The State Small Business Credit Initiative

In response to the illiquid market resulting from the Great Recession—which prevented many individuals and organizations from accessing credit, including small businesses—the Federal Reserve provided stimulus via quantitative easing and the federal government enacted the Troubled Asset Relief Program and the American Recovery and Reinvestment Act. These actions helped increase liquidity within the capital markets. A lesser-known program, the State Small Business Credit Initiative (SSBCI), was created as part of the Small Business Jobs Act of 2010. The SSBCI provided capital to small businesses at a time when small-business lending and equity investment had fallen sharply.

The SSBCI allocated nearly $1.5 billion to states to support small-business financing programs. Between 2011 and 2016, SSBCI provided public funds to leverage private-sector lending and equity investment into small businesses. States had authority to design and implement their own program or portfolio of programs. They also developed their own underwriting and operating procedures.

States funded a multitude of financing programs, which generally fell into one of five types:

- Capital access programs – provided a portfolio loan loss reserve for which the lender and borrower contributed a share of the loan value (up to 7 percent) that was matched on a dollar-for-dollar basis with SSBCI funds

- Loan guarantee programs – provided an assurance to lenders of partial repayment if a loan went into default once the lender made every reasonable effort to liquidate available collateral and collect on personal guarantees

- Collateral support programs – provided cash to lenders to boost the value of available collateral

- Loan participation programs – purchased a portion of a loan that a lender made, or made a direct loan from the state in conjunction with a private loan; the state often subordinated to the lender’s senior loan

- Venture capital programs – provided financing by purchasing an ownership interest or providing equity-like loans to enterprises that typically do not participate in debt financing markets

States’ economic development agencies were primarily responsible for administering the program, with the U.S. Department of the Treasury overseeing the program at the federal level. States partnered with eligible lenders—banks, credit unions, community development financial institutions (CDFIs) and state finance authorities—to deploy funds to small businesses. Community banks, midsized banks and CDFIs were the most active lenders, accounting for 94 percent of all SSBCI-supported loans. In addition to participating lenders, states also partnered with investment funds and local individual investors to finance small businesses through venture capital programs.

SSBCI required states to target small businesses, design programs that leverage private-sector lending and investing, and develop a plan to target underserved communities. This Policy Insight examines how the U.S. as a whole and how the states that comprise the Federal Reserve’s Eighth District—Arkansas, Illinois, Indiana, Kentucky, Mississippi, Missouri and Tennessee—met the financing needs of small businesses located in low- and moderate-income (LMI) and rural areas. Additionally, this Policy Insight examines the role CDFIs played in the SSBCI program with regard to financing small businesses in these underserved communities.

LMI Focus

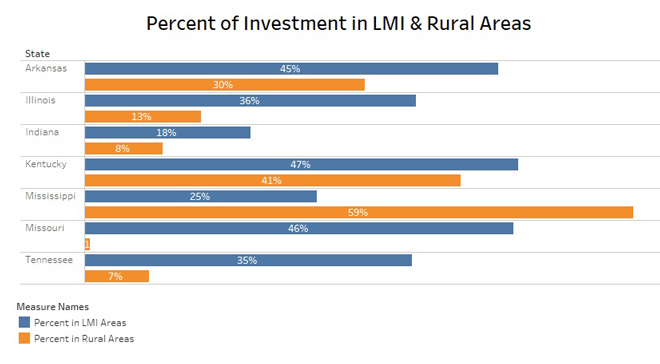

Over the six years that the program was active, the value of loans and investments made to small businesses located in LMI areas of the Federal Reserve’s Eighth District was $311 million. This constituted 32 percent of the total financing for small businesses, which is nearly identical to the 34 percent of capital across the country that financed small businesses located in LMI areas. The Eighth District states and the financing programs they utilized directed 68 percent of funding to middle- and upper-income areas. However, there was one notable exception. In Arkansas—particularly, the Fayetteville-Springdale-Rogers, AR-MO, metropolitan statistical area (MSA)—$42 million was invested in small businesses. These investments were made primarily through Arkansas’ venture capital program. Of the $34 million invested through the venture capital program, 80 percent was invested in small businesses located in LMI communities. The main lenders that deployed funds to small businesses in LMI areas across Arkansas were Arkansas Development Finance Authority (headquartered in Little Rock, Ark.), First Security Bank (headquartered in Searcy, Ark.) and Forge, Inc. (headquartered in Huntsville, Ark.).

