A Look at Corporate Inversions, Inside and Out

A corporate inversion, as defined by the U.S. Treasury, occurs when a U.S.-based multinational corporation restructures itself so that the U.S. parent is replaced by a foreign parent and the original U.S. company becomes a subsidiary of the foreign parent.

Inversions are undertaken to reduce taxes. This permissible strategy changes the tax jurisdiction and, therefore, the tax rate to that of the new foreign parent. The tax benefit can be substantial because the U.S. corporate tax rate is one of the highest in the world, with a statutory rate of 35 percent. The transaction is often just on paper; frequently, the U.S.-based operations do not relocate, although investment in the new host country sometimes occurs after the inversion.

Critics of inversions view the strategy as a gimmick that takes unfair advantage of unintended loopholes in the U.S. corporate tax system, a system that is worldwide in scope compared with a territorial system used by most of the rest of the world. In a worldwide system, corporate earnings are taxed wherever they occur; in a territorial system, corporations are taxed just on the earnings generated within the home country’s borders.1 This mismatch of both unfavorable rates and two different taxation systems creates incentives for U.S. multinationals to sharply reduce their tax bills.2

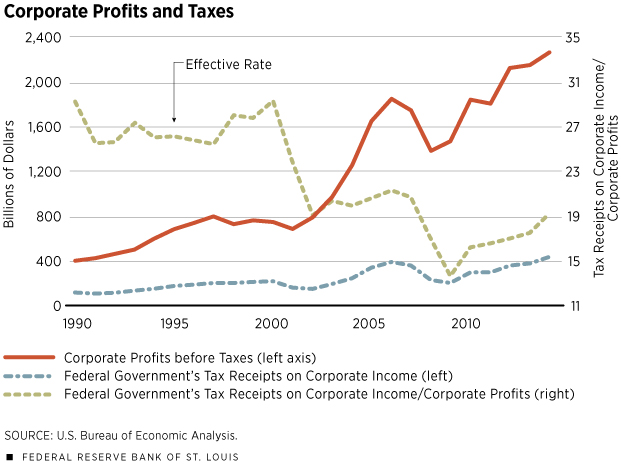

Inversions are one of a number of strategies U.S. corporations use to reduce taxes. As a result, the tax rate U.S. corporations actually pay (the effective rate) is far less than the statutory rate, and that effective tax rate has been declining for most of this century despite higher corporate profits. (See Figure 1.) Absent reform, that trend is expected to continue: The Congressional Budget Office has estimated that corporate income tax receipts will decline from 2.3 percent of gross domestic product (GDP) in fiscal year 2016 to 1.8 percent of GDP in fiscal year 2025—partly due to inversions.3Other countries have been cutting their statutory tax rates, while the U.S. rate has remained at 35 percent since 1986.4 Inversions appear to be a symptom of a larger underlying problem, namely a U.S. corporate tax code that many say is sorely in need of modernization.

Lessons from History

Past attempts by lawmakers to curtail inversions were successful in making them more difficult and expensive to execute. However, companies found ways around the rules.5 Because the monetary incentive is so great, attempts to circumvent rules that are meant to discourage or prohibit inversions will likely continue, even though guidance on inversions issued by the Treasury Department in April 2016 caused U.S. pharmaceutical giant Pfizer Inc. to call off its intended $160 billion merger and planned inversion with smaller Irish-based Allergan PLC.6

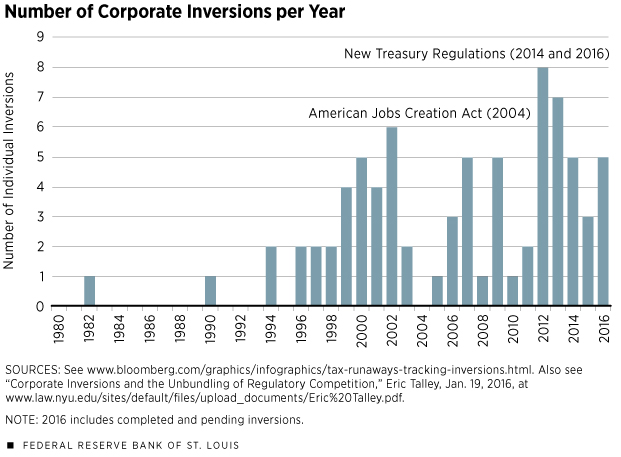

The first corporate inversion occurred in 1982. The activity became more common in the late 1990s, with tax havens like Bermuda and the Cayman Islands being favored destinations because they have zero corporate tax rates. (See Figure 2.) Well-known companies Tyco International and Fruit of the Loom both underwent inversions during this period.

