Was the Great Moderation Simply on Vacation?

From around 1984 to the mid-2000s, U.S. macroeconomic volatility dropped to unusually low levels. Economists dubbed the period the “Great Moderation.” With the arrival of the Great Recession, many declared the Great Moderation over. However, data indicate that the increased volatility in 2007-09 may have been a temporary blip instead of a reversion back to the days of high volatility.

To understand whether the Great Moderation has ended, we need to look at what may have caused it. There are three main explanations:

- Good luck: The shocks that derailed growth and price stability in the 1970s and early 1980s failed to rear their ugly heads over the subsequent 20 years.

- Structural change: Improved information technology, especially related to inventory management, and financial deregulation resulted in much smoother economic progress.

- Better monetary policy: Former Federal Reserve Chairman Paul Volcker set a precedent of aggressively reining in inflation.

The extent to which we believe each explanation played a role in the volatility reduction influences our opinion of whether the Great Moderation is likely to have returned.

- If we believe that good luck played the largest role, then we may think we have lost those golden years forever.

- If we believe that structural changes and/or monetary policy played a relatively larger role, then we should view the increased volatility during the Great Recession as the product of temporary factors that should have died out by now.

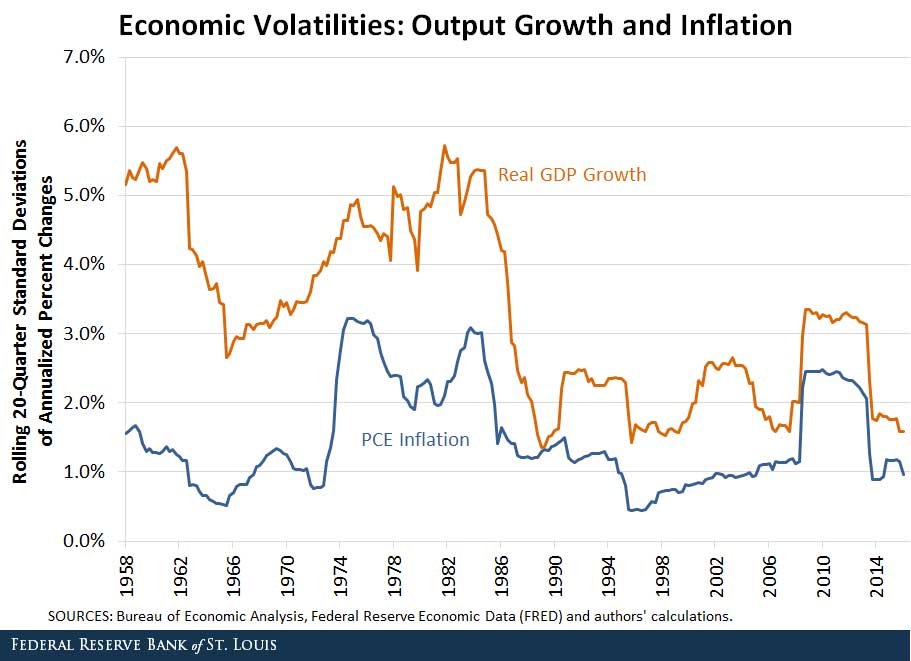

Fortunately, we don’t have to rely on theories to answer this question. We have seven years of GDP and inflation data. The figure below shows the volatilities of real GDP growth and inflation over the past several years.

We can very clearly see the Great Moderation. We can also see the effects of the Great Recession. Note that the value at each date is the standard deviation in each variable using data from that quarter and the 19 quarters preceding it. Hence, it is not very surprising that the effects of the recession didn’t diminish until late 2013. Once they did, however, volatility dropped back down to levels consistent with the Great Moderation.

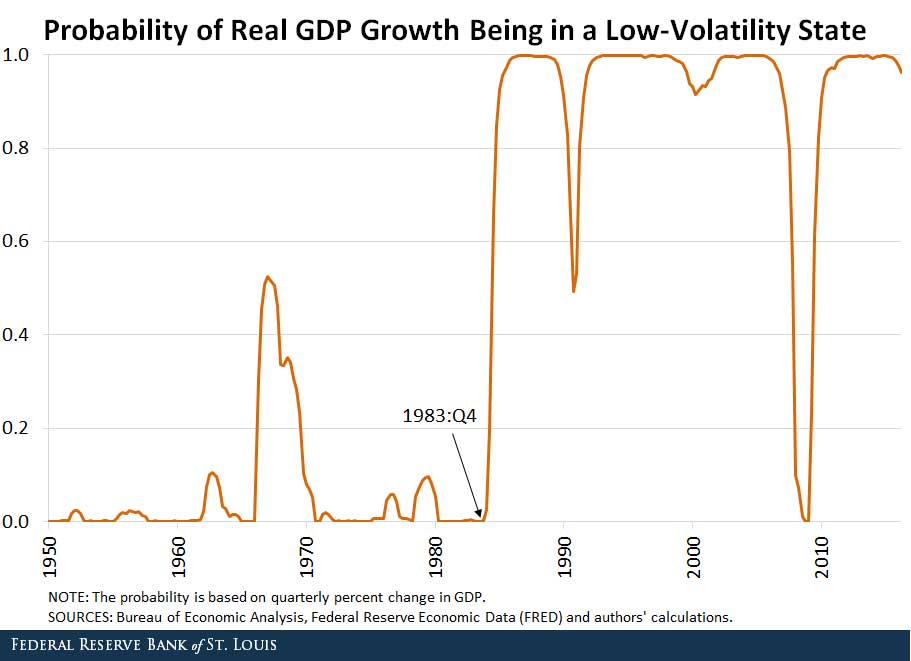

Because we can think of periods of high volatility and low volatility as different states of the world (like cloudy and sunny), we can estimate the probability of being in each state at a given point in time.1 The figure below plots this probability for real GDP growth.

The results agree with those of the first figure: The Great Recession resulted in only a temporary increase in volatility. So the data say that the Great Moderation never really left. It just took those twenty years of steady earnings growth and treated itself to a two-year vacation.

Therefore, while good luck likely played a role, a lot of credit should probably be given to a more structurally stable economy and better monetary policy. The U.S. economy experienced one of its largest shocks ever and has continued to face shocks from oil prices and international economic instability, yet it has gone back to its old low-volatility ways.

Notes and References

1 In this case, we used a Markov regime-switching model. Think of “regime” as being synonymous with “state.” The model basically looks for the presence of different states in the data. The results can then be used to estimate the probability of being in each state at a given point in the data.

Additional Resources

- On the Economy: New SEC Rules Cause Shift in Money Market Fund Assets

- On the Economy: Labor Compensation and Productivity Gap Keeps Growing

- On the Economy: Consumer Surveys, Inflation Expectations and the FOMC

Citation

Christopher J. Waller and Jonas Crews, ldquoWas the Great Moderation Simply on Vacation?,rdquo St. Louis Fed On the Economy, Sept. 26, 2016.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions