Many Americans Still Lack Retirement Savings

KEY TAKEAWAYS

- A growing debate is focused on whether U.S. households have saved enough for retirement.

- The latest Survey of Consumer Finances data show that 35 percent of households don’t participate in a retirement plan.

- Even for households approaching retirement, the problem of underparticipation in retirement plans persists.

As baby boomers age, significant debate has emerged about whether there is a retirement crisis developing in the United States. Some argue that the retirement situation is poor for many Americans, with many approaching retirement age with little or no savings. However, others describe the situation as better than commonly thought, as many retirees report living comfortably.1

This article aims to offer a glimpse into the current state of retirement readiness in the United States. We examine the participation in and usage of the two most common types of financial accounts designed exclusively for retirement savings.

The first type is the employer-sponsored pension plan (ESPP); this includes defined-benefit plans, such as traditional pensions, and defined-contribution plans, such as 401(k) plans. The second is a retirement plan offered independent of the workplace, which includes individual retirement accounts (IRAs) and Keogh accounts.

Overall, our analysis indicates that many households either do not utilize or underutilize the retirement savings plans available to them. We also examine how retirement savings vary with age and discuss alternative ways that nonparticipants may be preparing for retirement.

In our analysis, we utilized data on retirement account participation and account balances from the Survey of Consumer Finances (SCF). Every three years, the survey provides cross-sectional data on U.S. households’ demographic characteristics, incomes, balance sheets and pensions. The Federal Reserve Board, along with the Department of the Treasury, released the SCF data for 2016—the most recent year available—in September 2017. The primary unit of analysis in the SCF is the household, and the survey attempts to capture the distribution of households in the U.S. Thus, the results reported in this article should represent the general state of participation in and usage of retirement accounts in the U.S.

Little or No Retirement Savings

Previous studies documented low participation among households and low account balances for those that do participate. For example, a 2016 study by economist Monique Morrissey used SCF data to show that participation in defined-benefit and defined-contribution plans is quite low, and that many families have little or no retirement savings.

Our findings are generally in line with Morrissey’s. The most recent SCF data show that not all employers offer pension plans to their employees and not everyone who has access chooses to participate. Only 27 percent and 33 percent of households have defined-benefit and defined-contribution plans, respectively, at their current jobs; 8 percent of households have both. In total, about 56 percent of households have an employer-sponsored pension plan associated with their current or previous employment.

One might think that households that do not have access to an ESPP are more likely to utilize an IRA or Keogh account as an alternative option. However, this is not what we see in the data. Roughly 30 percent of households have an IRA or Keogh account. Of households that do not have an ESPP, only 20 percent utilize any IRAs or Keogh accounts, while 38 percent of households that have an ESPP also have at least one IRA or Keogh account. This implies that participating in one type of retirement account increases one’s likelihood of participating in additional retirement accounts.

Overall, 35 percent of U.S. households do not participate in any retirement savings plan.2

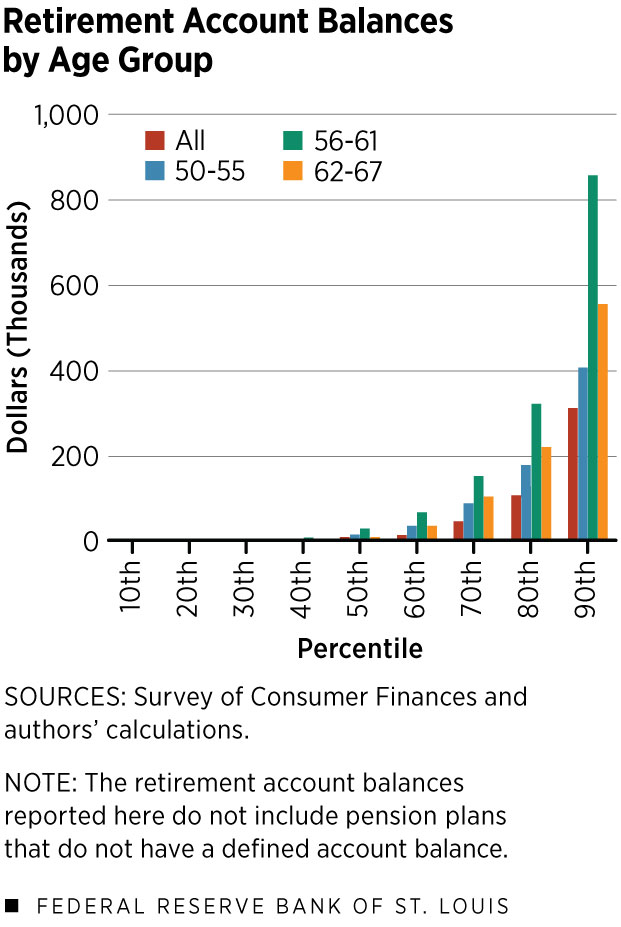

Even among those households that do hold retirement accounts, many of them have low account balances. Figure 1 plots the sum of account balances of all IRAs, Keogh accounts and pension plans by percentile for various age groups.3 The median (50th percentile) household of all ages (the red bar) holds only $1,100 in its retirement account. Even the 70th and 80th percentiles of households have only about $40,000 and $106,000 in their retirement accounts, respectively.

By contrast, the 90th and 95th (not shown in the figure) percentiles of households hold considerable amounts, at about $310,000 and $612,000, respectively. This implies a high degree of inequality in retirement account balances across households.

Intuitively, the balance of a retirement account should increase and peak right before retirement. Thus, it could be useful to exclude younger households from our analysis to avoid downwardly biasing the results. Younger households are likely to be in a stage of saving for expenses, such as a down payment on a house or future education costs for their children. It is reasonable to expect that they might postpone their retirement savings with the intention of catching up later.

