How Dangerous Is the U.S. Current Account Deficit?

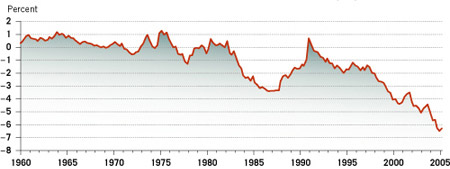

In recent years, the U.S. external deficit has attracted considerable attention from academics, policymakers and the media. One manifestation of recent trends that has raised concerns is a growing trade deficit—the difference between U.S. exports and imports of goods and services. More generally, it is useful to consider the broader concept of the current account, which includes earnings on investments, as well as trade in goods and services. As shown in the figure below, the U.S. current account deficit has been increasing as a percentage of gross domestic product (GDP) since the early 1990s, with the present deficit exceeding 6 percent..1

When a country runs a current account deficit, its purchases of goods and services from abroad exceed its sales of goods and services to foreign buyers. At the same time, the country is necessarily selling assets to foreigners, net of its purchases of assets abroad, in an amount equal to the current account deficit. Consequently, as current account deficits have accumulated over time, the net international investment position of the United States—the difference between U.S.-owned assets abroad and foreign-owned assets in the United States—has also grown ever larger. In light of these trends, a fundamental question is: How dangerous is the current account deficit?

As a practical matter, the U.S. net international investment position cannot become ever more negative as a percentage of GDP. In fact, economic theory suggests that it's likely that today's current account deficits will need to be trimmed or reversed over the long run. The question is not whether the U.S. current account deficit will narrow in the future but whether the inevitable adjustment is likely to be painful and disruptive of economic growth and stability—a "hard landing" precipitated by a dramatic decline in the foreign exchange value of the dollar as investors shun dollar-denominated assets.

Provided that U.S. monetary and fiscal authorities maintain sound policies, the hard-landing scenario seems unlikely. The necessary current account adjustment can be fairly slow and orderly, and it may not begin for quite some time.2

This outlook is based on a simple observation: For the United States, unlike almost every other country in the world, currency depreciation is inherently self-limiting. The reason for this result, which is discussed more fully later, hinges on the fact that U.S. assets owned by international investors are predominantly denominated in dollars, and a large fraction of U.S. assets abroad are denominated in foreign currencies.

Figure 1

Balance on Current Account as a Percent of GDP

Seasonally Adjusted

SOURCE: U.S. Bureau of Economic Analysis

Recent Trends in the U.S. International Investment Position

In balance-of-payments accounting, the mirror image of the current account is a measure known as the capital and financial account, which measures the international flow of capital assets. A current account deficit is exactly equal to a capital account surplus, up to unavoidable errors and omissions in the data.

It is a common mistake to treat international capital flows as though they are passively responding to what is happening in the current account. The current account deficit, some say, is "financed" by U.S. borrowing abroad. In fact, international investors buy U.S. assets not for the purpose of financing the U.S. current account deficit but because they believe these are sound investments, promising a good combination of safety and return. Moreover, many of these investments have nothing whatsoever to do with borrowing as is commonly understood, but instead involve purchases of land, businesses and common stock in the United States. A careful analysis of the nature of international capital flows is necessary before offering judgments about risks posed by the U.S. external deficit.

As trade and commerce around the world have grown increasingly integrated—the process often referred to as globalization—growth of cross-border financial flows has become particularly prominent. From 1990 through 2004, foreign ownership of U.S. assets increased at an average annual rate of nearly 12 percent, while U.S. ownership of foreign assets grew at nearly an 11 percent rate.3 These rates are far in excess of economic growth in the United States or in the rest of the world as a whole.

Prior to 1989, the United States had a positive net international investment position. As a consequence of large capital inflows in the 1990s, however, the United States today has the world's largest negative net international investment position. By the end of 2004, foreigners owned more than $12.5 trillion of U.S. assets, based on market values, while U.S.-owned assets abroad reached a level of just under $10 trillion. The difference of $2.5 trillion amounted to more than 20 percent of U.S. GDP.

In today's world, with electronic funds transfers, financial derivatives and largely unrestricted capital flows, investors have a global marketplace in which to seek profitable returns and to diversify risk. In such an environment, aggregate patterns of international trade may be the byproduct of a process through which financial resources are seeking their most efficient allocations in a worldwide capital market. Instead of thinking that capital flows are financing the current account deficit, it may well be that the trade deficit is driven by capital flows: Capital inflows keep the dollar stronger than it otherwise would be, tending to boost imports and suppress exports, thus leading to a current account deficit.

