Metro Profile: Louisville Successfully Transitions from Industrial to Service Economy

Welcome to the Metro Profile. This new feature replaces the long-running Community Profile. In each issue, we will focus on one of the more than 20 metropolitan statistical areas in the District, using data to explain what drives the economy of that MSA. For the most part, the data come from FRED® (Federal Reserve Economic Data), the online economic database of the St. Louis Fed. Some of the information in these articles is also anecdotal, provided by business contacts for use (anonymously) in our economic reports, such as the Beige Book and Burgundy Books.

Let us know what you think about Metro Profile. Submit your comments in a letter to the editor at www.stlouisfed.org/legacy_assets/publications/re/letter.cfm. You can also mail a note to the editor, Subhayu Bandyopadhyay, at the Federal Reserve Bank of St. Louis, Box 442, St. Louis, MO 63166-0442.

The Louisville-Jefferson County, Ky.-Ind., metropolitan statistical area (known informally as the Louisville MSA) is the largest MSA in Kentucky and the third-largest MSA in the Federal Reserve's Eighth District. The Louisville MSA has a population of 1,251,351 and a labor force of 643,271. The per capita personal income was $39,037 in 2011 (the most recent year for which data are available), about 6.1 percent less than that for the U.S. See the accompanying figures for perspective on the data cited in this article; the table and charts also include additional data that help tell the story about Louisville's economy.

In the postrevolutionary U.S., Louisville was an important western outpost. Situated at the Falls of the Ohio, Louisville became a key port for the western frontier. Similar to its inland-port contemporaries, such as Cincinnati and St. Louis, Louisville had an industrial river economy in the beginning; growth was driven by heavy manufacturing, shipping and trade. Louisville also gained attention for its bourbon whiskey, Louisville Slugger baseball bats and Kentucky Derby, cultural hallmarks that live strong today.

Postwar Louisville saw a movement away from heavy manufacturing and away from river trade, as production processes and labor needs changed across the country. Coupled with deurbanization and population loss, Louisville's economic transition was typical of that of industrial cities. Atypical was Louisville's ease of adapting to a modern postindustrial service economy.

As it stands today, the city is a particularly strong hub for the health-care and food-service industries. Logistics and distribution, as well as recently expanding manufacturing, are other industries of note.

This economic transition also helped dampen urban population loss experienced in similar cities and even helped garner healthy population growth in recent years.

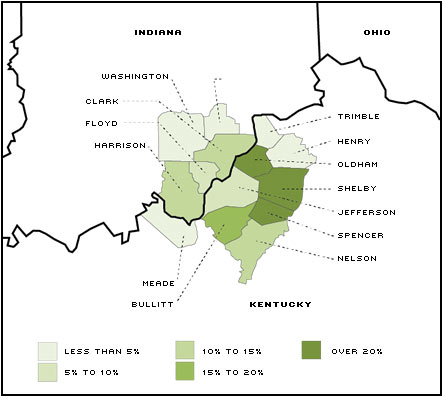

Over the past 10 years (2002-2012), Louisville's population increased by 9.7 percent, noticeably faster than Kentucky's growth of 7.1 percent and just above the national rate of growth, 9.1 percent. Within the metro area, Jefferson County, Ky., holds a substantial majority of Louisville's population: about 60 percent of the total. In the past decade, there has been some shift in the population: Jefferson County grew 7.3 percent, while Clark County, Ind., the second- largest county in the MSA, grew at almost twice the rate: 14.3 percent.

Much of the MSA's growth over the period can be attributed to Kentucky-based counties surrounding the city. Spencer, Shelby and Oldham counties grew the fastest, with rates of 31.7, 25.5 and 24.7 percent, respectively, between 2002 and 2012. These three counties largely outpaced population growth in Kentucky and the nation. As a result of this growth, Spencer, Shelby and Oldham counties gained about 1.7 percent of Louisville's population; today, about 10 percent of the population is located in these three counties.

Economic Drivers

Humana, a managed-health-care company on the Fortune 100 list, has headquarters in downtown Louisville. By revenue, Humana is the largest publicly traded company based in town. With 11,000 local employees, it is the second-largest Louisville company by local employee count.

Six of Louisville's 10 largest employers operate in the health-care industry; they range from insurance companies to hospitals. Norton Healthcare and Kentucky-One Health are two other companies of note, with 9,658 and 5,898 local employees, respectively, as of July 2012. Helped by the strong research atmosphere stemming from the University of Louisville and the region's early advances in heart transplants, Louisville's health-care industry has consistently driven economic growth.

