculated the increase in the federal debt between 1931 and 1939 as a fraction of GNP in 1931. This equaled 30.3 percent. Then, I calculated the increase in the federal debt between 2008 and 2011 as a fraction of GNP in 2008. This equaled 32 percent. By this broader measure, the two interventions were of a relatively similar size, with the response to the 2007-09 recession being slightly larger. The figure shows the four-year change in the federal debt scaled by GNP across time.

Beyond Fiscal Stimuli

Finally, there are aspects of countercyclical government intervention that sometimes go beyond traditional fiscal (or monetary) policy. These can be difficult to measure with a particular dollar value. The New Deal famously introduced industrial and labor policies that influenced the operation of the private sector, even though the policies did not increase government purchases or change taxes.3 For example, the National Industrial Recovery Act authorized the regulation of industry by the president as a potential way to stimulate the economy by raising prices. Also, the Wagner Act established the National Labor Relations Board, which increased the power of labor unions. In contrast, the Recovery Act consisted almost entirely of tax relief, transfers and government spending and did not venture into industrial and labor policy areas.

Bill Dupor is an economist at the Federal Reserve Bank of St. Louis. For more on his work, see https://research.stlouisfed.org/econ/dupor. Research assistance was provided by Rodrigo Guerrero, a research associate at the Bank.

Endnotes

- A substantial amount of research has been done on the short-term economic impact of the act. For example, Conley and Dupor (2013) and Dupor and Mehkari (2016) examined the act’s job-market effects. Dupor and Li (2015), in part, studied the effects of the Recovery Act on inflation. Dupor and McCrory (2017) examined the extent to which Recovery Act spending spilled over across geographic regions. [back to text]

- See, for example, Bennett and Weise, Chapman and Klein. [back to text]

- See, for example, Cole and Ohanian. [back to text]

References

Bennett, Drake; and Weise, Karen. “Unemployment and the Stimulus: A Timeline.” Bloomberg, Oct. 11, 2012. See www.bloomberg.com/news/articles/2012-10-11/unemployment-and-the-stimulus-a-timeline.

Chapman, Steve. “The Failure of Obama’s Stimulus.” Reason.com, Sept. 23, 2010. See www.reason.com/archives/2010/09/23/the-failure-of-obamas-stimulus.

Cole, Harold L.; and Ohanian, Lee E. “New Deal Policies and the Persistence of the Great Depression: A General Equilibrium Analysis.” Journal of Political Economy, Vol. 112, No. 4, 2004, pp. 779-816.

Conley, Timothy; and Dupor, Bill. “The American Recovery and Reinvestment Act: Solely a Government Jobs Program?” Journal of Monetary Economics, Vol. 60, No. 5, 2013, pp. 535-49.

Dupor, Bill; and Li, Rong. “The Expected Inflation Channel of Government Spending in the Postwar U.S.” European Economic Review, Vol. 74, 2015, pp. 36-56.

Dupor, Bill; and McCrory, Peter. “A Cup Runneth Over: Fiscal Policy Spillovers from the 2009 Recovery Act.” The Economic Journal, forthcoming.

Dupor, Bill; and Mehkari, M. Saif. “The 2009 Recovery Act: Stimulus at the Extensive and Intensive Labor Margins.” European Economic Review, Vol. 85, 2016, pp. 208-28.

Fishback, Price; and Kachanovskaya, Valentina. “The Multiplier for Federal Spending in the States during the Great Depression.” The Journal of Economic History, Vol. 75, No. 1, 2015, pp. 125-62.

Grabell, Michael. “Money Well Spent? The Truth behind the Trillion-Dollar Stimulus, the Biggest Economic Recovery Plan in History.” New York: Public Affairs Books, 2012.

Klein, Ezra. “Could This Time Have Been Different?” The Washington Post, Oct. 8, 2011. See www.washingtonpost.com/blogs/ezra-klein/post/could-this-time-have-been-different/2011/08/25/gIQAiJo0VL_blog.html.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us