While the conclusion that the capital account is driving the current account is surely an overstatement, it is worth emphasizing that capital flows are a highly dynamic feature of the world economy, driven by a number of economic forces. The "home bias" of investors, which has led them to invest in their home countries rather than seek optimal international diversification, has been diminishing; investors everywhere are increasingly investing outside their home countries. Countries with rapidly aging populations, especially Japan and in Western Europe, may be saving and investing in the United States against the day when their populations will be drawing down assets to support retired citizens. Capital flows to the United States have also been encouraged by the faster pace of U.S. growth relative to that of most high-income countries.

Capital inflows may also reflect the low saving rate in the United States. However, the U.S. saving rate should not be viewed in isolation: Ben Bernanke, the new chairman of the Federal Reserve, has persuasively argued that an unusually high level of worldwide savings relative to investment opportunities has resulted in downward pressure on world interest rates.4 Investors have brought abundant capital to the United States because the profitability and security of U.S. investment opportunities make the United States something of an oasis of prosperity and stability.

In general, we should think of capital flows as the equilibrium outcome of investors worldwide seeking to acquire portfolios that balance risk and return through diversification. The fundamental economic determinants of capital flows, and therefore the capital flows themselves, are unlikely to change quickly and massively. When we bear this perspective in mind, prospects for a painful current account adjustment in the future seem less likely.

U.S. Role in International Capital Markets

Another factor to consider is the central role of the United States in international financial markets. U.S. financial markets are among the most highly developed in the world, offering efficiency, transparency and liquidity. The U.S. dollar serves as both a medium of exchange and a unit of account in many international transactions. These factors make dollar-denominated claims attractive assets in any international portfolio. No capital market in the world has a combination of strengths superior to that of the United States. Our advantages include the promise of a good return, safety, secure political institutions, liquidity and an enormous depth of financial expertise.

For some purposes, it is useful to think of U.S. financial markets as serving as a world financial intermediary. Just as a bank channels the savings of many individuals toward productive investments, U.S. financial markets play a similar role for many investors from around the world. In the process, individuals, companies and governments accumulate dollar-denominated assets to serve as a vehicle for facilitating transactions and storing liquid wealth safely.

A bank earns its return on capital by paying a lower interest rate to depositors than it earns on its assets. Similarly, the United States earns a higher return on its investments abroad than foreigners do on their investments in the United States. Despite the fact that the U.S. net international investment position at the end of 2004 was −$2.5 trillion, U.S. net income in 2004 on its investments abroad slightly exceeded income payments on foreign-owned assets in the United States.

How can the United States earn a higher return on its assets abroad than foreigners earn on their assets in the United States? Consider currency, which pays a zero return. Over half of the total amount of U.S. currency outstanding is circulating abroad. Another factor is that much of the foreign holding of U.S. assets is in the form of Treasury bills and other debt instruments, while U.S. residents hold a much larger share of their foreign assets in the form of equities, thus earning an equity premium.

More generally, many private and governmental investors abroad rely on the U.S. capital market as the best place to invest in extremely safe and highly liquid securities. The United States as a whole earns a return from providing these safe and liquid investments to the world. The desire of foreigners to hold U.S. Treasury securities is a testament to the confidence that the world has in the safety and soundness of our financial system.

How Dangerous Is the U.S. Current Account Deficit?

In light of these considerations, let us return to the question: How dangerous is the U.S. current account deficit? The first thing to note is that many of the economic forces driving capital flows are very long-term. Portfolio reallocations occur as home bias declines, but over years rather than quarters. Firms build operations in other countries based on plans extending many years into the future. Demographic developments unfold over decades. What may appear to be an imbalance from a short-run perspective may make perfect sense over a long-term horizon.

To the extent that adjustment of the current account will involve changes in the foreign exchange value of the dollar, it is quite likely that such changes will take place over time in orderly markets. There is no inherent reason that such changes would lead to a financial market crisis; as a stable, diversified and growing economy, the United States is not likely to suffer from a sudden lack of confidence by investors so long as it maintains sound economic policies.

It is sometimes said that the United States has become a "net debtor" nation, increasing the risk that currency depreciation might lead to financial crisis. Indeed, with a current account deficit amounting to 6 percent of GDP and a negative net international investment position over 20 percent of GDP, some have drawn comparisons with Argentina, Brazil, Mexico and other countries that at times have experienced severe balance-of-payments crises.