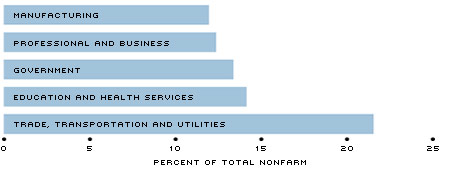

Education and health-services payroll employment, which comprises about 14 percent of total nonfarm employment, has seen largely positive growth over the past decade. Between January 2003 and January 2013, employment in education and health services increased by 14,300 (5,500 in the narrower health-services industry), while total payroll employment in Louisville increased by about 26,000 jobs.

| The Federal Reserve Bank of St. Louis is looking for local business leaders in the Eighth District to join the Bank's panel of contacts. Leaders are surveyed between four and eight times per year to gather information about the economy in their area; this information is distilled and passed on to our president and others who participate on the Federal Open Market Committee, our nation's chief monetary policymaking body. All information is compiled in a manner to preserve anonymity. To see a sample survey, go to https://research.stlouisfed.org/beigebooksurvey. |

Several international restaurant brands also call Louisville home. The most notable is Yum Brands, owner of KFC, Pizza Hut, Taco Bell and WingStreet, making it the largest fast-food restaurant company in the world. By revenue, Yum Brands is the second-largest publicly traded company headquartered in Louisville and employed 1,558 workers locally, as of July 2012. Papa John's pizza has also become an international brand and is a top local employer, as is the restaurant chain Texas Roadhouse. In the food industry, however, employment in the corporate headquarters of these restaurant companies falls under professional and business services employment, which comprises about 12 percent of Louisville's total nonfarm employment.

One other economic driver of note is the air-freight arm of United Parcel Service, UPS Airlines. Although its parent company calls Atlanta home, UPS Airlines is based in Louisville. Because of this presence, UPS is the largest local employer, with a July 2012 local employee count of 20,117, nearly twice the amount of the runner-up, Humana. This employment presence has driven the growth in the region's transportation sector, which employs about 3 percent of the MSA's workers. Between January 2003 and January 2013, payroll employment in the transportation sector increased by 1,600 jobs, or 6.4 percent of total employment growth over this period.

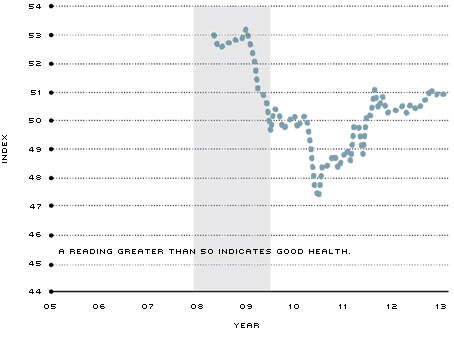

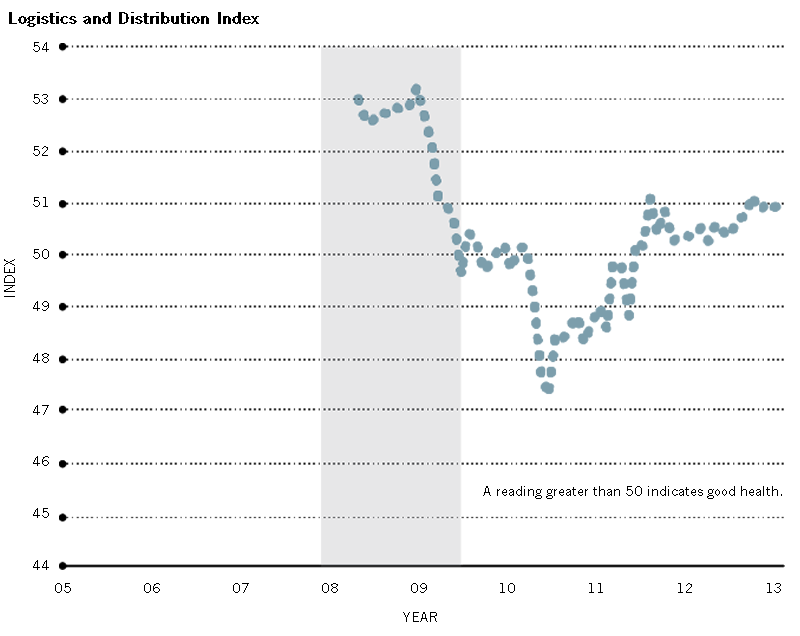

Louisville's location at a nexus of transportation systems has made it a trade and distribution hub throughout its history. As such, the Logistics and Distribution Institute at the University of Louisville keeps the national LoDI Index, which gauges the health of logistics and distribution activity. The most recent reading showed 51, indicating a healthy amount of logistics and distribution activity (greater than 50 indicates good health), which is generally viewed as a positive sign for the economy.

