Assessing the Generational Gap in Future Living Standards through Generational Accounting

Among the goals of any policymaker are the design of policies that contribute to sustained increases in living standards over time. These increases depend on many interrelated factors, including inflation, labor force growth, capital formation and productivity gains. In this regard, monetary and fiscal policy can play a key role. For monetary policymakers, this means maintaining an environment of stable prices, which enhances the efficiency of a dynamic economy by fostering confidence among the savers and investors who are crucial to its long-term prosperity. For their part, fiscal policymakers can also help out by having the foresight to implement sound tax and expenditure policies.

To most citizens and many policymakers, achieving a balanced federal budget by 2002 would be considered sound fiscal policy. Many economists, however, would instead ask what policies would be put in place to achieve this fiscal balance. Moreover, how would these policies affect both current and future generations of taxpayers? Because traditional fiscal policy analysis is not readily equipped to handle the complexity of this question, a new method of analysis, called generational accounting, has been developed.

The Incredible Shrinking Deficit

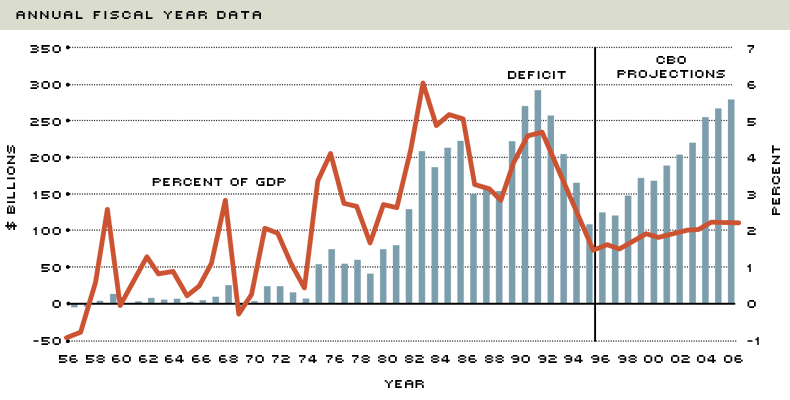

There is no denying, as both the Congressional Budget Office (CBO) and the Office of Management and Budget (OMB) report, that the country's short-term fiscal outlook is as favorable as it has been for quite some time. As shown in Figure 1, the federal budget deficit measured $107.3 billion in fiscal year (FY) 1996—the smallest deficit in dollar terms since 1981, and the smallest as a percent of GDP in 22 years.1 Thus, the political task of crafting a federal budget that achieves balance by FY 2002 is considerably easier than it would have been a few years earlier, when the budget deficit approached $300 billion.

According to the CBO, this improved outlook has occurred for four reasons.2 First, economic growth has been relatively strong since 1991, with real (inflation adjusted) GDP growing by about 2.8 percent per year. This is well above the 2.25 percent to 2.5 percent growth that most economists believe the economy is currently capable of producing on a sustained basis (called "potential output growth"). Second, with the end of the Cold War, there have been continued rollbacks in real defense expenditures: Defense spending as a share of GDP measured 3.6 percent in FY 1996—the lowest ratio since 1948.

Third, the 1990 Budget Enforcement Act instituted a ceiling on the amount that discretionary spending—such as defense, income supports for the poor and transportation—could increase each year (spending caps). The act, which also put in place pay-as-you-go procedures, effectively slowed the growth of real government spending dramatically—in fact, to its smallest share of GDP since before World War II.3 Finally, structural changes in the health care sector have produced significant cost savings, driving medical care inflation rates to their lowest levels since 1965. Going forward, the deficit outlook is expected to worsen somewhat, however, as many of the factors that have contributed to this improved situation begin to play themselves out.

