The Great Retirement: Who Are the Retirees?

This Institute for Economic Equity spotlight on the labor market focuses on the continued exit from the labor force of workers, primarily those age 65 and older. Our estimates from the monthly Current Population Survey indicates that there are 3.3 million or 7% more retirees as of October 2021 than in January 2020.

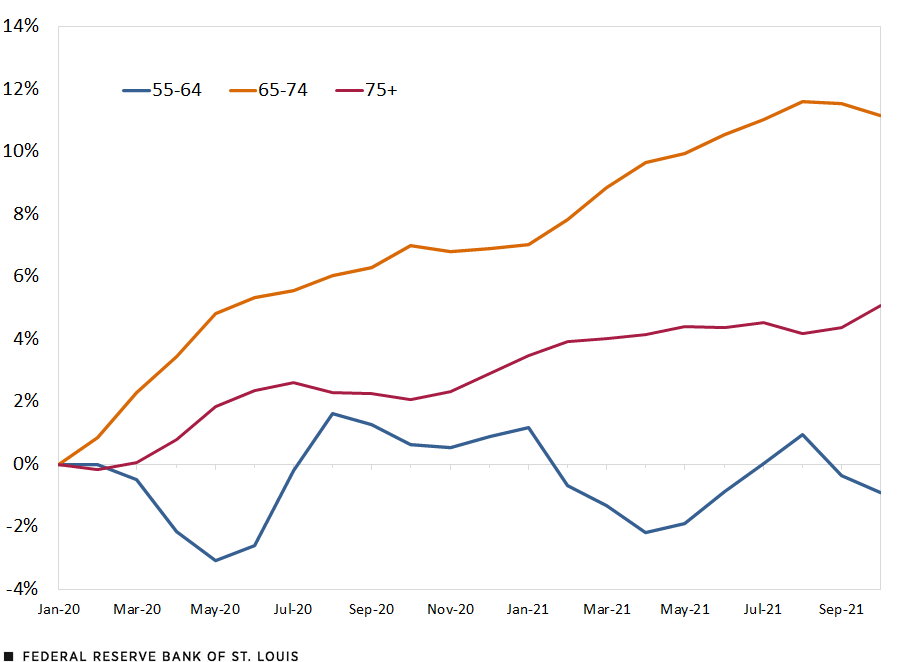

The figure below shows that the increase is largely among those age 65 and older, with notably stronger growth among those ages 65 to 74. In contrast, retirements among those ages 55 to 64 have been largely flat during the pandemic. The rate of retirements exceeds that predicted by the demographic shift of baby boomers into retirement. This Great Retirement is a particularly important trend to understand as the nation is grappling with widespread labor shortages.

Cumulative Percent Change in the Number of U.S. Retirees since January 2020

SOURCES: IPUMS-CPS and authors’ calculations.

NOTE: Percent change is calculated using a three-month moving average of the number of retirees.

A Demographic Profile of Retirees

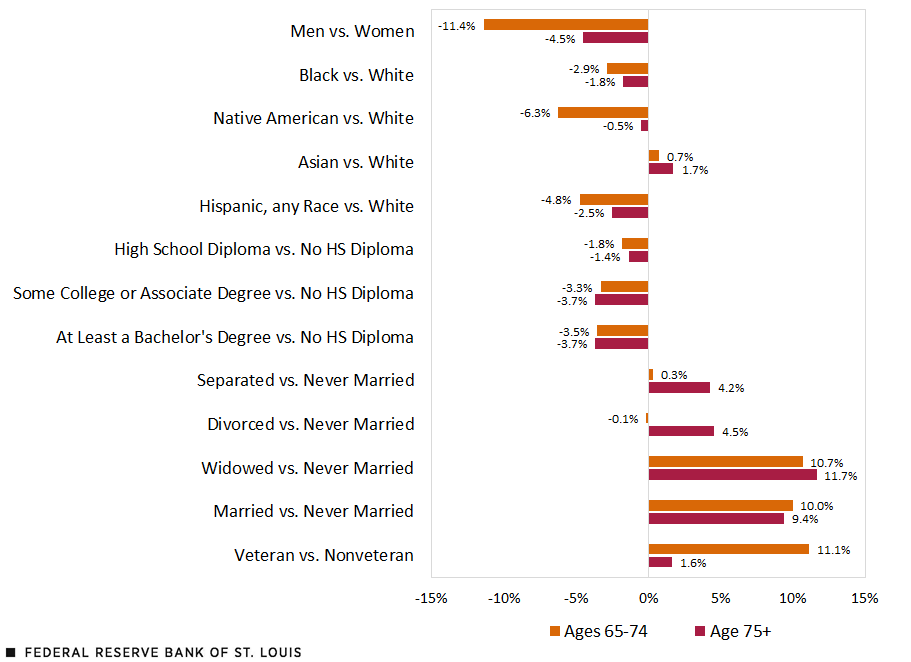

Using IPUMS-CPS survey data, we developed a profile of who is more likely to be retired within the age groups in which the bulk of retirements have occurred.These results were largely the same when using the CPS microdata provided on the Bureau of Labor Statistics website. Combining the results into a “typical” retiree, retirements were much more common among older white women without a college education. Our other findings were the following:

- Male workers were less likely to be retired than their female counterparts. This difference was far more pronounced among workers ages 65 to 74.