Current Conditions

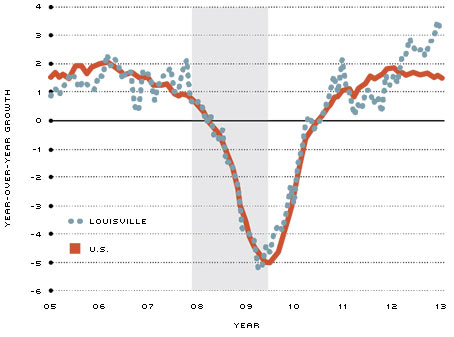

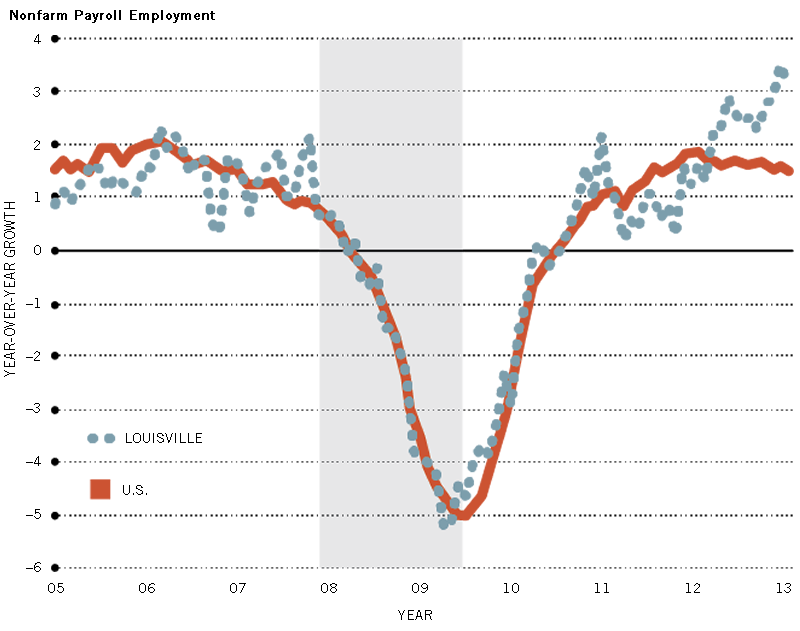

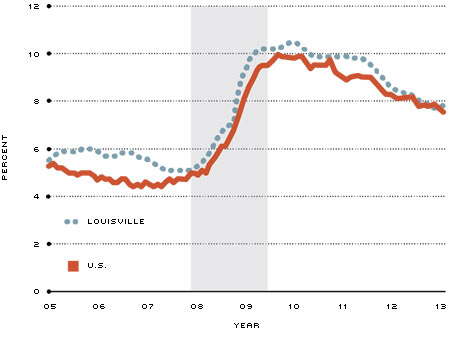

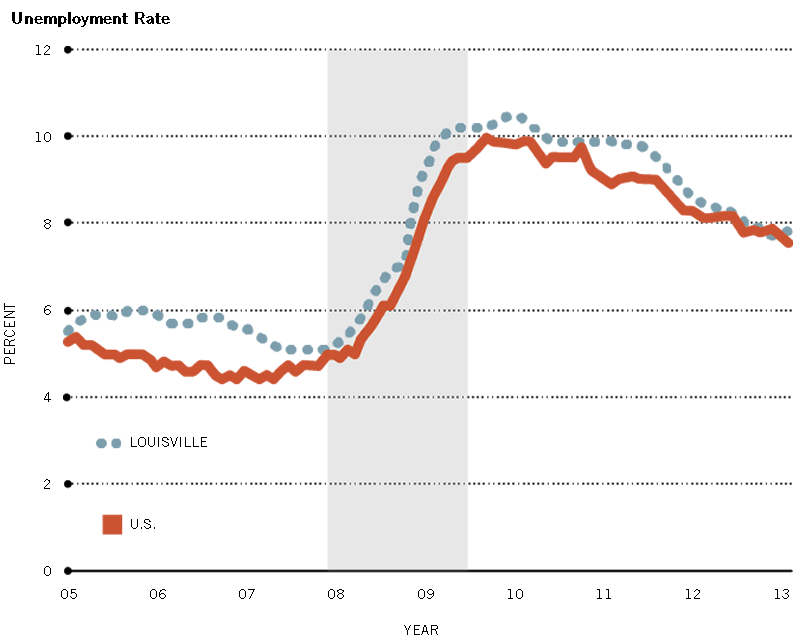

In the postrecession years, Louisville's nonfarm payroll employment growth has typically been on track with the nation's. However, Louisville has seen increases in the last year that have outpaced those of the U.S. As of March 2013, year-over-year growth in nonfarm employment doubled the national rate of 1.5 percent. This 3 percent growth translates to an increase of 18,800 jobs over a 12-month period, or almost three-quarters of the increase experienced over the past 10 years. These gains have helped to reduce the unemployment rate over the past year to a level consistent with the national rate.

| For your convenience, key data that pertain to the Eighth District have been aggregated on a special web page at https://research.stlouisfed.org/regecon/. To see all that FRED offers, go to http://research.stlouisfed.org/fred2/. |

The apparent stall in the decline of unemployment in recent months, even as employment growth is strong, is likely attributable to growth in Louisville's labor force. This is a good reflection of better labor conditions, as more area workers who have been out of the