Balancing the budget regularly registers as a high priority with a large percentage of the public and increasingly seems to be one of the top priorities among the nation's policymakers, as well. Despite partisan wrangling over the specifics, both the Clinton administration and Congress have written budgets that—at least on paper—would produce a slight surplus by FY 2002. This effort to balance the budget is being driven in large part by the recognition of most policymakers that, unless current fiscal policy is altered, largely with respect to transfer payments like Social Security, Medicare and Medicaid, the nation faces an impending economic crisis when the baby boom generation—those born between 1946 and 1964—enters its golden years.

A Meaningful Measure?

Will balancing the federal budget by 2002 put the nation on a sustainable path of fiscal rectitude? Moreover, should we even look at the budget deficit as an accurate gauge of the nation's fiscal condition either now or, more important, in the future? To many economists, the answer to both questions is no.

The unified deficit's inadequacies as a measure of future fiscal solvency become clear when certain demographic trends are pushed to the forefront. For example, in 1950, those 65 and older made up 8 percent of the total population; however, by 2010, when the baby boomers begin retiring, this share is expected to reach 13 percent. When most of the boomers have retired by 2030, those 65 and older are projected to comprise 20 percent of the population, with less than three workers paying taxes to support each retiree's Social Security and health care benefits. The problem, which has been recognized for several years, is that the system was originally constructed under the assumption that the number of workers supporting each retiree would be greater today than it actually is. For example, in the 1950s and 1960s six to seven workers supported each retiree, while today the ratio is about 4.5 to 1.

Although the normal retirement age is slated to begin increasing steadily in 2000—eventually reaching 67 in 2022—the demographic challenge confronting current and future fiscal policymakers is still enormous: Proportionately less revenue will accrue from income and payroll taxes, while outlays to retirees in the form of Social Security pensions and health care benefits (Medicare and Medicaid) will continue to rise rapidly. The CBO estimates that with no change in the existing level of retirement benefits, and with all other expenditures merely growing at the rate of inflation (that is, keeping the spending caps in place), total federal outlays are projected to equal nearly half of GDP by 2030, which is more than double the 21 percent they comprised in FY 1996. Moreover, the debt-to-GDP ratio is projected to approach an unprecedented 230 percent by about 2030—nearly five times what it is today. Ratios of this magnitude raise the specter of the government defaulting or the Federal Reserve (effectively) printing money to pay off the debt.

One would be hard-pressed, however, to discern this looking solely at the deficit projections in Figure 1. Even if the deficit could by itself provide some meaningful measure of this impending crisis, however, it would still provide little sense as to what the future economic effects would be on the individuals and firms that will be forced to bear the burden of such adjustments. In a nutshell, this is why proponents of generational accounting (GA) believe that the unified deficit is an inaccurate gauge of the true stance of fiscal policy over time.

GA proponents believe that the budget deficit is nothing more than an arbitrary number. Specifically, they believe the deficit reflects the decisions by policymakers to label certain items receipts and expenditures, instead of attaching different labels to them. For example, it would be just as correct to view receipts from Social Security contributions, which are currently labeled tax revenues, as loans to the government, and transfers,which are currently labeled expenditures, as repayment of the loan's principle with interest.

GA advocates are not alone in claiming that the deficit is an arbitrary measure. The recent debate over the constitutional amendment to balance the budget reinforced this division. Besides those wanting to keep the current definition, many other policymakers wanted the official deficit to exclude outlays for Social Security (which would have increased the official deficit). Still others pushed for the federal government to enact a capital budget like private corporations do, which would have effectively lowered the official deficit. Recognizing this schism, the CBO regularly reports several deficit measures.

Some economists and public policymakers, while accepting the notion that the near-term deficit outlook masks large future fiscal liabilities, nonetheless believe that there is ample time to deal with this problem. GA advocates beg to differ, believing that unless policies are changed quickly and dramatically, the window of opportunity policymakers have to make the changes that will produce the least disruption to economic activity and future living standards will disappear.