- Black, Hispanic and Native American workers were less likely to be retired than their white peers of similar ages. However, there was no difference in the likelihood of retirement between Native American and white workers age 75 and older. Asian workers were slightly more likely to be retired than white workers of similar ages.

- Workers who were married or widowed were more likely to be retired than their never-married, single peers.

- Findings were more complicated among workers who were separated or divorced. These workers were more likely to be retired among those 75 and older, but at younger ages there was no meaningful difference.

- Workers with at least some college education were less likely to be retired than their peers with a high school diploma or less education.

- Results by income (not displayed here) show a declining likelihood of retirement as household income increases.

- Veterans were more likely to be retired versus nonveterans, especially among those workers ages 65 to 74.

Differences in the Probability of Retirement

SOURCES: IPUMS-CPS and authors’ calculations.

NOTE: The differences shown are based on coefficients of interest from a linear probability model of self-reported retirement status on demographic factors, income and time.

Historic Asset Gains May Prompt Retirements

The tumult of the pandemic labor market (including the risks of COVID-19 exposure) may have motivated retirements among those workers with the means to do so. Recent record levels in the value of assets, such as investments and residential real estate, may make that decision to retire easier, financially speaking.

The Federal Reserve Board’s Distributional Financial Accounts offers timely information on asset appreciation during the pandemic. After adjusting for inflation and population growth, average net worth jumped 12% and 14.8% among households with a head of household aged 55 to 69 and 70 and older, respectively.

These notable wealth gains also include liquid cash support via stimulus checks. Collectively, these gains have bolstered household balance sheets during the pandemic. These stronger balance sheets in turn likely created a pathway to retirement for many workers.

Mental Health Distress

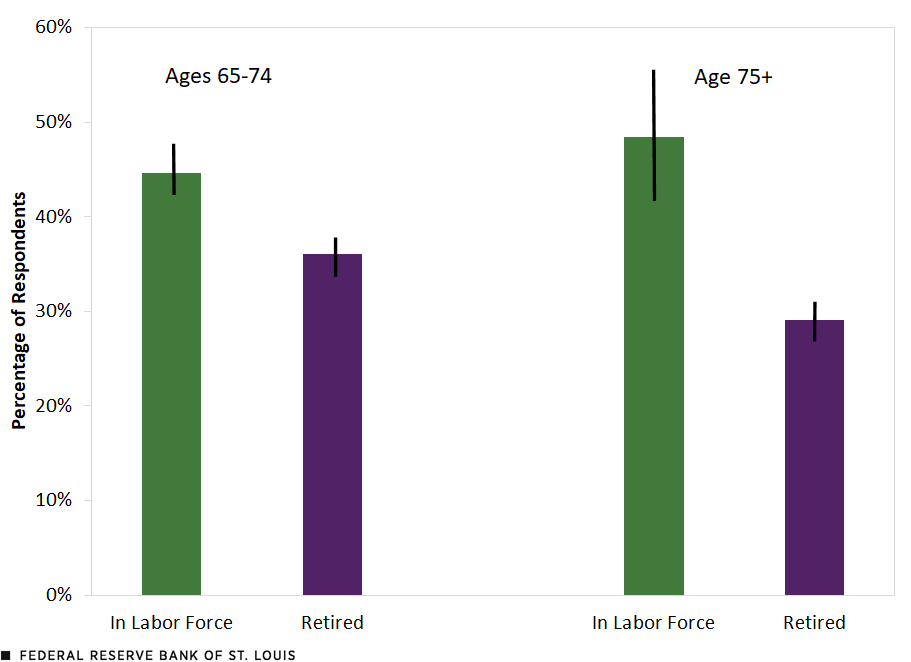

During the pandemic, mental health challenges became more prevalent. Increasing mental health distress was a concern even before the pandemic, represented by a rise in “deaths of despair.” Using the Census Bureau’s Household Pulse Survey, we found that rates of anxiety were significantly lower among retirees relative to their similarly aged peers still in the labor force. This anxiety may reflect the fear of the virus, which has had disproportionately lethal effects on these age groups. Mitigating the spread and risk associated with COVID-19 may represent one pathway back to the labor market.

Older People Experiencing Anxiety in Past Week,

By Age and Employment Status

Sept. 28-Oct. 11, 2021

SOURCES: Census Bureau’s Household Pulse Survey and authors’ calculations.

NOTE: The black vertical line represents the estimates’ likely ranges (90% confidence intervals). For example, in the case of retirees who were 75 and older, the upper bound was 31.4% and the lower bound was 26.8%.

The Return of the Retirees?

Questions remain regarding the permanence of these retirements. Perhaps counter to popular perception, retirements don’t necessarily constitute a permanent shift out of the labor force, as many retirees eventually return to the labor market in some form. However, recent evidence suggests this is happening at noticeably lower rates relative to other downturns. Given the mental distress associated with being in the labor force during a pandemic, employers might be able to retain and bolster their workforce with experienced talent if they can mitigate the risk and fear of COVID-19 as well as provide additional support for mental health. The Institute will continue to follow developments in the Great Retirement in subsequent work.

Notes and References

- These results were largely the same when using the CPS microdata provided on the Bureau of Labor Statistics website.

This blog offers commentary, analysis and data from our economists and experts. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us

All other blog-related questions