labor force re-enter and seek employment. Since March 2012, Louisville has added almost 19,000 jobs to nonfarm payrolls, with almost 15,000 people entering the labor force. During that time, the unemployment rate fell from 8.5 percent to 7.8 percent.

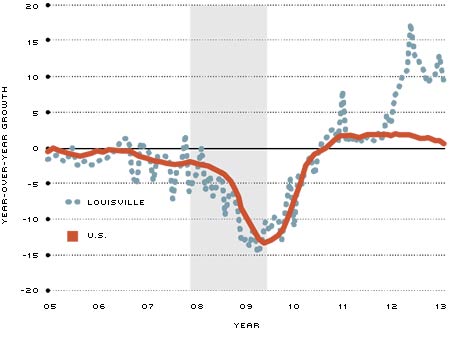

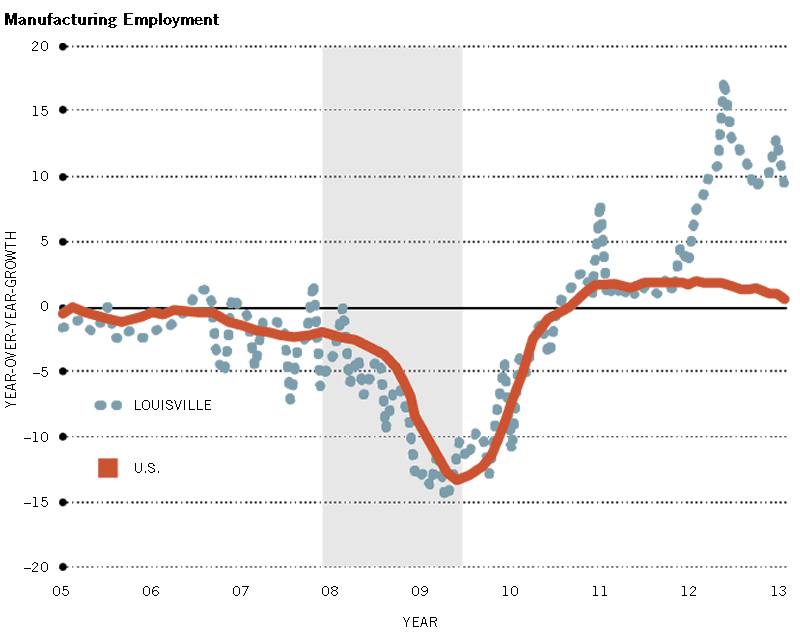

Manufacturing employment, representing about 12 percent of total nonfarm employment in Louisville, has been a particularly strong growth driver. Generally on trend with the U.S. as a whole since 2005, Louisville's manufacturing employment began largely outpacing U.S. growth over the past year. Manufacturing employment increased by about 9 percent (6,300 jobs), contributing one-third of the new jobs in Louisville over the past year. These increases in growth are attributable to increased production from auto manufacturers, such as Ford and Toyota. Ford's truck plant is the fourth-largest local employer, with 8,696 employees. GE Appliances has also picked up employment lately as it added a product line; it now has 5,000 local employees.

This strong growth from manufacturing employment and the consistency from Louisville's traditionally strong sectors like health care have contributed to an overall positive current outlook for Louisville's economy.