In 2004, Congress passed the American Jobs Creation Act (AJCA) to stop inversions without impeding legitimate mergers. The AJCA created a section of the Internal Revenue Code (Section 7874) that sought to prevent inversions by continuing to count such corporations as domestic for tax purposes if the original U.S. shareholders still owned at least 80 percent of the revamped firm.7 Firms seeking to invert were also required to have active operations in the country hosting the new headquarters.

Although Section 7874 essentially put a stop to inversions, corporations made adjustments to take advantage of loopholes in the law, and soon a second wave of inversions took place—at least 30 were announced or completed between 2009 and 2014. Several of the companies involved in this second wave had participated in, or were spin-offs from, earlier inversions, thus becoming known as “serial inverters.”

Because of rules enacted with the AJCA, this second wave featured mergers of economic substance, like Burger King’s acquisition of Canadian restaurant chain Tim Hortons and medical technology firm Medtronic’s acquisition of Ireland’s Covidien PLC. Ireland and the United Kingdom have become favored destinations, due in part to the lowering of corporate taxes to attract business. This second group of inversions involved mergers with existing foreign corporations to get around the Substantial Business Activities (SBA) test requirement of the AJCA.8 The SBA test was intended to prevent a relocation that was represented by only a post office address and token operations.

The U.S. Treasury issued regulations in late 2014 and early 2016 aimed at closing loopholes in the 2004 law, as well as taking action against a variety of tax-avoidance transactions known as “hopscotch” loans and “earnings stripping.” Such transactions use related-party debt structured to transfer funds without creating a taxable event.9

The “Lockout Effect"

While the foreign earnings of U.S. multinational companies are subject to both foreign and U.S. corporate taxes, the domestic tax bill does not become due until earnings are repatriated—brought home—to the U.S.10 Despite U.S. multinationals’ being able to get credits on foreign taxes paid so that they can reduce their domestic tax bills, many companies have chosen to leave the money overseas. Analysts estimate that as much as $2.5 trillion of corporate earnings are voluntarily “locked out” of being returned to the U.S. and, thus, are subject to deferred income taxes. The combination of earnings kept overseas and earnings exempt from taxes because of inversions contributes to an effective corporate tax rate that is much lower than the statutory rate.

The AJCA granted a one-time, yearlong tax holiday in 2004 for corporations to repatriate foreign-earned income at a reduced corporate tax rate of 5.25 percent. Some of the largest U.S. corporations, particularly in the pharmaceutical and technology sectors, took advantage and repatriated an estimated $362 billion following the AJCA’s passage.11 Companies had to pledge to use the money for domestic operations and could not use the funds for dividend payments or executive compensation.

Although some policymakers argue that another tax holiday would bring home much-needed revenue that could be used to finance infrastructure and other budget priorities, others argue that the previous holiday did not provide the promised benefits and that another one would only encourage firms to shift more income overseas in preparation for the next holiday. Further, a U.S. Senate investigation following the 2004 tax holiday found that firms that repatriated earnings during that period did pay larger dividends to shareholders, repurchased their own stock and, in a number of cases, cut their U.S. workforces.12

Tax Overhaul to the Rescue?

Corporations seek inversions because of two fundamental features of the U.S. tax code: the differential treatment of income earned at home versus abroad and a high corporate tax rate. While inversions are entirely rational from a corporation’s perspective, they create distortions and inefficiencies that cost the economy at large. Legislation has been used as a stopgap measure to halt inversions, but it has not solved the fundamental problems of the tax code.

Corporate tax reform is one solution often proposed by opponents of inversions. Most proposals would reduce the corporate tax rate while also changing the taxation of foreign earnings. Although lowering the tax rate would certainly make inversions less attractive, U.S. companies would still have an incentive to relocate to any country with a still lower tax rate. A lowering of the tax rate would simply make it less expensive to repatriate earnings. The benefits of a lower rate would also need to be carefully weighed against the potential consequences for the U.S. economy if it led to a significant overall reduction in tax revenue.

Moving to a territorial system of taxation has also been suggested as a way to halt inversions. A territorial system, however, would increase the incentives to shift U.S. profits overseas to avoid any taxation and could dampen domestic investment by firms seeking to increase after-tax returns.

Tax treaties and international agreements complicate the ability of rule-makers to act, moreover. While one nation may be trying to increase its collection of corporate tax revenue, another may be trying to attract corporate investment and be willing to sacrifice revenue to do so. It’s the international equivalent of U.S. local governments’ using tax increment financing to attract a business or development, which raises concerns of “a race to the bottom” among nations that could lead to significant declines in government revenue collected from corporations. Over time, this would likely lead to additional policy challenges, such as reducing government spending, increasing borrowing or increasing taxes from other sources, such as individual income taxes.