Rural Focus

Through the SSBCI program, lenders and investors deployed just over 20 percent of total capital to small businesses located in rural areas of the Eighth District. This exceeds the national rate of 15 percent of total capital deployed to rural areas. Among the Eighth District states, Mississippi and Kentucky led the way with 59 percent and 41 percent, respectively, invested in rural areas.

Role of CDFIs

CDFIs were one of the major participating lenders to small businesses through the SSBCI. While there was no requirement that lenders and investors deploy a minimum amount in LMI or rural areas, the initiative did require states to develop a plan targeting underserved communities. As mission-driven lenders accustomed to leveraging funding from private and public sources to meet the financing needs of underserved communities, CDFIs were a natural partner for states. Nationally, CDFIs loaned and invested $630 million through the SSBCI; 46 percent was deployed in LMI areas and 18 percent was deployed in rural areas. By comparison, non-CDFI lenders and investors deployed almost 32 percent of funds to small businesses in LMI areas and 19 percent in rural areas. Across the U.S., the primary CDFI lenders were loan funds; major players included Opportunity Fund of Northern California (headquartered in San Jose, Calif.), Craft3 (headquartered in Seattle, Wash.), Southwest Georgia United Empowerment Zone Inc. (headquartered in Cordele, Ga.) and Access to Capital for Entrepreneurs (headquartered in Cleveland, Ga.).

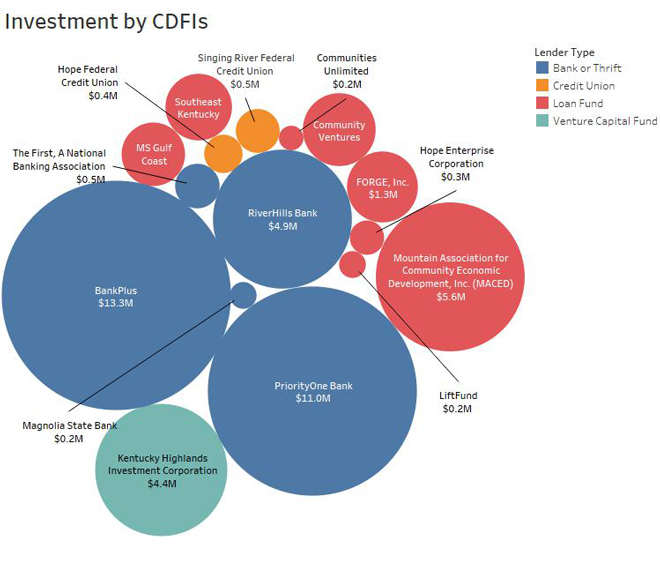

In the Eighth District, CDFIs loaned and invested a total of $45 million; 35 percent was deployed in LMI areas and 52 percent in rural areas. In other words, relative to CDFIs across the nation that participated in the program, CDFIs in the Eighth District over-performed on investments in rural areas and underperformed on investments in LMI areas. The primary CDFI lenders in the Eighth District were banks, the vast majority of which are based in Mississippi. In addition to MACED, major CDFI players in the SSBCI program in the Eighth District included Kentucky Highlands Investment Corp. (headquartered in London, Ky.) and three banks headquartered in Mississippi—BankPlus (Belzoni, Miss.), PriorityOne Bank (Magee, Miss.), and RiverHills Bank (Vicksburg, Miss.).

Conclusion

At a time when capital for small businesses was in short supply, the SSBCI program created a strong and effective incentive for lenders and investors to meet the financing needs of small businesses throughout the U.S. While 34 percent of investment financed small business in LMI areas across the country, some locations (e.g., the Fayetteville, Springdale-Rogers, AR/MO, MSA) saw significantly higher investment in LMI areas. There proved to be more challenges to finance small business located in rural areas, though states like Mississippi and Kentucky found ways to deploy substantial financing to these communities. Finally, CDFIs played a role in providing financing to small businesses through the SSBCI program during a time in which small-business lending and investment activity had otherwise fallen sharply.

Related Topics