To account for this, Figure 1 also plots retirement account balances for nonretired households whose heads are ages 50-55, 56-61, and 62-67. We refer to these households as pre-retirement households throughout the rest of the article.

Participation rate improves very little for pre-retirement households, indicating that age plays only a small role in the decision to participate and that younger households that do not participate may not be very likely to participate even by the time retirement approaches.

Conditional on having a positive retirement account balance, the households with heads ages 56-61 accumulate more savings, but the underparticipation problem persists. The median of this group holds only around $25,000. The balances of the 70th and 80th percentiles improve to about $148,000 and $320,000, respectively. The degree of inequality is more pronounced among this age group: The 90th percentile of households holds around $855,000, while the 95th percentile (not shown in the figure) holds almost $1,470,000.

Fallback Options?

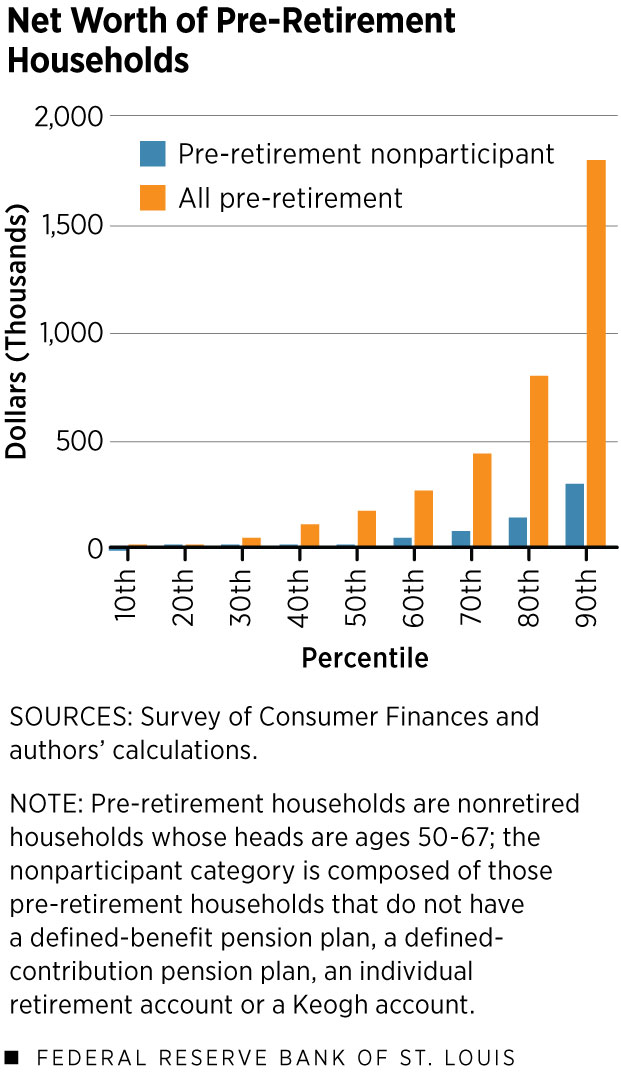

The lack of retirement accounts does not necessarily imply that nonparticipants aren’t saving for retirement. Households could save through other financial assets or nonfinancial assets, such as home equity. However, the net worth (the value of all assets net of total debt) of pre-retirement nonparticipants is typically quite limited.

Figure 2 plots the distribution of net worth among all pre-retirement households and pre-retirement nonparticipant households. The net worth of pre-retirement nonparticipant households is much lower relative to that of all pre-retirement households. Only the pre-retirement nonparticipant households at the upper end of the distribution have sizable net worth, but the numbers are still not very sizable, especially compared to those of all pre-retirement households. The 80th percentile has a net worth of approximately $138,000, and the 90th percentile has a net worth of $293,000. The net worth of the corresponding percentiles for all pre-retirement households is at least five times larger.

However, these pre-retirement households that don’t participate in retirement plans may have some fallback options that fall outside the scope of our analysis. Social Security benefits are the first and most obvious option. In addition, postponing retirement age or taking a part-time job after retirement could alleviate the problem. In fact, the labor force participation rate for seniors (age 65 and above with no disability) has been trending upward for much of the past decade and was at 23 percent in January 2018.4

We also do not take into account the potential inheritance one might get, and financial support or housing assistance from children, relatives and friends could provide some security for those without significant retirement savings.

Still, this article documents that many households either do not utilize or underutilize retirement accounts, such as ESPPs and IRAs. It could be worrisome that, for many American households, the total balances of their retirement accounts may not be sufficient to ensure a solid life in retirement.

Endnotes

- See Moeller and Henricks for recent reports on the current retirement crisis. [back to text]

- We define nonparticipants to be households that do not participate in a defined-benefit pension plan, a defined-contribution pension plan, an IRA or a Keogh account. [back to text]

- The retirement account balance reported here does not include defined-benefit pension plans that do not have a defined account balance. Therefore, one should interpret this measure as a lower bound. [back to text]

- For the specific data, see https://fred.stlouisfed.org/series/LNU01375379. [back to text]

References

Henricks, Mark. Reports of a Retirement Crisis Are Off the Mark: Think Tank. CNBC, July 5, 2017. See www.cnbc.com/2017/07/05/reports-of-a-us-retirement-crisis-are-off-the-mark-think-tank-study.html.

Moeller, Philip. 5 Reasons the Retirement Crisis Is Getting Worse for Average Americans. Money, March 22, 2016. See http://time.com/money/4266111/retirement-crisis-worse-average-americans/.

Morrissey, Monique. The State of American Retirement: How 401(k)s Have Failed Most American Workers. Economic Policy Institute, March 3, 2016. See www.epi.org/publication/retirement-in-america/.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us