Feducation Video Series

Welcome to the Feducation video series! Designed for learners of all ages, this series offers three videos to enrich your understanding of the Federal Reserve’s role in shaping the economy through monetary policy tools.

Money and Inflation Explained

Discover the functions of money, the relationship between the supply of money and inflation, and how changes in the money supply affect the economy.

Unemployment and Monetary Policy

Learn how unemployment is defined and measured in economic terms, and how the Fed pursues maximum employment and price stability.

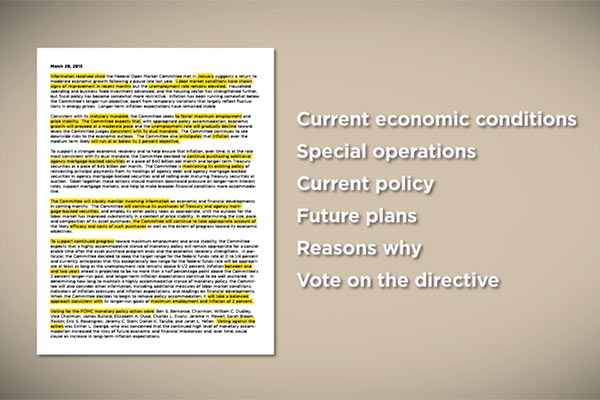

Understanding an FOMC Statement

Learn how to read and understand an FOMC statement and what the statements mean. This video overviews Fed communication strategies for transparency and clarity.

---

If you have difficulty accessing this content due to a disability, please contact us at economiceducation@stls.frb.org or call the St. Louis Fed at 314-444-8444 and ask for Economic Education.