What's around the Bend?

Recently, U.S. cities have come under criticism for their decaying and dilapidated infrastructure, specifically in bridge maintenance. This problem is particularly bad in older industrial cities, where tax revenue has been hurt by suburbanization and dwindling urban economies. Bucking the trend, Kentucky and Indiana have started on the Ohio River Bridges Project, which involves repairing a number of bridges and building two new ones over the Ohio River. One of the new bridges will connect downtown Louisville with sister city Jeffersonville, Ind. The second bridge will complete an interstate loop outside of the city center; this is a smaller undertaking.

Since 2003, politicians in both states have pushed for a cost-effective solution to the region's transportation and safety problems. The Ohio River Bridges Project commenced in June 2013 with the construction of a six-lane cable-stayed downtown bridge and the overhaul of the existing Kennedy Bridge. With an estimated cost of $2.6 billion, this undertaking represents about 1 percent of the metro area's annual output, as measured by gross metropolitan product.[1] It appears the project will benefit the local economy through construction and skilled labor, as well as improved transportation.

"The Ohio River Bridges Project will have a positive impact on construction employment growth and will generate significant economic benefits over the next three-plus years."

–Louisville area commercial real estate contact [2]

Assuming no major shifts, Louisville can expect its stable-growth sectors of health care and logistics to provide consistency in employment trends moving forward. Coupled with recent vigor in heavy manufacturing, such as for autos, and the large undertaking of the Ohio River Bridges Project, area employment conditions should continue to improve to postrecession bests. Should these trends continue, Louisville will continue to experience solid economic activity in this postrecession time.

Logistics and Distribution Index

{kind=link}

NOTE: Data are from the University of Louisville and are easily accessible in the St. Louis Fed's economic database, FRED, using this series ID: LODINIM066N. Gray shading in all figures indicates recession period.

Nonfarm Payroll Employment

{kind=link}

NOTE: Data are from the U.S. Bureau of Labor Statistics and are easily accessible in the St. Louis Fed's economic database, FRED, using these series IDs: Louisville (LOINA) and US (PAYEMS).

Unemployment Rate

{kind=link}

NOTE: Data are from the U.S. Bureau of Labor Statistics and are easily accessible in the St. Louis Fed's economic database, FRED, using these series IDs: Louisville (LOIUR) and US (UNRATE).

Manufacturing Employment

{kind=link}

NOTE: Data are from the U.S. Bureau of Labor Statistics and are easily accessible in the St. Louis Fed's economic database, FRED, using these series IDs: Louisville (LOIMFG) and US (MANEMP).

MSA Snapshot

Louisville-Jefferson County, Ky.-Ind. (MSA)

| POPULATION |

1,251,351

|

| LABOR FORCE |

643,271

|

| UNEMPLOYMENT RATE |

7.8%

|

| PERSONAL INCOME (PER CAPITA) |

$39,037

|

Largest Sectors by Employment

Largest Local Employers

| 1. United Parcel Service Inc. |

| 2. Humana Inc. |

| 3. Norton Healthcare Inc. |

| 4. Ford Motor Co. Kentucky Truck Plant |

| 5. KentuckyOne Health Inc. |

Population Growth by County 2002-2012

NOTES: Population and employment are from the U.S. Census Bureau and U.S. Bureau of Labor Statistics and are easily accessible in the St. Louis Fed's economic database, FRED. For the first two panels and map, see these FRED series (IDs are in parentheses): Population (LOIPOP); Labor Force (LOILF); Unemployment Rate (LOIUR); Personal Income (LOIPCPI); Manufacturing (LOIMFG); Professional and Business (LOIPBSV); Government (LOIGOVT); Education and Health (LOIEDUH); and Trade, Transportation and Utilities (LOITRAD). Data for the employers panel are as of July 2012 and come from the Louisville Business Journal Book of Lists.

Endnotes

- This estimate is based off the most recent data on gross metropolitan product for Louisville, assuming the project takes about four years to complete. [back to text]

- In order to assess the regional economy, the Federal Reserve Bank of St. Louis collects anecdotal information from a panel of business contacts multiple times a year. This is an excerpt from results of the survey taken between May 1 and May 15, 2013. For more information, see https://research.stlouisfed.org/regecon/. [back to text]

Views expressed in Regional Economist are not necessarily those of the St. Louis Fed or Federal Reserve System.

For the latest insights from our economists and other St. Louis Fed experts, visit On the Economy and subscribe.

Email Us