The word "debtor" is extremely misleading in this context, for the U.S. assets owned by foreigners include equities and physical capital located in the United States, in addition to bonds issued by U.S. entities. Moreover, the part of the U.S. international financial position that is debt—bonds and other fixed claims, such as bank loans—is predominantly denominated in dollars. In fact, about 95 percent of international claims on the United States are denominated in dollars. A country with most of its debt denominated in its own currency is in a very different situation from one whose debt is denominated in other currencies. The familiar crises experienced by several Asian countries in 1997-98, by Mexico on several occasions and by numerous other countries have all involved situations in which the affected countries have had large external debts denominated in foreign currencies.

In these previous crises, the foreign denomination of domestic debt had destabilizing consequences. Consider what typically happens to a country suffering a balance-of-payments crisis. As the foreign exchange value of its currency depreciates, the value of its foreign liabilities—in terms of domestic purchasing power—increases, as does the burden of servicing its international debt. Recognizing this, international investors respond by paring back their positions further, engendering even greater currency depreciation. Hence, the combination of foreign-denominated debt and a depreciating currency has proved to be a vicious circle—compounding and accelerating a crisis.

The U.S. situation is completely different. To the extent that the foreign exchange value of the dollar declines, the effect on the values of U.S. and foreign asset holdings works not as an accelerator of crisis, but as part of a self-correcting mechanism. Dollar-denominated U.S. liabilities remain unchanged in domestic value, which means that debt service in dollars and relative to the size of the U.S. economy does not change. Moreover, holdings of U.S. investors abroad, about two-thirds of which are denominated in foreign currencies, appreciate in dollar terms. The composition of the U.S. international investment account, therefore, contributes to stability rather than to instability.

The significant quantitative importance of exchange rate changes on the U.S. net international investment position can be illustrated by examining specific periods in which the dollar appreciated or depreciated. Consider the years 2002-04, during which the Fed's trade-weighted exchange rate index of major currencies depreciated by nearly 27 percent.5 Associated with the current account deficits during this period were financial flows into the United States totaling $1.6 trillion. However, because foreign claims on U.S. assets are denominated in dollars to a far greater extent than are U.S. claims on foreign assets, the depreciation increased the dollar value of U.S. assets abroad relative to foreign assets in the United States. As shown in the table below, the total valuation impact stemming from exchange rate changes was $919 billion, which was 57 percent of the net financial flows. For this three-year period, the U.S. net international investment position decreased by $202.8 billion, but absent the exchange rate adjustment, the position would have decreased by more than $1.1 trillion.

Now consider the years 1999-2001 to illustrate the impact of an appreciating dollar. During this period, the Fed's trade-weighted exchange rate index of major currencies showed a dollar appreciation of nearly 15 percent. Net financial flows into the United States totaled $1.1 trillion. Meanwhile, the total valuation impact of the appreciating dollar was a negative $548.2 billion, which is nearly half the size of the net financial flows. For this three-year period, the U.S. net international investment position decreased by $1.3 trillion. Absent the exchange rate adjustment, the decrease would have been $684.4 billion. However, the negative international investment position did not threaten to cause dollar depreciation; instead, causation went the other way, as dollar appreciation caused a significant increase in the negative net investment position.

Figure 2

| YEAR | POSITION BEGINING | CHANGES IN POSITION | POSITION ENDING | ||||

|---|---|---|---|---|---|---|---|

| Attributal to | Total< (a+b+c+d) | ||||||

| Financial flows (a) | Valuation adjustments | ||||||

| Price changes (b) | Exchange-rate changes (c) | Other changes (d) | |||||

| 1999 | −1,070,769 | −236,148 | 329,672 | −125,970 | 65,778 | 33,332 | −1,037,437 |

| 2000 | −1,037,437 | −486,373 | 133,716 | −270,594 | 79,681 | −543,570 | −1,581,007 |

| 2001 | −1,581,007 | −400,243 | −224,184 | −151,685 | 17,671 | −758,441 | −2,339,448 |

| 2002 | −2,339,448 | −500,316 | −59,582 | 231,247 | 212,985 | −115,666 | −2,455,114 |

| 2003 | −2,455,114 | −560,646 | −1,716 | 415,507 | 229,599 | 82,744 | −2,372,370 |

| 2004 | −2,372,370 | −584,597 | 146,514 | 272,278 | −4,070 | −169,875 | −2,542,245 |

| SOURCE: U.S. Bureau of Economic Analysis | |||||||

The effects of changes in the foreign exchange value of the dollar on the U.S. net international investment position serve to stabilize the international sector of the U.S. economy. Clearly, valuation changes play a significant role in the net change in financial position that is measured in the capital account.