The Generational Accounting Approach

According to Figure 1, fairly sound fiscal policy was practiced for much of the postwar period—at least until the early 1970s. During this time, relatively small deficit-to-GDP ratios were the norm, with even a few surpluses. From a GA standpoint, however, this "balanced-budget" era was a period when large fiscal burdens were placed on future generations through expansions in the Medicare and Medicaid programs and increased Social Security benefits. The so-called unified budget deficit could not measure these burdens properly.4

GA advocates stress that this shortcoming is particularly true under the existing pay-as-you-go system, which depends heavily on payroll taxes to bankroll large government transfer programs. For example, a policy that would increase payroll taxes to fully fund expanded Social Security or Medicare benefits would have no effect on the unified deficit, although it would effectively increase the financial burdens of young and future generations, while lessening those of the elderly.

GA—the Basics

Generational accounting is based on the premise that the government must eventually repay, with interest, what it borrows. Or, in the words of economist Milton Friedman, there is no such thing as a free lunch. The basic idea, then, is to compare the fiscal burden of today's newborns with tomorrow's newborns in terms of their lifetime tax liability. If today's newborns end up paying a smaller share of their income in taxes than tomorrow's newborns, there is a generational imbalance that favors those alive today.

Generational accounts are constructed under the requirement known as the government's zero sum constraint, which states that the sum of net tax payments of current and future generations must equal the sum of what the government expects to spend in the future, including the interest payments necessary to service the debt arising from both past deficits and projected future deficits. In other words, the bill for the goods and services provided (or promised) by all levels of government must be paid by someone. If present generations pay less, then future generations must pay more. This does not, however, dictate that the government's debt must be eventually retired; it merely states that servicing it is required to avoid default. In economic terms, this means that the growth of the government's debt cannot forever exceed the growth of GDP. If it did, interest on the debt would eventually exceed the amount of income available to pay for it (see below for more detail on how these generational accounts are constructed).

The GA View of Fiscal Policy

According to a recent study by economists Alan Auerbach, Jagadeesh Gokhale and Laurence Kotlikoff (AGK), fiscal policy is seriously out of generational balance. In their 1995 study, they calculate that males born in 1994 or after (called future generations hereafter for the purposes of this article) faced a net lifetime tax payment of $215,500, which is more than double the $107,000 net tax payment faced by males who were 5 years old in 1993. For females born during the same years, these two tax payments were $131,500 and $64,300, respectively.5 These figures, while illustrative of the difference in tax burdens across generations, are not strictly comparable in dollar value terms. To compare the fiscal burdens across generations, lifetime net tax rates must be calculated (see sidebar).

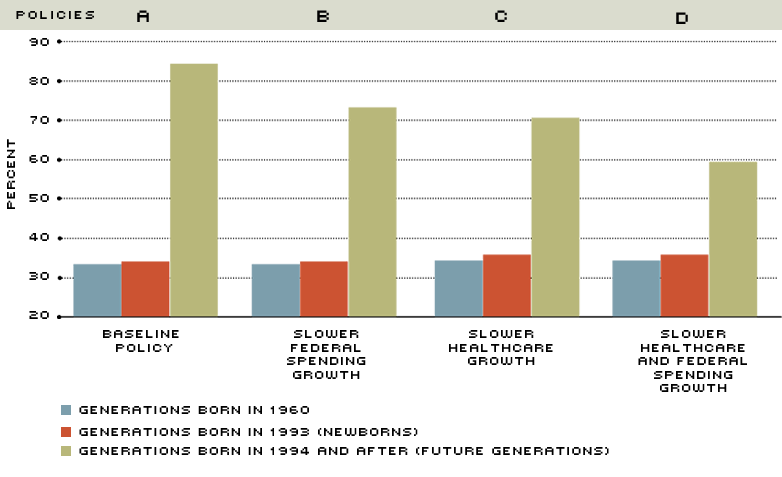

As the first set of bars in Figure 2 shows, under the fiscal policy that prevailed at the time of the 1995 study, Policy A, future generations faced an average net tax rate of 84.4 percent. This is significantly more than both the 33.5 percent rate faced by those who were 30 years old in 1960 and the 34.2 percent rate faced by those born in 1993 (newborns). These figures, which should be interpreted cautiously, indicate that unless current fiscal policy is put on a different path with respect to entitlements, the tax burden faced by future generations will greatly surpass that borne by those alive today. This is because future generations will have to devote a significantly higher percentage of their income to servicing the debt that has been accumulated to pay for the policies that benefit those alive today.

