The Millennial Wealth Gap: Smaller Wallets than Older Generations

When I was growing up, every afternoon after school I’d hike up my low-rise jeans and run up to the family computer to connect to the internet. After an enchanting cacophony of electronic dial-up tones, I’d be connected and would power up AOL’s AIM chat to make sure I wasn’t missing out on anything important.

By now, you’ve probably realized that I’m a millennial, and I look back on those days (in particular, the fashion) with equal parts nostalgia and horror.

Fast-forward to today, and many things have changed: JT and Britney are no longer together (disappointingly), and the internet is (mercifully) much faster. Other things remain the same, like the fact that young adults want to buy homes and think it’s a core part of the American Dream.See Clever, 2019 Millennial Home Buyer Report.

However, in my job as a policy analyst at the St. Louis Fed’s Center for Household Financial Stability, my colleagues and I have called into question millennials’ ability to achieve that dream—and financial stability more broadly.

Older millennials own fewer homes and are 34% “poorer” than expected

Indeed, only 44% of older millennial families were homeowners in 2016, which is 4 percentage points lower than we would expect based on older generations at the same age. We define older millennials as families headed by someone born between 1980 and 1989.

More striking is the fact that the typical older millennial family was 34% poorer than we would have expected. By typical, we mean a family at the middle, or median. This difference in their median wealth (what they own minus what they owe) amounted to $12,000.All dollars are inflation-adjusted using the CPI-U to 2016 dollars. Values have been rounded to the nearest $1,000. For someone at the beginning of adulthood, this is a lofty sum to miss out on.

Those without bachelor’s degrees fall 44% short of wealth expectations

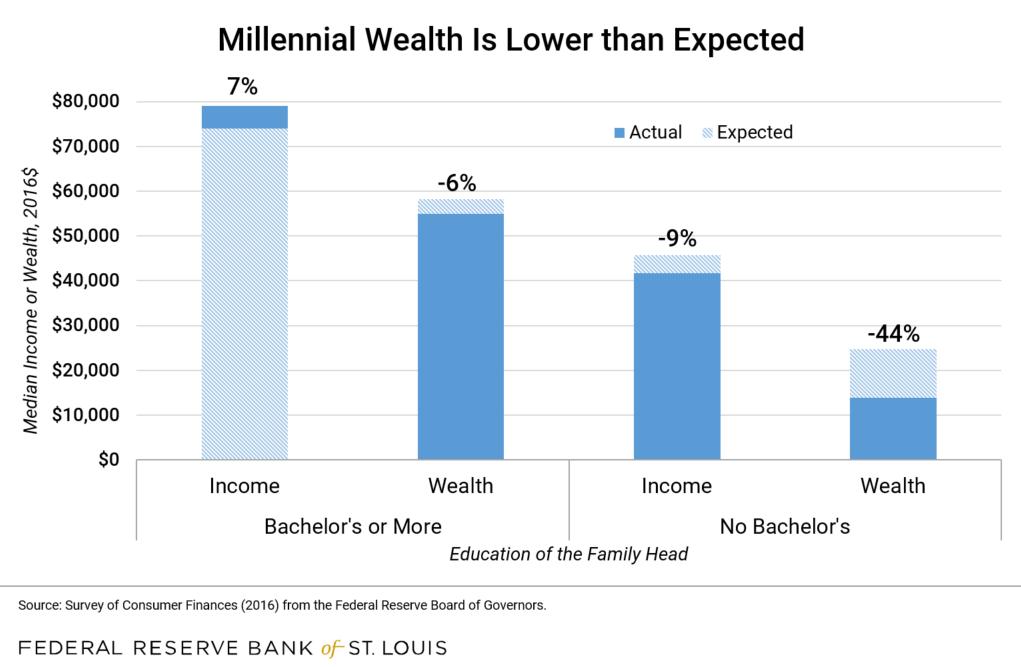

Breaking it down further—which we did when my colleagues and I published a chapter in New America’s The Emerging Millennial Wealth Gap—we found that it’s really older millennials without bachelor’s degrees who are struggling.

The typical income of this group in 2016 was nearly $42,000, which was 9% lower than what we would have expected based on older generations at the same age. The wealth gap between actual median wealth and what we’d expect was astounding: Typical wealth in 2016 was under $14,000, which was 44% lower than expectations of about $25,000.

Older millennials with at least a four-year college degree were doing better. With median income of nearly $79,000, they were about 7% above expected income of nearly $74,000. And they were only slightly below wealth expectations, with actual wealth of about $55,000 versus expected wealth of about $58,000. The figure below shows these numbers.

Notes: This stacked column chart shows median income and wealth in 2016 for families whose head was born between 1980 and 1989. The two bars on the left show income and wealth, respectively, for those families headed by someone with at least a bachelor’s degree. The two bars on the right show those measures for families headed by someone without a bachelor’s degree. The solid part of each bar represents actual income or wealth levels, while the shaded part represents expected income or wealth based on all generations with the same education. The percent difference between actual and expected levels is listed above each stacked column.

Older millennials also have high debt relative to income

For this generation of older millennials, having less money than older generations at the same age could be very problematic, indeed.

They have high debt relative to income compared with what we would expect, and the main types of debt they owe include student loans, auto loans and credit card debt. The assets financed by these types of debt haven’t increased in value as quickly as stocks and housing in the past few years (and in fact, many quickly fall in value after purchase, like cars). Catching up to older generations may prove to be a very difficult task.

It’s too early to know if we will succeed, or if we will have to echo NSYNC and say “bye bye bye” to our financial dreams. Only time will tell.

Notes and References

1 See Clever, 2019 Millennial Home Buyer Report.

2 All dollars are inflation-adjusted using the CPI-U to 2016 dollars. Values have been rounded to the nearest $1,000.

More to Explore:

This blog explains everyday economics, consumer topics and the Fed. It also spotlights the people and programs that make the St. Louis Fed central to America’s economy. Views expressed are not necessarily those of the St. Louis Fed or Federal Reserve System.

Email Us