Other industrialized economies have incurred much larger external obligations as a percent of GDP without precipitating crises. For example, Australia's negative net investment position reached 60 percent of GDP in the mid-1990s, Ireland's exceeded 70 percent in the 1980s and New Zealand's hit nearly 90 percent of GDP in the late 1990s. Notably, these economies have recently been among the most successful—in terms of economic growth—in the industrialized world. The combination of rising external obligations and prospects for robust growth is entirely consistent: Capital flows toward countries that can make productive use of it.

A recent study by economists at the Federal Reserve Board of Governors buttresses this view.6 The authors of the study systematically examined examples of developed industrial nations that have experienced current account reversals. The authors found that such reversals have typically been benign: Among those countries that experienced the largest declines in growth during the adjustment period, cyclical considerations appeared to be an important factor. Moreover, these cases were generally not associated with significant exchange rate depreciations. Among those cases where countries weathered the adjustment while experiencing increasing economic growth, exchange rate adjustments were an important factor in reducing current account deficits—primarily by raising export growth rather than lowering imports. In these cases, the exchange rate depreciation evidently played a role in buffering those economies against adverse growth consequences.

These findings provide little evidence to support a hard-landing scenario characterized by disorderly foreign exchange markets. To be sure, no country can permanently incur rising levels of net external obligations relative to GDP. If sustained indefinitely, service payments on ever-increasing obligations would ultimately exceed national income. Long before that situation of literal insolvency occurred, however, market forces would drive changes in exchange rates, interest rate differentials and relative growth rates in such a way to move the economy toward a sustainable path. Nevertheless, such adjustments need not be sudden, large or disruptive.

The international capital markets view suggests that the United States is more like those countries that have experienced high levels of debt without obvious ill effects than those that have suffered crises. Moreover, the U.S. case is unique in a number of respects. The central role of U.S. financial markets—and of the dollar—in the world economy suggests that capital account surpluses and, therefore, current account deficits are being driven primarily by foreign demand for U.S. assets rather than by any structural imbalance in the U.S. economy itself.

Concluding Comments

The international financial markets' view highlights the dynamic role of international capital adjustments as investors exploit the opportunities of globalized financial markets. Because the technological progress and capital-market liberalizations that have driven this process have evolved over time, the process has been protracted. Ultimately, however, when portfolio adjustments have optimally exploited new diversification opportunities, and as growth abroad rises, the net international investment position of the United States will stabilize. So also, over time, will the current account deficit decline to sustainable levels.

If this view is correct, the forces driving the U.S. capital account represent a persistent, but ultimately temporary, process that might result in a higher negative level of net claims without necessarily posing any threat to the long-run sustainability of the U.S. current account. Nor will the transition to a sustainable long-run path necessarily require wrenching adjustments in domestic or international markets or in exchange rates.

Endnotes

- In a growing economy, a current account deficit that is increasing at the same rate as the overall economy implies an unchanging burden of indebtedness. It can, therefore, be misleading to cite current account deficits in dollar terms—it is more appropriate to express the size of the deficit in terms of a fraction of total economic output. [back to text]

- For an alternative view, see Obstfeld and Rogoff (2005). [back to text]

- Data are from the Bureau of Economic Analysis, as reported in the U.S. International Investment Position tables. Direct investment is measured at market value. [back to text]

- See Bernanke (2005). [back to text]

- A trade-weighted exchange rate index provides a measure of how the U.S. dollar has changed in value relative to a sample of other currencies (e.g., the euro, the yen, the Canadian dollar). The importance of each of the other currencies is weighted to depend on the size of the trade flows between the United States and the other countries used to compute the index. [back to text]

- See Croke, Kamin and Leduc (2005). [back to text]

References

Bernanke, Ben S. "The Global Saving Glut and the U.S. Current Account Deficit," presented at the Homer Jones Memorial Lecture, Federal Reserve Bank of St. Louis, St. Louis, Mo., April 14, 2005. See www.federalreserve.gov/boarddocs/speeches/2005/20050414/default.htm.

Croke, Hilary; Kamin, Stephen B.; and Leduc, Sylvain. "Financial Market Developments and Economic Activity during Current Account Adjustments in Industrial Economies." Board of Governors of the Federal Reserve System, International Finance Discussion Papers: No. 827, 2005.

Obstfeld, Maurice; and Rogoff, Kenneth. "Global Current Account Imbalances and Exchange Rate Adjustments." Brookings Papers on Economic Activity, 2005, No. 1, pp. 67-146.

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us