Lifetime Net Tax Rates Under Existing Fiscal

Policy and Three Alternatives

SOURCE: Auerbach, Gokhale and Kotlikof (1995)

Harsh Medicine

One of the main criticisms of generational accounting estimates is that it is unreasonable to expect that those currently alive will largely escape paying for the accumulating fiscal burdens wrought by existing policies. Most economists and policymakers, however, agree that current generations of tax payers must eventually bear some of the burden of returning fiscal policy to a more sustainable path. The question is: How much of a burden? To address this issue, AGK conducted two experiments in their 1995 study. First, what would happen to the net tax rates faced by current and future generations if some of the burden of correcting the generational imbalance were to be shifted to current generations (those born in 1993 or before) in the form of reduced government spending or higher taxes? And second, would these policy changes be enough to equalize the generational tax burden, or would additional measures be needed?

In the first experiment, AGK compared the net tax rates of both current and future generations calculated under baseline policy, Policy A, and three alternative policies. Under the first of these alternative policies, Policy B, government spending is allowed to grow only at the rate of inflation after the year 2000. Under the second alternative policy, Policy C, government health care spending would grow by 2 percent a year less than projected before 2005; after 2005, however, it would resume its projected path. The third policy, Policy D, combines the effects of policies B and C.

If policies B through D—which are all very similar to current proposals being considered to balance the budget by 2002—are sound from a GA standpoint, the net tax rates faced by current and future generations should be approximately equal. As Figure 2 shows, they clearly are not. Although the alternative policies modestly lower the net tax rates faced by future generations, the first experiment shows that the burden these generations face is much higher than current generations. For example, enacting the most restrictive of the three policies, Policy D, reduces the net tax rate of future generations from just over 84 percent to just above 59 percent. Still, the improvement is modest because future generations' net tax bill would be roughly 65 percent higher than those born in 1993 (newborns). Thus, if restoring generational equity is an important concern for policymakers, this experiment suggests that more fiscal restraint is needed than those hypothesized in policies B, C or D.

The second experiment conducted by AGK attempts to determine how much more fiscal restraint is needed to ensure that future generations of taxpayers are made no worse off than current generations. To keep this simple, AGK assumed that policymakers decided to preserve the existing level of retirement benefits for future generations also. If this action were employed in 1996, average income tax rates would have had to increase immediately and permanently by nearly 43 percent—from 15.7 percent to 22.3 percent. If, however, policymakers decided to postpone these actions, the 1995 AGK study offered two alternative scenarios: Wait until 2001 or wait until 2016. Waiting until 2001 would mean a permanent 51.5 percent increase; waiting until 2016 would mean a near doubling of current tax rates.

The tradeoff, therefore, amounts to current generations paying higher net lifetime taxes so that future generations could pay less. But what would those tax rates be? If taxes had been raised in 1996 to maintain existing benefits, then current and future generations would have faced (equalized) net lifetime tax rates of almost 43 percent. However, waiting until 2001 to increase taxes would push this rate up to nearly 45 percent, and waiting until 2016 ratchets it up to about 53 percent.

The problem with raising taxes to restore generational balance is that an increase in taxes harms the young, working-age population more than the retired, elderly population. It's worth considering, therefore, what would happen if policymakers instead decided to distribute the fiscal burden more equally by changing the level of health and retirement benefits for both current and future generations.