Most important, some firms that merge and execute an inversion have substantial synergies that would justify a merger even without the inversion tax benefits. By stopping inversions, policymakers could obstruct U.S. corporations from pursuing beneficial mergers. If U.S. companies are hobbled competitively by adhering to a restrictive tax regime, they could become takeover targets of foreign acquirers.

Michelle Clark Neely is an economist, and Larry D. Sherrer is a senior examiner, both in the Banking Supervision and Regulation Division at the Federal Reserve Bank of St. Louis.

Endnotes

- In actual practice, the U.S. system is a hybrid, mixing some of the characteristics of a territorial system with those of a worldwide system. Earnings are taxable wherever they occur (worldwide), but taxes are not due until or unless the earnings are brought back, or repatriated, to the U.S. Further, U.S. corporations receive credit for foreign taxes paid to avoid double taxation. [back to text]

- See Duhigg and Kocieniewski for an analysis of Apple’s complex arrangements to minimize its U.S. tax bill. [back to text]

- See Joint Committee on Taxation. [back to text]

- The 1986 Tax Reform Act was signed into law Oct. 22, 1986, by President Ronald Reagan. [back to text]

- See The Economist for a discussion of the futility of stopgap rules that fail to address larger problems within the tax code. [back to text]

- See Murphy. [back to text]

- Under Section 7874, an inverted corporation with 60 percent ownership by shareholders of the former parent faces 10 years of U.S. taxes on gains from the sale of certain assets. See Marian. [back to text]

- See Oosterhuis, as well as Marples and Gravelle. [back to text]

- See U.S. Department of the Treasury. [back to text]

- The 2013 Congressional Budget Office study provides illustrations and examples of repatriation options under different tax-planning scenarios. [back to text]

- See Browning. [back to text]

- See Marr and Huang. [back to text]

References

Browning, Lynnley. “A One-time Tax Break Saved 843 U.S. Corporations $265 billion,” The New York Times, June 24, 2008. See www.nytimes.com/2008/06/24/business/24tax.html.

Congressional Budget Office. “Options for Taxing U.S. Multinational Corporations,” January 2013. See www.cbo.gov/publication/43764.

Duhigg, Charles; and Kocieniewski, David. “How Apple Sidesteps Billions in Taxes.” The New York Times, April 28, 2012. See www.nytimes.com/2012/04/29/business/apples-tax-strategy-aims-at-low-tax-states-and-nations.html.

The Economist. “How to Stop the Inversion Perversion,” July 26, 2014. See www.economist.com/news/leaders/21608751-restricting-companies-moving-abroad-no-substitute-corporate-tax-reform-how-stop.

Government Accountability Office. “Corporate Tax Expenditures: Evaluations of Tax Deferrals and Graduated Tax Rates," September 2013. See www.gao.gov/assets/660/657896.pdf.

Joint Committee on Taxation. “Present Law and Selected Policy Issues in the U.S. Taxation of Cross-Border Income.” Staff report for U.S. Senate Committee on Finance, JCX-51-15, March 16, 2015.

Marian, Omri. “Home-Country Effects of Corporate Inversions.” Washington Law Review, Vol. 90, No. 1, 2015. See www.law.uw.edu/wlr/print-edition/print-edition/vol-90/1/home-country-effects-of-corporate-inversions.

Marples, Donald J.; and Gravelle, Jane G. “Corporate Expatriation, Inversions, and Mergers: Tax Issues.” Congressional Research Service, Report 7-5700, April 27, 2016. See https://fas.org/sgp/crs/misc/R43568.pdf.

Marr, Chuck; and Huang, Chye-Ching. “Repatriation Tax Holiday Would Lose Revenue and Is a Proven Policy Failure.” Center on Budget and Policy Priorities report, June 20, 2014. See www.cbpp.org/research/repatriation-tax-holiday-would-lose-revenue-and-is-a-proven-policy-failure.

Murphy, Tom. “Experts Expect Corporate Tax Inversions to Survive New Rules.” Chicago Tribune, April 7, 2016. See http://www.chicagotribune.com/business/ct-corporate-tax-inversions-new-rules-20160407-story.html.

Oosterhuis, Paul W. “The Inversion Experience in the United States.” ITPF/TPC Conference on Corporate Inversions and Tax Policy, Jan. 23, 2015. See www.brookings.edu/wp-content/uploads/2015/01/OOSTERHUIS_slides.pdf.

U.S. Department of the Treasury. “Fact Sheet: Treasury Actions to Rein in Corporate Tax Inversions.” Sept. 22, 2014. See www.treasury.gov/press-center/press-releases/Pages/jl2645.aspx.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us