Rerunning the above experiment according to this scenario indicates that if policymakers decide to wait until 2001, they would need to immediately cut all transfer payments (Social Security, Medicare and Medicaid) by 38 percent. Such a policy change would equalize lifetime net tax rates for current and future generations at about 40 percent. If policymakers were to wait until 2016, they would need to cut benefits by 63 percent, resulting in a net tax burden of 43 percent. These rates would be much lower than the 84 percent assumed under no change whatsoever and those that would occur if taxes alone were raised.

A Better Mousetrap?

As a tool to analyze fiscal policy, generational accounting has found a home mostly among a small, but growing, group of economists. To be sure, fiscal authorities in the United States are not ready to abandon the type of analysis they currently do.6 The reasons for this reticence seem to be twofold. First, calculating future tax burdens over time depends on what discount rate is used. This is potentially problematic because the true discount rate is not known—and even it was, it would probably not stay constant over time as GA practitioners assume.7 Second, assuming that future taxes, transfer payments, population and government spending all increase at a fixed rate seems implausible. To a large extent, though, these are shortcomings of any long-term forecasting exercise, rather than specific criticisms of GA. Nevertheless, even critics of GA do not seriously challenge the fundamental point made by its analysis: Maintaining current fiscal policy indefinitely means that future generations will have to shoulder a larger burden than those alive today—even under more optimistic growth assumptions. The question is how much of a burden.

Endnotes

- The reported deficit is the unified budget deficit, which includes an "off-budget component" (mostly Social Security) and an "on-budget"component (most everything else). In recent years, the off-budget component has been in surplus ($67 billion in FY 1996) because receipts from Social Security payroll taxes have exceeded the program's outlays. [back to text]

- See Congressional Budget Office (1997). [back to text]

- Pay-as-you-go policy essentially prohibits increased spending or lower taxes without some offset that would leave the unified budget deficit unchanged. Unless extended, this policy is set to expire at the end of FY1998. [back to text]

- See Kotlikoff (1992). [back to text]

- The difference between the net tax payments of males and females reflects such variables as expected lifetime earning differentials, labor force participation (fewer females enter the labor force than males, thus paying fewer taxes) and the fact that females on average live longer, thereby receiving more transfer payments during retirement. [back to text]

- See Congressional Budget Office (1996). [back to text]

- Haveman (1994), p. 96. [back to text]

- See Auerbach, Gokhale and Kotlikoff (1994). For a nontechnical discussion, see Kotlikoff (1992). [back to text]

- Putting the accounts in present-value terms is done so that all generations are on an equal basis. The present-value calculation for any sum of money (X) over any number of years (n) is $X/(1 + i)n, where i is the interest rate (called the discount rate). [back to text]

References

Auerbach, Alan J., Jagadeesh Gokhale, and Laurence J. Kotlikoff. "Restoring Generational Balance in U.S. Fiscal Policy: What Will It Take?" Economic Review, Federal Reserve Bank of Cleveland (First Quarter, 1995), pp. 2-12.

______. "Generational Accounting: A Meaningful Way to Evaluate Fiscal Policy," Journal of Economic Perspectives (Winter 1994), pp. 73-94.

Congressional Budget Office. "The Economic and Budget Outlook:Fiscal Years 1998-2007," A Report to the Senate and House Committees on the Budget, Congress of the United States (January 1997).

______. "The Economic and Budget Outlook: Fiscal Years 1997-2006," A Report to the Senate and House Committees on the Budget, Congress of the United States (May 1996).

______. "Who Pays and When? An Assessment of Generational Accounting," CBO Study, Congress of the United States (November1995).

Haveman, Robert. "Should Generational Accounts Replace Public Budgets and Deficits?" Journal of Economic Perspectives (Winter 1994), pp. 95-111.

Kotlikoff, Laurence J. Generational Accounting: Knowing Who Pays, and When, for What We Spend (The Free Press, 1992)

Office of Management and Budget. Budget of the United States Government, Fiscal Year 1998 (U.S. Government Printing Office, February 1997).

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us